A mortgage touchpoint strategy is a planned sequence of borrower communications, timed to mortgage milestones and triggered by borrower behavior, that reduces fallout and builds the trust needed to close loans on time. Most loan officers know they should follow up more consistently. The ones who actually close at a higher rate have a system behind that follow-up. That system is what the industry formally calls a communication cadence, though “touchpoint strategy” captures the same concept in more practical terms. This article breaks down the full framework: which milestones anchor your schedule, how automation and behavioral triggers work together, what TRID compliance requires, and how to keep messaging consistent across every channel your borrowers use.

Mortgage touchpoint strategy explained: the milestone framework

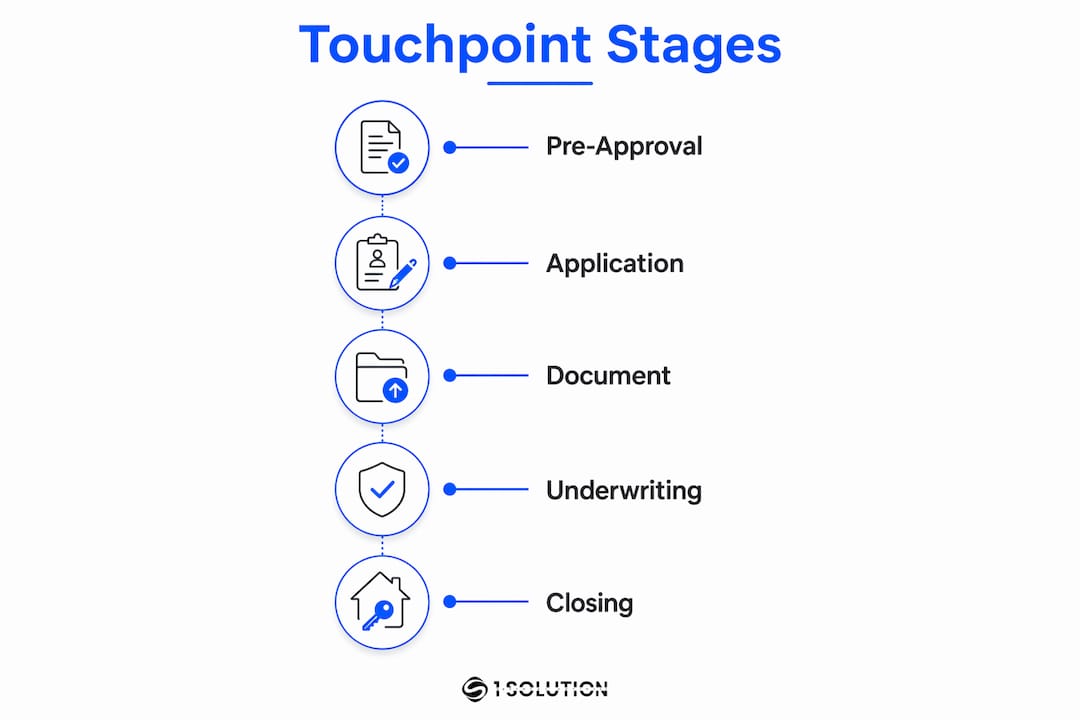

A touchpoint strategy only works when it maps to the actual stages of the mortgage process. Without that anchor, you end up with generic follow-ups that arrive at the wrong time and say the wrong thing.

The mortgage process follows a predictable timeline from application to closing, with distinct windows where borrower anxiety and drop-off risk spike. Understanding those windows is the first step in designing a cadence that actually reduces fallout.

Here are the core stages and their typical timing:

| Stage | Typical Window | Communication Priority |

|---|---|---|

| Pre-approval and inquiry | Days 1–3 | Immediate response, expectation setting |

| Full application submitted | Days 1–3 | Loan Estimate delivery, document checklist |

| Document collection | Days 1–7 | Daily or every-other-day reminders |

| Underwriting review | Days 14–30 | Status updates, condition responses |

| Clear to close | Days 28–40 | Closing Disclosure delivery, final prep |

| Closing | Days 30–45 | Confirmation, wire instructions, celebration |

The two highest-risk windows are document collection and underwriting. Borrowers go quiet during these phases not because they lost interest, but because they feel uncertain and do not know what to do next. A proactive communication rhythm during these windows reduces surprises and gives you early visibility into borrower hesitation before it becomes a lost deal.

Two regulatory deadlines also function as mandatory touchpoints. The Loan Estimate must be delivered within 3 business days after receiving a completed application. It is a standardized 3-page form showing estimated payments, loan terms, and closing costs. This is not just a compliance checkbox. It is your first real opportunity to set expectations and demonstrate transparency.

How to design a behavior-sensitive touchpoint cadence

Knowing the milestones is the foundation. Designing the actual cadence requires layering in borrower behavior so your outreach feels relevant rather than robotic.

The most effective cadences use automated triggers tied to specific borrower actions. Behavior-triggered outreach includes instant text messages plus phone calls within 5 minutes for new inquiries, and tailored check-ins at set intervals based on what the borrower has or has not done. This approach outperforms scheduled blasts because it meets borrowers at the moment they are already thinking about their loan.

Here is a practical sequence structure for the pre-approval phase:

-

Trigger: Application submitted. Send an immediate confirmation text and email with a document checklist and expected timeline. Follow up with a personal call within 5 minutes.

-

Day 2 (no documents received). Send a friendly SMS reminder with a direct link to the document portal.

-

Day 4 (partial documents received). Send a specific list of what is still missing. Avoid generic “we still need documents” language.

-

Day 7 (documents complete). Send a congratulatory message confirming the file is moving to underwriting, with a realistic timeline.

-

Day 14 (underwriting). Send a status update confirming the file is under review. Include a direct contact for questions.

Pro Tip: Use branching logic in your automation platform so borrowers who respond to a text do not also receive the follow-up call 10 minutes later. Treating a responsive borrower like an unresponsive one is one of the fastest ways to erode trust.

Channel diversity matters as much as timing. Multi-channel outreach using SMS, calls, email, webchat, and social messaging integrated into a unified inbox increases contact rates and borrower satisfaction. Different borrowers prefer different channels, and a unified inbox means your team sees the full conversation history regardless of where it started. A borrower who texted a question yesterday should not have to repeat themselves on a call today.

Poorly executed automation reduces your CRM to a glorified mailing list. Intelligent trigger-based sequences tied to borrower status and application activity provide timely, relevant communication without manual effort at every step.

Why compliance timing shapes your entire communication schedule

Compliance is not separate from your touchpoint strategy. It is built into it. Two TRID (TILA-RESPA Integrated Disclosure) deadlines define hard stops in your communication calendar that you cannot move around.

Key compliance requirements every loan officer must account for:

-

The Loan Estimate is due within 3 business days of a completed application, no exceptions.

-

The Closing Disclosure must be delivered at least 3 business days before closing. It is a final 5-page document showing actual loan terms, monthly payments, and closing costs.

-

Major changes to loan terms after the Closing Disclosure is issued restart the 3-day review clock. This can push your closing date and damage borrower confidence.

-

“Clear to close” is a separate milestone from Closing Disclosure delivery. Do not conflate them in your borrower communications. Telling a borrower they are “clear to close” before the disclosure review period ends creates confusion and potential legal exposure.

TRID compliance is not just a legal requirement. It is a communication design constraint. Your touchpoint schedule must account for these hard deadlines so your messaging never gets ahead of your disclosures.

Accurate disclosures prevent delays. Compliance failures under TRID carry penalties and borrower dissatisfaction that can damage your reputation and your pipeline. Build your cadence so that disclosure delivery triggers its own communication sequence: a confirmation message, a plain-language summary of what the borrower is reviewing, and a clear call to action for questions.

Loan officers who treat compliance touchpoints as relationship-building moments, rather than bureaucratic obligations, consistently report fewer last-minute surprises at the closing table.

How to maintain cross-channel consistency at moments of truth

Borrowers do not experience your organization the way your org chart is drawn. They experience it as one continuous relationship. When your loan officer says one thing, your document portal says another, and your support team has no record of the conversation, borrowers lose confidence fast.

Borrowers judge trust at “moments of truth,” which are the critical interactions during conditional approvals, document requests, and status updates where their confidence in you either solidifies or cracks. These moments require coordination across loan processing, underwriting, and support, not just a well-timed email.

Practical steps to maintain consistency:

-

Align messaging across every channel before a major milestone. If underwriting is about to issue conditions, your loan officer should know before the borrower does.

-

Use a shared communication log so every team member who touches the file can see what the borrower has already been told.

-

Address borrower questions proactively during conditional approvals. A condition letter without context is one of the most common sources of borrower panic.

-

Set clear internal SLAs (service level agreements) for response times. Slow response during key steps drives abandonment. Target response times of approximately 1.5 seconds for application submissions and 3 to 5 seconds for conditional approvals to reduce drop-off.

Pro Tip: After every conditional approval, send the borrower a plain-language explanation of what the condition means, what they need to do, and when you need it by. This single habit eliminates the majority of “what does this mean?” calls that slow your pipeline.

Cross-channel consistency requires integrating loan officer communications, document portals, underwriting updates, and support interactions into a unified borrower experience. The technology to do this exists. The discipline to implement it consistently is what separates high-performing loan officers from the rest.

Key takeaways

A mortgage touchpoint strategy works when it combines milestone-anchored timing, behavior-triggered automation, TRID-compliant disclosure sequencing, and cross-channel message alignment into one coordinated system.

| Point | Details |

|---|---|

| Anchor to milestones | Map every touchpoint to a specific mortgage stage, with heaviest focus on document collection and underwriting. |

| Use behavior triggers | Automate outreach based on borrower actions, not just calendar intervals, to stay relevant and timely. |

| Respect TRID deadlines | Build Loan Estimate and Closing Disclosure delivery into your cadence as hard communication triggers. |

| Unify your channels | Integrate SMS, email, calls, and portals into one inbox so no borrower message falls through the cracks. |

| Coordinate internally | Share communication logs across your team so every borrower interaction reflects a consistent, informed voice. |

What I have learned building touchpoint systems from the ground up

By Omar Khamisa

After 20 years working as a processor, underwriter, loan originator, and systems consultant, I can tell you that most touchpoint failures are not technology failures. They are empathy failures. Loan officers design follow-up sequences around what is convenient for them to send, not around what the borrower is actually experiencing at that moment in the process.

A borrower in underwriting is not thinking about your next marketing email. They are wondering whether their loan is going to be approved and whether they should be doing something right now. The right touchpoint at that moment is a short, specific status update that answers the question they have not asked yet.

The second mistake I see constantly is treating automation as a replacement for judgment. Automation handles the volume. It sends the right message at the right time without you having to remember to do it. But the content of that message still needs to reflect where the borrower actually is, emotionally and procedurally. A trigger-based system connected to real loan data, not just a static drip sequence, is the difference between a CRM that closes loans and one that just sends emails.

Speed matters more than most loan officers realize. The brokers I have worked with who respond to new inquiries within 5 minutes consistently outperform those who respond within an hour, regardless of how good their follow-up sequence is after that. First contact speed sets the tone for the entire relationship. Build your system around that reality, and the rest of your touchpoint strategy becomes much easier to execute.

— Omar Khamisa

Put your touchpoint strategy to work with 1 Solution Mortgage Software

1 Solution Mortgage Software was built by mortgage professionals who have worked every role in the process, and it shows in how the platform handles borrower communication. The platform brings CRM, multi-channel messaging, compliance management, POS, and LOS tools into one connected system designed specifically for independent brokers. You get behavior-triggered automation tied to real loan data, a unified inbox for SMS, email, and webchat, and built-in compliance tracking that keeps your Loan Estimate and Closing Disclosure timelines on schedule. No fragmented tools, no manual workarounds. If you are ready to run a touchpoint strategy that actually reflects how mortgage lending works, explore the platform and see what brokers built for brokers looks like.

FAQ

What is a mortgage touchpoint strategy?

A mortgage touchpoint strategy is a structured plan of borrower communications aligned with loan milestones and triggered by borrower behavior to maximize engagement and reduce fallout. It combines scheduled outreach, automated triggers, and compliance-aware messaging into one coordinated system.

When should the Loan Estimate be sent to a borrower?

The Loan Estimate must be delivered within 3 business days after receiving a completed mortgage application, as required under TRID rules. It shows estimated loan terms, monthly payments, and closing costs to help borrowers compare options before committing.

How does the Closing Disclosure fit into a touchpoint cadence?

The Closing Disclosure must be provided at least 3 business days before closing and triggers its own communication sequence, including a confirmation message and plain-language summary. Major changes to loan terms after delivery restart the 3-day review clock, which can delay closing.

What channels should a mortgage touchpoint strategy use?

An effective strategy uses SMS, phone calls, email, webchat, and document portal notifications integrated into a unified inbox. Multi-channel outreach reaches borrowers on their preferred platform and reduces missed connections during critical stages like document collection and underwriting.

How does automation improve a mortgage touchpoint strategy?

Automation tied to borrower actions and loan status, rather than static calendar intervals, delivers timely and relevant messages without manual effort. Using branching logic ensures that responsive borrowers receive different follow-ups than unresponsive ones, keeping communication appropriate to each borrower’s actual situation.