A mortgage team structure is the deliberate division of roles and responsibilities within a mortgage operation to maximize efficiency, compliance, and throughput. This is not simply a headcount decision. It is a strategic framework that segments tasks by licensing requirements, decision complexity, and workflow stage. Role design by task complexity is what separates high-performing brokerages from those stuck in constant rework. When you get the mortgage team structure explained correctly, every loan moves faster, errors drop, and your licensed staff spend time on work only they can legally do.

What are the primary roles in a mortgage team?

Mortgage team roles fall into two clear categories: licensed roles that require legal authority to make decisions, and operational roles that execute process-driven tasks under supervision. Confusing these two categories is the most common and costly structural mistake in the industry.

Licensed and decision-making roles include:

- Loan Originator (MLO): The client-facing professional responsible for taking applications, advising borrowers, and signing off on compliance-sensitive decisions. This role owns the borrower relationship from application through closing.

- Underwriter: The final decision authority on loan approval. Underwriters assess risk, verify compliance with investor guidelines, and issue conditions. No one else in the team holds this authority.

- Branch Manager or Production Lead: Oversees the pipeline, manages MLO performance, and maintains regulatory accountability for the operation.

Operational and execution roles include:

- Loan Processor: The operational engine of the team. Processors verify income and assets, request missing documents, track deadlines, and prepare complete files for underwriting review. Their accuracy directly determines how fast underwriting can move.

- Closing Coordinator: Monitors milestone checklists, manages appointment scheduling, communicates with title and escrow, and prepares escalation logs when issues arise. Closing coordinators operate under licensed supervision to maintain compliance and timeliness.

- Trailing Document Specialist: A post-closing role that is often overlooked but never optional. Trailing specialists coordinate with title companies, escrow agents, and county recorders to obtain missing documents and package files for investor delivery.

- Offshore or Nearshore Support Staff: Integrated operational roles that handle defined, lower-risk tasks such as document collection, data entry, and status updates. Specialized offshore roles can reduce operational costs by 50–60% while improving consistency and turnaround time.

Pro Tip: Never assign a single person to cover both origination and processing on the same file. The role overlap creates compliance risk and slows the pipeline. Separate these functions even in a two-person shop.

How does task specialization speed up mortgage workflows?

Task specialization works because it eliminates context switching. When a loan officer also chases documents, orders appraisals, and answers processor questions, they lose the focused time needed to originate new business. The same logic applies to every role in the chain.

The most effective mortgage teams design roles around decision rights and file artifacts, not job titles. A decision right defines who owns a specific loan milestone and who must sign off before the file advances. This approach, described in detail by PeoplePartners' workforce re-engineering framework, increases throughput and reduces compliance gaps caused by duplicated or skipped checks.

