A mortgage broker platform is integrated software that centralizes every stage of the mortgage lending process, from borrower application through loan closing, into one connected system. The industry standard term for this technology is a mortgage origination and management platform, though "mortgage broker platform" is the phrase most borrowers and first-time homebuyers use when searching for it. These platforms combine a Loan Origination System (LOS), Point of Sale (POS), Customer Relationship Management (CRM), and a product/pricing engine to give brokers and borrowers a single, organized workflow. Whether you are buying your first home or managing a portfolio of investment properties, understanding how this technology works puts you in a stronger position at the negotiating table.

What is a mortgage broker platform and how does it work?

A mortgage broker platform is software that integrates LOS, POS, CRM, and pricing engines into one end-to-end workflow, replacing the fragmented stack of spreadsheets, email chains, and disconnected tools that once defined mortgage operations. Each component handles a distinct job, and together they eliminate the gaps where errors and delays typically occur.

Here is how the core workflow moves through a modern platform:

- Borrower application (POS layer). The Point of Sale system is the borrower-facing front door. You complete your application online, upload documents, and track your loan status in real time. The POS feeds your data directly into the LOS, so nothing gets re-keyed.

- Loan origination and underwriting (LOS layer). The LOS automates processes from application to funding, centralizing underwriting workflows and document fulfillment. Brokers review conditions, order appraisals, and manage compliance tasks inside the same system.

- Client communication (CRM layer). The CRM stores every borrower interaction, sends automated status updates, and flags follow-up tasks. Brokers using platforms like OMS report that reduced repeated data entry speeds applications and cuts processing errors significantly.

- Rate and product comparison (pricing engine). The pricing engine pulls live rates from multiple lenders simultaneously. Brokers can compare options for Conventional, FHA, VA, USDA, Jumbo, and Non-QM loans in seconds rather than hours.

- Automation features. Advanced platforms like Zeitro generate pre-approval letters automatically, use OCR technology to read and extract data from uploaded documents, and maintain compliance knowledge bases that flag regulatory issues before they become problems.

Pro Tip: When evaluating any mortgage broker platform, ask specifically whether the POS and LOS share a single database or sync through an API. A shared database eliminates sync errors entirely; an API integration is acceptable but introduces a small failure point.

The practical result of this integration is speed and accuracy. Centralized systems improve workflow speed compared to multiple disconnected tools, which means your loan moves faster and with fewer back-and-forth requests for documents you already submitted.

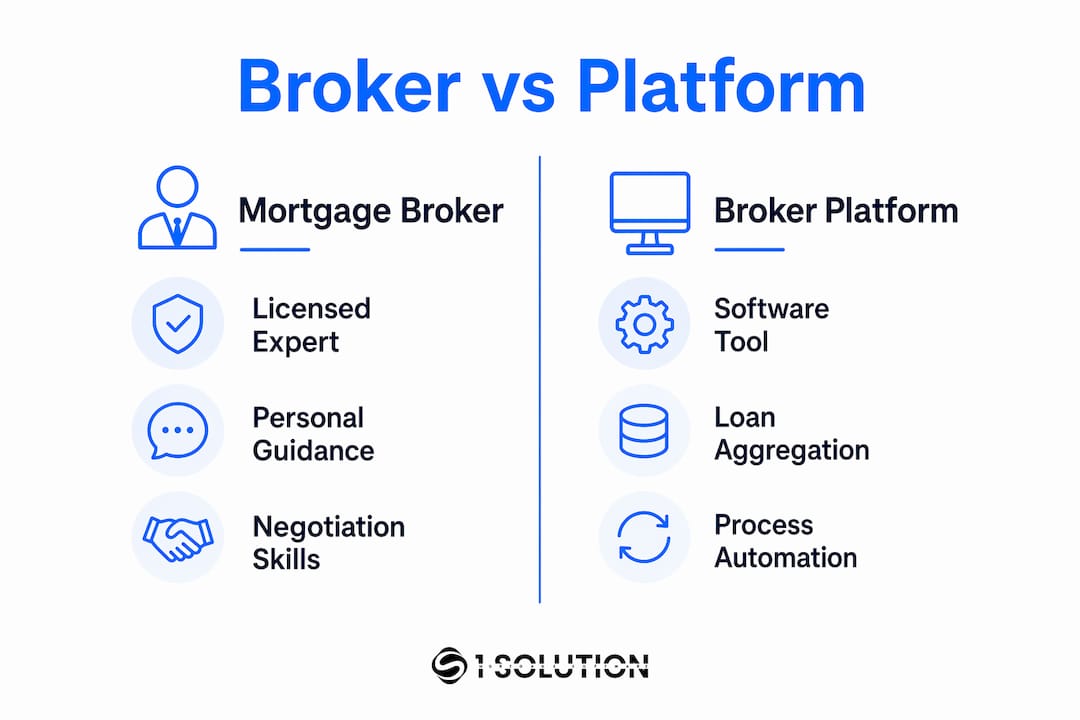

Mortgage broker vs direct lender: understanding the human and software roles

The distinction between a mortgage broker and a mortgage broker platform confuses many first-time homebuyers, and it matters.

A mortgage broker is a licensed intermediary who guides borrowers through the lending process and connects them with lenders. The broker is a person, bound by licensing requirements, fiduciary responsibilities, and professional judgment. A mortgage broker platform is the software tool that broker uses to do that job faster and more accurately. One is the professional; the other is the instrument.

The table below shows where each one contributes:

| Factor | Mortgage broker (the person) | Mortgage broker platform (the software) |

|---|---|---|

| Role | Licensed intermediary and advisor | Digital workflow and data management tool |

| Core function | Guides borrowers, negotiates with lenders | Automates applications, documents, and pricing |

| Decision-making | Applies professional judgment and experience | Flags data, generates options, supports decisions |

| Borrower relationship | Personal communication and trust-building | Status updates, document portals, automated alerts |

| Compliance | Holds license and bears legal responsibility | Maintains compliance checklists and audit trails |

The most effective lending experience combines both. Equifinance's broker portal demonstrates this balance well: the platform delivers instant credit decisioning and fast affordability calculations, but final underwriting decisions remain with human underwriters. Technology accelerates the process; human judgment protects the outcome. For borrowers, this means faster answers without sacrificing the careful review your loan deserves.

The mortgage broker vs direct lender question also becomes clearer through this lens. A direct lender uses its own capital and its own underwriting criteria. A broker, armed with a strong platform, shops your file across dozens of lenders simultaneously and finds the product that fits your specific situation. The platform makes that comparison fast and transparent.

Key benefits of mortgage broker platforms for borrowers and brokers

The advantages of using a mortgage broker platform fall into three categories: speed, access, and accuracy.

Speed and efficiency. Platforms that automate pre-approval letter generation and OCR document processing cut the time between application and conditional approval from days to hours in many cases. For a first-time homebuyer competing in a tight market, a same-day pre-approval letter can be the difference between winning and losing an offer.

Broader access to loan products. Platforms support loan types including Conventional, FHA, VA, USDA, Jumbo, Non-QM, and commercial loans with integrations to third-party services. This versatility means a broker using a full-featured platform can serve a first-time FHA buyer and a seasoned investor seeking a Non-QM product within the same system, without switching tools or losing data.

Accuracy and compliance. Manual data entry is where mortgage files break down. Errors in income figures, property addresses, or borrower Social Security numbers trigger delays that can push closing dates back by weeks. Integrated platforms reduce these errors by pulling data once and populating it across every form automatically. You can explore how compliance automation works within these platforms to understand the regulatory layer that protects both brokers and borrowers.

Additional benefits worth knowing:

- Real-time loan tracking. Borrowers see exactly where their file stands at every stage, which reduces the anxiety of waiting and the volume of "where are we?" calls to the broker's office.

- Marketing and lead management. Brokers gain built-in tools for email campaigns, referral tracking, and pipeline reporting, all connected to the same CRM that manages active loans.

- Transparent pricing comparisons. Borrowers can see rate options across multiple lenders side by side, which builds trust and supports informed decisions.

- Scalability. A broker managing 10 loans and a broker managing 100 loans can use the same platform. The system scales with the business without requiring additional staff for administrative tasks.

Pro Tip: As a borrower, ask your broker which platform they use and whether you will have direct access to a borrower portal. Direct portal access means you can upload documents securely, check status updates, and sign disclosures electronically without waiting for email attachments.

How to choose the right mortgage broker platform for your needs

Selecting a platform aligned with broker needs and business size determines whether the technology delivers real efficiency or just adds another layer of complexity. For borrowers evaluating brokers, asking the right questions about the tools a broker uses tells you a great deal about how organized and responsive they will be.

Here are the criteria that matter most:

- Integration scope. The platform must connect LOS, POS, CRM, and pricing in one system. A platform that handles origination but requires a separate CRM and a separate pricing tool is not a platform. It is three tools pretending to be one.

- Automation depth. Look for instant pre-approval generation, OCR document reading, automated status notifications, and compliance flagging. Each of these removes a manual step that would otherwise slow your file.

- Ease of use. A platform that requires two weeks of training to navigate basic tasks will not be used consistently. Brokers who find the interface cumbersome revert to workarounds, which defeats the purpose.

- Compliance tools. Mortgage lending is heavily regulated. The platform should maintain an up-to-date compliance knowledge base, generate required disclosures automatically, and create audit trails. Reviewing a mortgage compliance checklist alongside platform features helps identify gaps before they become violations.

- Loan type support. If you are a real estate investor who works with Non-QM or commercial products, confirm the platform handles those loan types natively, not through a workaround.

- Pricing and scalability. Platforms priced per loan or per user can become expensive quickly as volume grows. Understand the pricing model before committing, and confirm the platform can handle your projected volume without performance issues.

For borrowers, the practical takeaway is this: a broker using a well-integrated platform will ask for your documents once, give you a clear timeline, and communicate proactively. A broker working from disconnected tools will ask for the same document three times and go quiet for days. The platform a broker chooses reflects how they run their business.

Key takeaways

A mortgage broker platform is the single most important technology decision an independent broker makes, because it determines the speed, accuracy, and client experience of every loan they originate.

| Point | Details |

|---|---|

| Core definition | A mortgage broker platform integrates LOS, POS, CRM, and pricing into one connected system. |

| Human and software roles | Brokers provide judgment and relationships; platforms provide speed, data, and compliance support. |

| Top borrower benefit | Real-time tracking and automated pre-approvals give borrowers faster answers and greater transparency. |

| Automation and accuracy | OCR document processing and automated data population cut errors that delay closings. |

| Selection criteria | Evaluate integration scope, automation depth, compliance tools, and loan type support before choosing. |

Why the human element still defines the best platforms

I have spent over 20 years working inside mortgage operations as a processor, underwriter, loan originator, and systems consultant. I have seen every generation of mortgage technology, from the early LOS systems that barely talked to each other to the fully integrated platforms available today. My honest observation is this: the brokers who get the most out of these platforms are not the ones who trust the automation blindly. They are the ones who understand what the technology is doing and why.

The balance between automation and human underwriting is not a temporary compromise while technology catches up. It is the correct model. Automated decisioning gives borrowers early confidence and speeds the process. Human underwriting catches the nuances that algorithms miss, the self-employed borrower whose income structure is unusual, the investor whose property type falls outside standard guidelines. A platform that removes human review entirely is not more efficient. It is more fragile.

What I built with 1 Solution Mortgage Software came directly from watching brokers struggle with fragmented systems that were designed for banks, not independent professionals. The technology should work for the broker, not the other way around. When you see a broker who responds quickly, communicates clearly, and closes on time, there is almost always a well-integrated platform running behind the scenes. That is not a coincidence. You can read more about speeding up loan approvals through unified platform technology if you want to understand the mechanics in more depth.

The future of mortgage brokering is not automation replacing brokers. It is brokers using automation to serve more clients, more accurately, with less administrative friction. The platform is the infrastructure. The broker is still the professional.

— Omar Khamisa

See how 1 Solution Mortgage Software puts this into practice

If you are a broker who has felt the frustration of juggling disconnected tools, or a borrower who has experienced the delays that come from a disorganized process, there is a better way.

1 Solution Mortgage Software was built from the trenches of real mortgage operations by a team that has lived every problem the platform solves. The all-in-one system brings together LOS, POS, CRM, pricing, compliance, marketing, and communication tools in one connected ecosystem designed specifically for independent mortgage professionals. No outside investors. No hidden agendas. Just technology that works the way brokers actually work. Explore the platform and start a free trial to see the difference a purpose-built system makes.

FAQ

What is a mortgage broker platform in simple terms?

A mortgage broker platform is software that manages the entire mortgage process in one place, connecting loan origination, borrower applications, client communication, and lender pricing into a single workflow.

How does a mortgage broker platform differ from a direct lender?

A mortgage broker platform is a tool used by independent brokers to shop loans across multiple lenders simultaneously. A direct lender uses its own funds and its own criteria, offering only its own products without comparison.

What does a mortgage broker do that the platform cannot?

A licensed mortgage broker provides professional judgment, borrower advocacy, and lender negotiation. The platform automates data management and workflow but cannot replace the human expertise required for complex underwriting decisions.

What are the main benefits of mortgage broker platforms for first-time homebuyers?

Platforms give first-time buyers faster pre-approvals, real-time loan tracking, and access to a wider range of loan products including FHA and VA options, all managed through a single borrower portal.

How do I know if my broker is using a good mortgage broker platform?

Ask whether you will have access to a borrower portal for document uploads and status tracking. A broker using a well-integrated platform will ask for your documents once and communicate proactively throughout the process.