A mortgage origination training course is structured education that teaches individuals how to originate residential mortgage loans, covering the full workflow from application to closing, compliance obligations, documentation requirements, and product knowledge. These courses exist in two distinct forms: licensing education required by the SAFE Act and operational training designed to sharpen production skills. The Mortgage Bankers Association's School of Loan Origination (SOLO) and providers like TapMoney Institute represent the two ends of this spectrum. Understanding which type you need, and when, is the most important decision you will make when choosing a program.

What is a mortgage origination training course and what does it cover?

A mortgage origination training course teaches the full origination workflow, from taking a borrower application through underwriting, pricing, and closing a residential loan. The industry term for this category of education is "MLO training" or "loan originator education," and it spans both mandatory pre-licensure courses and voluntary professional development programs. Knowing the difference between these two tracks saves you time and money before you enroll.

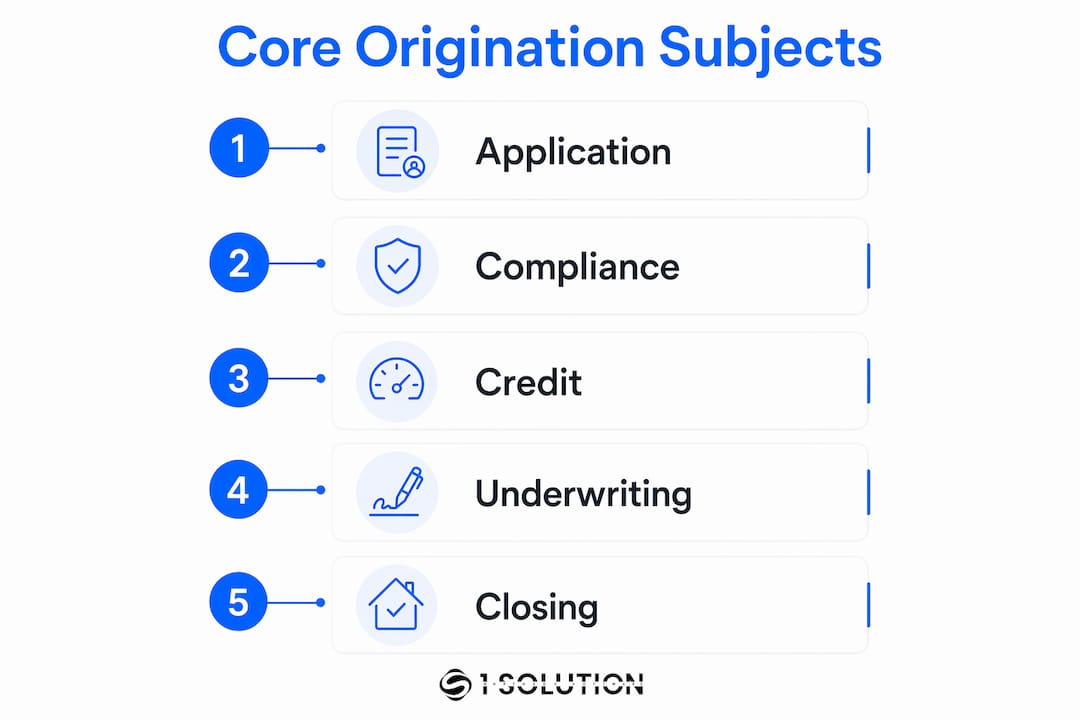

Core subjects taught in origination courses

Most mortgage origination training programs cover the following subject areas:

- Loan origination workflow. The sequence from the initial borrower interview through application, processing, underwriting, and closing. Understanding each handoff point reduces errors and speeds up file movement.

- Federal compliance. The Truth in Lending Act (TILA), the Real Estate Settlement Procedures Act (RESPA), and SAFE Act components are standard curriculum. Compliance knowledge protects both the borrower and the originator from regulatory penalties.

- Documentation. Courses cover the Uniform Residential Loan Application (Form 1003), the Loan Estimate, and tax transcript requests using Form 4506-T. Knowing exactly what each document proves and when to request it is a skill that separates efficient originators from slow ones.

- Product knowledge. Conventional, FHA, VA, USDA, jumbo, and non-traditional loan products each carry distinct guidelines. Originators who understand product differences can match borrowers to the right loan on the first attempt rather than switching products mid-process.

- Pricing and rate locks. Courses introduce how lenders price loans, how margin and points work, and when to lock a rate. This knowledge directly affects a borrower's cost and an originator's credibility.

Pro Tip: Before enrolling in any program, request a full course syllabus and confirm it addresses both compliance theory and practical documentation exercises. A course that only covers law without applying it to real loan files will leave you underprepared on day one.

The MBA's SOLO program delivers 12 two-hour webinars with instructor guidance across these topics, making it one of the most structured operational programs available in 2026. That format matters because instructor-led courses allow you to ask questions about real scenarios, not just memorize definitions.

How do licensing requirements connect to origination training?

Pre-licensure mortgage origination training is defined by the SAFE Act, which mandates a 20-hour national course before a candidate can sit for the NMLS licensing exam. This is not optional, and the hour breakdown is federally prescribed.

The 20 hours are divided as follows:

- 3 hours of federal law. Covers the SAFE Act itself, TILA, RESPA, and the Equal Credit Opportunity Act (ECOA).

- 3 hours of ethics. Focuses on fraud prevention, consumer protection, and fair lending obligations.

- 2 hours of non-traditional mortgage lending. Addresses products like interest-only loans, negative amortization, and adjustable-rate structures.

- 12 hours of electives. States and NMLS-approved providers fill this time with additional federal content, state-specific law, or supplemental exam preparation.

Most states also require additional state-specific education hours on top of the national 20. Georgia, for example, requires candidates to complete a state-approved course that satisfies both NMLS and Georgia Department of Banking requirements simultaneously.

"Candidates should prioritize courses that are NMLS-approved and align with their specific state's requirements to ensure licensing success." — TapMoney Institute

This distinction matters because not every course marketed as "mortgage training" qualifies for NMLS credit. A course can be well-designed and informative but still fail to count toward your license if the provider is not NMLS-approved. Always verify approval status before purchasing. You can check provider status directly through the NMLS Resource Center.

Licensing education and operational training serve completely different purposes. Confusing the two leads candidates to misprioritize their preparation, spending hours studying for an exam when they actually need production skills, or vice versa. Licensing gets you in the door. Operational training determines how well you perform once you are inside.

What types of origination training exist beyond licensing?

Once you hold your license, the real education begins. Operational and sales-focused mortgage training programs address the production skills that licensing courses never touch.

| Course Type | Primary Focus | Best For |

|---|---|---|

| MBA School of Loan Origination (SOLO) | Workflow, compliance, documentation, risk reduction | New and mid-career originators, processors, assistants |

| Pulse Sales Trainings: Mortgage Purchase Origination Selling | Sales workflow, marketing strategy, purchase transaction skills | Licensed originators building purchase volume |

| Role-based operational courses | Processor workflows, branch manager oversight, assistant coordination | Support staff and team leads |

| Specialized market courses | Later-life lending, jumbo products, non-QM origination | Experienced originators targeting niche segments |

The MBA's SOLO program targets mortgage loan originators, assistants, and processors with an instructor-led format, which means the training applies to an entire production team, not just the originator. That is a significant advantage for brokers who want consistent file quality across their operation.

Pulse Sales Trainings offers a 60-minute purchase origination course focused entirely on sales skills for licensed originators. The contrast with SOLO is instructive. SOLO builds process discipline. Pulse builds revenue skills. Both are necessary at different career stages.

Pro Tip: If you manage a team, consider enrolling your loan officer assistants and processors in the same operational training program you use. Shared vocabulary and shared process knowledge reduce miscommunication and cut file touches significantly.

Effective operational origination training connects compliance requirements directly to production goals such as reducing repurchase risk and minimizing rework. This is the key insight most originators miss. Compliance is not separate from production. It is the mechanism that protects production quality. Courses that teach compliance in isolation from daily file management produce originators who know the rules but still make expensive mistakes.

For a practical look at how loan officer onboarding programs translate training into day-one performance, the structure of operational courses becomes even clearer.

How to choose the right origination training course for your goals

Selecting the right mortgage certification course depends on where you are in your career and what outcome you need. Here is how to think through the decision:

- Identify your immediate goal. If you are not yet licensed, your only priority is an NMLS-approved pre-licensure course that meets your state's hour requirements. Everything else is secondary until you pass the SAFE MLO exam.

- Verify NMLS approval and state alignment. Not all courses count equally toward licensing. Confirm the provider is listed on the NMLS-approved course catalog before enrolling. A course that does not qualify wastes both time and money.

- Choose the right format for your schedule. Instructor-led courses offer real-time Q&A and accountability. Self-paced courses offer flexibility. If you are preparing for the NMLS exam, instructor-led formats tend to produce better retention of compliance material.

- Look for courses that connect compliance to production. The best mortgage training programs explicitly link compliance topics to everyday operational goals, improving loan quality and reducing costs. A course that teaches TILA without explaining how a disclosure error triggers a repurchase request is incomplete.

- Factor in ongoing education. Licensing is not a one-time event. Most states require annual continuing education hours through NMLS-approved providers. Build a habit of structured learning from the start rather than treating education as a box to check.

One fact that surprises many candidates: becoming a mortgage loan originator requires no college degree. The requirements are age 18 or older, completion of required education hours, and passing the SAFE MLO national test. This means the barrier to entry is lower than most people assume, and the quality of your training becomes the primary differentiator between you and other new originators.

For a deeper look at how mortgage scenario analysis applies the product knowledge taught in these courses, the connection between training and real-world loan decisions becomes concrete.

Key takeaways

Mortgage origination training courses fall into two categories: NMLS-approved pre-licensure education and operational production training, and choosing the wrong type for your current career stage is the most common and costly mistake new originators make.

| Point | Details |

|---|---|

| Two distinct course types | Pre-licensure and operational training serve different goals; identify which you need before enrolling. |

| SAFE Act mandates 20 hours | Federal law requires 20 hours of pre-licensure education covering federal law, ethics, and non-traditional lending. |

| NMLS approval is non-negotiable | Only NMLS-approved courses count toward licensing; verify provider status before purchasing any program. |

| Compliance connects to production | The strongest programs teach compliance in the context of daily file management, not as abstract theory. |

| No degree required | Licensing requires education hours and exam passage only, making training quality the primary differentiator. |

Training is not the finish line. It is the starting point.

I have spent over 20 years working across mortgage operations as a processor, underwriter, originator, and systems consultant. The pattern I see most often is this: people treat licensing education as the destination rather than the entry ticket. They complete their 20 hours, pass the NMLS exam, and assume they are ready to originate. They are not.

Licensing tells regulators you understand the rules. It does not tell borrowers you can close their loan efficiently and without errors. The originators I have watched build durable careers are the ones who pursued operational training after licensing, not instead of it. They enrolled in programs like MBA's SOLO not because they had to, but because they understood that process discipline is what separates a 10-loan-per-month originator from a 3-loan-per-month originator.

There is also a misconception I want to address directly. Many people believe that mortgage origination training is primarily about memorizing regulations. It is not. The best training teaches you how regulations connect to file quality, borrower experience, and your own liability. When you understand why a disclosure requirement exists, you stop treating it as a bureaucratic hurdle and start treating it as a quality control step. That shift in mindset is worth more than any certification.

My honest advice: complete your licensing education with an NMLS-approved provider, then immediately identify one operational program that addresses your weakest production skill. Do not wait until you have a problem to invest in training. By then, the cost is already higher than the course fee.

— Omar Khamisa

How 1 Solution Mortgage Software supports you after training

Training gives you the knowledge. The right technology gives you the environment to apply it consistently.

1 Solution Mortgage Software was built by mortgage professionals who have sat in the same seat you are in now. Our platform brings together pricing, CRM, POS, LOS, compliance, and communication tools into one connected system designed specifically for independent mortgage professionals. After completing your origination training, the last thing you need is fragmented software that creates the exact errors your training taught you to avoid. Explore 1 Solution Mortgage Software to see how the right technology reinforces the compliance and workflow discipline you worked to build.

FAQ

What is a mortgage origination training course?

A mortgage origination training course is structured education that teaches individuals how to originate residential mortgage loans, covering workflow, compliance, documentation, product knowledge, and pricing. These courses exist as either NMLS-approved pre-licensure programs or operational training for licensed professionals.

How many hours of pre-licensure training does the SAFE Act require?

The SAFE Act requires 20 hours of pre-licensure education, including 3 hours of federal law, 3 hours of ethics, 2 hours of non-traditional lending, and 12 hours of electives. Many states require additional state-specific hours on top of the national requirement.

Do I need a college degree to become a mortgage loan originator?

No. Becoming a mortgage loan originator requires only that you are 18 or older, complete the required education hours, and pass the SAFE MLO national exam. A college degree is not required.

What is the difference between licensing education and operational training?

Licensing education satisfies NMLS requirements and prepares you for the SAFE MLO exam. Operational training, such as the MBA's School of Loan Origination, focuses on production skills, process discipline, and connecting compliance knowledge to daily file management.

How do I verify that a mortgage training course counts toward my license?

Confirm the provider is listed in the NMLS-approved course catalog before enrolling. State-specific requirements vary, so also check your state's licensing authority to verify that the course meets both national and state hour requirements.