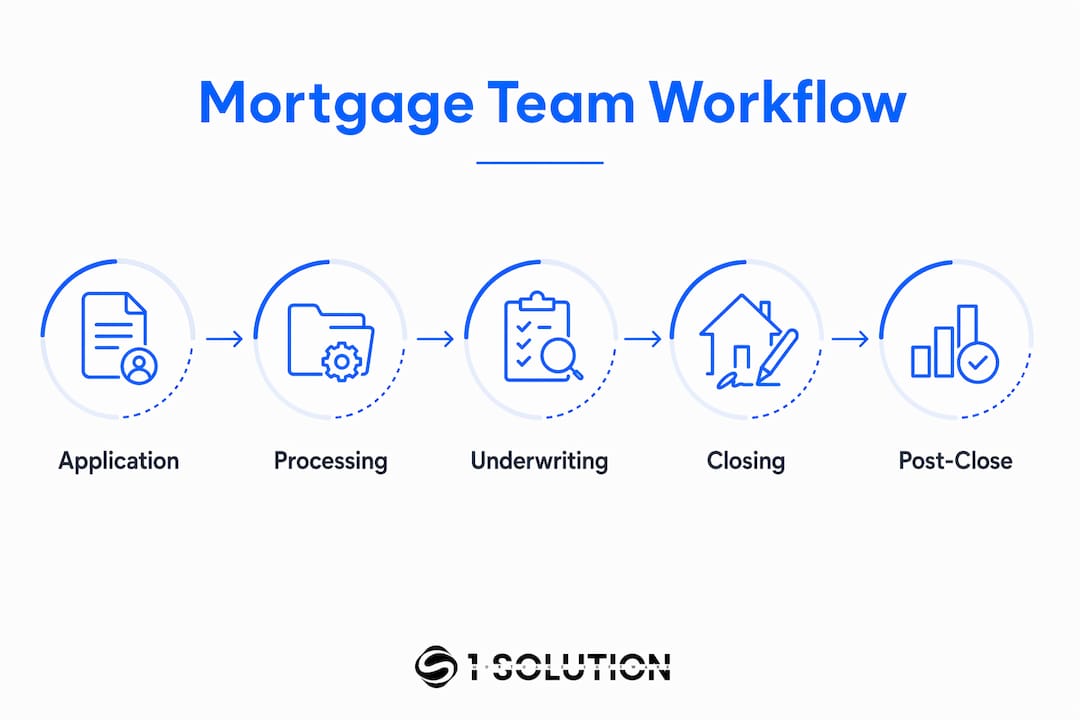

Here is how a well-structured handoff sequence looks in practice:

- Application intake: MLO collects borrower information, runs credit, and issues a pre-qualification. File is handed to the processor with a complete checklist.

- Processing stage: Processor orders verifications, collects documents, and confirms file completeness against an SLA threshold before advancing.

- Underwriting submission: File is submitted only when completeness triggers are met. Automating internal handoffs while retaining licensed sign-off can reduce pre-approval time from days to hours.

- Conditional approval: Underwriter issues conditions. Processor clears conditions with borrower and third parties.

- Closing coordination: Closing coordinator confirms final numbers, schedules signing, and tracks document return.

- Post-closing: Trailing document specialist audits the file, obtains missing items, and ships the complete package to the investor.

| Workflow Stage | Role Owner | Key Artifact |

|---|---|---|

| Application | Loan Originator | 1003, credit report |

| Processing | Loan Processor | Verified file package |

| Underwriting | Underwriter | Approval or denial letter |

| Closing | Closing Coordinator | Closing disclosure, signed docs |

| Post-Closing | Trailing Specialist | Investor delivery package |

Operational efficiency improves when file completeness triggers and SLA thresholds automate handoffs and reduce idle time between stages. Idle time is where pipelines stall and borrowers lose confidence.

Pro Tip: Set a hard SLA rule: no file advances to underwriting without 100% document checklist completion. This single rule eliminates the most common cause of underwriting suspensions.

What organizational structures support compliance and clarity?

Regulators do not just want to see that you have people. They want to see that you know who is responsible for what. A clear mortgage department layout satisfies both internal management needs and external regulatory scrutiny.

Regulators prefer a Q&A memo format that maps four key areas: compliance oversight, production and sales management, loan processing and operations, and financial controls. A one-page document answering who owns each area and who they report to is often more useful than a complex org chart.

The table below compares two common structural models used in brokerages and small lenders:

| Structure Type | Best For | Compliance Clarity | Scalability |

|---|---|---|---|

| Flat (MLO + Processor) | Solo brokers, 1–3 person shops | Moderate | Low |

| Layered (MLO, Processor, Coordinator, Underwriter) | Growing brokerages | High | High |

| Hub and Spoke (Central ops team + MLO pods) | Multi-branch operations | Very High | Very High |

Role clarity speeds onboarding and reduces errors because team members know exactly what they own and when to escalate. A new processor who joins a team with a defined checklist and clear escalation path ramps up in days, not weeks. A new processor joining a team where "everyone does everything" takes months to become productive and makes more mistakes along the way.

The mortgage compliance setup checklist approach works well here. Assign each compliance function to a named role, document the reporting line, and review it annually or when regulations change.

Which tools support mortgage team collaboration and transparency?

Mortgage team collaboration explained at its core is about visibility. Every team member needs to see where a file stands, what is missing, and who owns the next step. Without that visibility, files stall and borrowers get frustrated.

The primary technology categories that support this are:

- Loan Origination System (LOS): The central record of every loan. An LOS like Encompass or a purpose-built platform tracks file status, documents, and conditions in one place. