Mortgage file submission is the process of collecting, organizing, validating, and delivering all required loan documents to underwriting for a credit decision. In the industry, this workflow is formally called the loan file packaging and submission process, though most loan officers simply call it "file submission." Understanding mortgage file submission explained in full means knowing every stage from document intake through automated underwriting system (AUS) delivery. Get any stage wrong and you face rework, delays, and frustrated borrowers. Get it right and you close faster, with fewer conditions, and a cleaner audit trail.

What is the end-to-end mortgage file submission workflow?

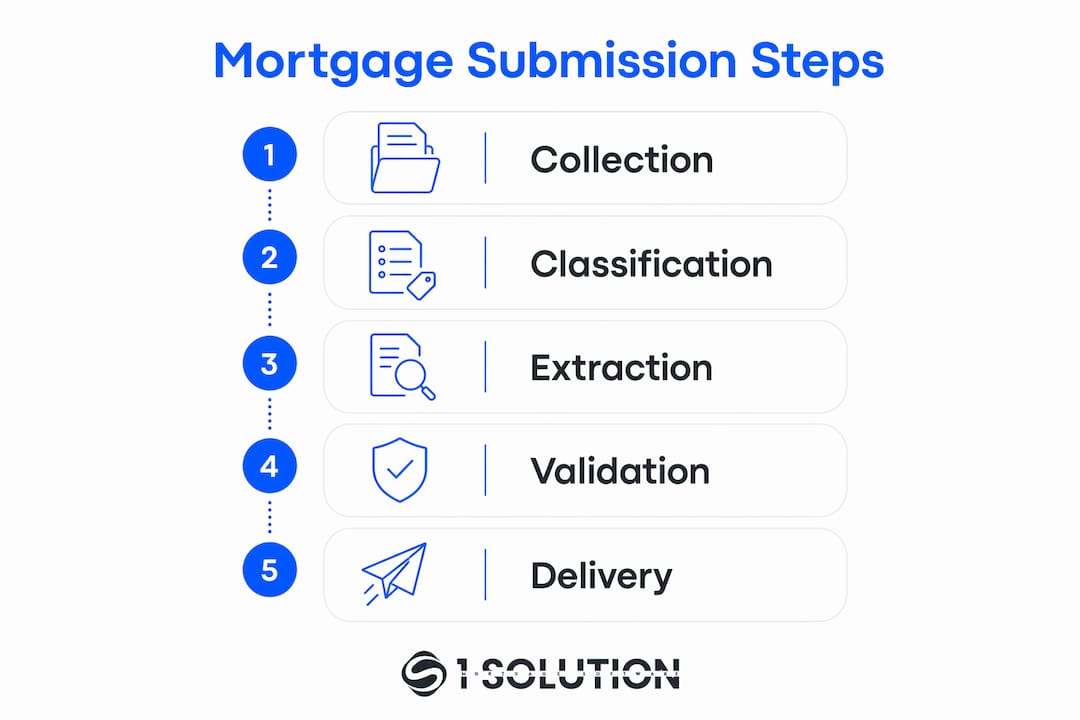

Mortgage file submission is a structured, multi-stage workflow. Documents arrive via portals, email, scanned images, and multi-page bundles before they are classified, extracted into structured data fields, and validated for accuracy. Each stage depends on the one before it. Skip a step or rush through it and the downstream consequences compound fast.

Here is how the full workflow runs from intake to underwriting delivery:

- Document intake. Borrowers submit files through a borrower portal, email, or broker package. The intake channel matters because unstructured email attachments require far more manual sorting than portal uploads with predefined checklists.

- Document classification. Every file gets labeled by type: W-2, pay stub, bank statement, appraisal, title commitment, and so on. Accurate classification splits combined PDFs and assigns correct labels, which then direct the extraction and validation processes downstream. Misclassification at this stage populates wrong data schemas and triggers expensive manual reviews.

- Data extraction. Once classified, data fields are pulled from each document. Intelligent Document Processing (IDP) platforms go beyond basic OCR by understanding document context, so a gross income figure on a 1003 is not confused with a net figure on a pay stub.

- Cross-document validation. Validation is the final quality gate, confirming data correctness and consistency across all documents. Income on the 1003 must match the W-2. The property address on the appraisal must match the purchase contract. Failures here cause the most rework before underwriting.

- AUS submission. After credit review, the file is submitted to Fannie Mae Desktop Underwriter or Freddie Mac Loan Product Advisor. The AUS findings determine eligibility, required documentation, and any conditions.

- eFolder management. All documents remain in electronic folders during processing and condition management. Encompass users store everything in the eFolder, creating a single source of truth for processors, underwriters, and compliance teams.

Pro Tip: Submit to AUS as early as possible after credit review. Early AUS submission surfaces eligibility issues before you have invested hours building out the full file, turning a potential closing-day problem into an early, fixable decision.

How do modern technologies improve mortgage document submission?

Technology has fundamentally changed what loan officers can accomplish in a single day. The mortgage document process used to mean printing, scanning, emailing, and manually re-keying data into a Loan Origination System (LOS). Modern platforms eliminate most of that friction.

Here is where the biggest gains come from:

- Intelligent Document Processing (IDP). IDP automatically classifies mortgage documents by type, extracts data fields with context, validates data internally and across documents, and integrates directly with LOS platforms. The difference between IDP and basic OCR is context awareness. IDP knows that a 1099 and a W-2 both report income but require different extraction schemas.

- Direct LOS integration. When IDP feeds extracted data directly into Encompass or a comparable LOS, manual re-keying disappears. That removes a primary source of data entry errors and speeds the mortgage application submission timeline significantly.

- Secure borrower portals. Borrowers receive a unique upload link without needing an account, upload documents from any device, and the dashboard tracks received versus missing items in real time. Automated reminders chase borrowers for outstanding documents so loan officers do not have to.

- Security that email cannot match. Modern portals use AES-256 encryption, HTTPS/TLS transfer, audit trails, and link revocation. Email offers no encryption guarantees after delivery and has no audit logging. For sensitive borrower data, portals are not optional; they are the professional standard.

- Early AUS submission. Submitting to AUS after credit review speeds loan processing by catching eligibility issues earlier. This single practice alone can prevent the scenario where a file reaches underwriting only to bounce back on a guideline issue that was always there.

- Real-time validation. Automated validation flags discrepancies the moment they appear, replacing slow manual review cycles and reducing rework hours before the file ever reaches an underwriter.

For loan officers looking to cut time on repetitive submission tasks, the combination of IDP, portal-based intake, and direct LOS integration is the most effective setup available today.

Common challenges in mortgage file submission and how to avoid them

Every loan officer has lived through at least one of these. Knowing where the process breaks down is the first step toward preventing it.

- Unstructured or incomplete documents. Borrowers send multi-page PDFs with tax returns, bank statements, and pay stubs merged into a single file. Without automated classification, a processor must manually split and label each page. This is slow, error-prone, and scales poorly during volume spikes.

- Manual re-keying errors. Typing data from a document into an LOS introduces transcription mistakes. A transposed digit in an income figure or a misspelled name on a title document can trigger a condition that delays closing by days.

- Chasing missing documents without tracking. When document collection happens over email, there is no central record of what has been received and what is outstanding. Loan officers spend significant time on follow-up calls and emails that a portal with automated reminders would handle automatically.

- Late-stage validation failures. When cross-document validation happens manually and late in the process, discrepancies surface at the worst possible time. An income figure that does not match across the 1003, W-2, and pay stub discovered the day before closing creates a rework loop that affects everyone on the transaction.

- Compliance gaps in the audit trail. Files submitted without a clear, timestamped record of who uploaded what and when create compliance exposure that regulators and lenders will find.

Pro Tip: Build a standardized mortgage file checklist for each loan type you originate. A purchase conventional file has different requirements than a cash-out refinance or an FHA loan. A type-specific checklist given to borrowers at application cuts missing document follow-up by a measurable margin.

The most overlooked fix is training. Teams that understand why classification must precede extraction, and why validation failures are so costly, handle exceptions better and escalate problems earlier.

How to implement an efficient mortgage file submission workflow

Improving your submission process does not require replacing everything at once. A phased approach works well for most operations.

- Audit your current intake channels. Map where documents come from today: email, fax, borrower portal, or broker package. Identify which channels create the most manual work and prioritize those for replacement first.

- Adopt a borrower portal with automated reminders. Replace email-based document collection with a portal that gives borrowers a checklist, a secure upload link, and automated follow-up. This alone removes the most time-consuming manual task in most loan officers' days.

- Implement IDP with direct LOS integration. Connect your document processing platform directly to your LOS so extracted data flows in without manual re-keying. Platforms that integrate with Encompass or similar systems reduce data entry errors at the source.

- Submit to AUS early. After completing the credit review, run the file through Fannie Mae Desktop Underwriter or Freddie Mac Loan Product Advisor before building out the full condition package. Early AUS submission identifies borrower eligibility issues sooner, saving hours of work on files that would otherwise bounce back.

- Monitor with dashboards and audit trails. Use your LOS or pipeline management tool to track submission progress, outstanding conditions, and document status in real time. A dashboard view of your full pipeline is the difference between proactive management and reactive firefighting.

The table below summarizes the key implementation steps and their primary benefit:

| Step | Primary benefit |

|---|---|

| Audit intake channels | Identifies highest-friction document sources |

| Deploy borrower portal | Eliminates manual document chasing |

| Integrate IDP with LOS | Removes re-keying errors at data entry |

| Submit to AUS early | Surfaces eligibility issues before full file build |

| Monitor with dashboards | Enables proactive pipeline management |

For teams working to speed up loan approvals, the combination of early AUS submission and automated validation is the highest-leverage change available in 2026.

Key takeaways

Mortgage file submission is a sequential workflow where classification, extraction, and validation must each succeed before underwriting delivery, and automation at every stage is the most reliable way to reduce errors and close faster.

| Point | Details |

|---|---|

| Classification comes first | Misclassifying documents corrupts extraction and validation, causing expensive manual rework. |

| Validation is the costliest failure point | Cross-document discrepancies found late create rework loops that delay closings and frustrate borrowers. |

| Portals beat email for security | AES-256 encryption, audit trails, and automated reminders make portals the professional standard for document collection. |

| Early AUS submission saves time | Running AUS after credit review catches eligibility issues before you invest hours building the full file. |

| Dashboards enable proactive management | Real-time pipeline visibility turns reactive firefighting into controlled, predictable closings. |

The part most loan officers skip until it costs them

I have spent over 20 years working mortgage operations from the processor seat, the underwriter seat, and the originator seat. The single most consistent pattern I have seen across all of it is this: teams invest in technology at the front end of the process and ignore validation until something breaks.

Most shops will adopt a borrower portal, maybe even an IDP tool, and feel like the problem is solved. But validation is where the real money is lost. A file that looks complete at intake can still carry income discrepancies, address mismatches, or date inconsistencies that only surface when someone runs a cross-document check. If that check happens manually and late, you are looking at a rework loop that costs days, not hours.

The other thing I would push back on is the idea that automation removes the need for human judgment. It does not. Automation handles the repetitive, high-volume work so your experienced processors and underwriters can focus on the exceptions that actually require expertise. A flagged discrepancy still needs a human to determine whether it is a data entry error, a legitimate inconsistency, or a red flag. The goal is not to remove people from the process. The goal is to make sure people are working on the problems only they can solve.

The future of mortgage file submission is AI-driven document processing with tighter LOS integration and borrower-friendly portals that make document collection feel effortless. But the teams that will benefit most are the ones that build the right habits now: clear checklists, early AUS submission, and a validation step that happens before the file leaves your desk.

— Omar Khamisa

How 1 Solution Mortgage Software supports your file submission process

1 Solution Mortgage Software was built by mortgage professionals who have lived through every stage of the file submission process. The platform supports end-to-end loan pipeline management, from document intake through underwriting delivery, with tools designed specifically for independent brokers and loan officers.

1 Solution integrates with LOS and AUS tools, offers borrower portals with secure upload links and real-time tracking, and includes automated reminders and audit logs that keep your pipeline moving without constant manual follow-up. If you are ready to bring your document process under control, explore 1 Solution Mortgage Software and see how a platform built from real industry experience handles the problems you deal with every day.

FAQ

What is mortgage file submission?

Mortgage file submission is the process of collecting, classifying, extracting, validating, and delivering all required loan documents to an underwriter or automated underwriting system for a credit decision. It covers every step from borrower document intake through final AUS submission.

What documents are needed for mortgage file submission?

A standard mortgage file includes the 1003 loan application, W-2s, pay stubs, bank statements, tax returns, the appraisal, title commitment, purchase contract, and all required disclosures. The exact list varies by loan type, lender, and AUS findings.

Why does document classification matter in the submission process?

Classification must precede extraction and validation because misclassification populates the wrong data schemas, causes cross-document validation failures, and triggers manual reviews that delay underwriting. Accurate classification is the foundation every downstream step depends on.

How does early AUS submission improve the mortgage process?

Submitting to AUS early after credit review identifies borrower eligibility issues before you have built out the full condition package, saving significant processing time and preventing late-stage surprises.

Are borrower portals more secure than email for document collection?

Yes. Portals use AES-256 encryption, HTTPS/TLS transfer, audit trails, and link revocation. Email provides no encryption guarantees after delivery and has no audit logging, making portals the only defensible choice for sensitive borrower data.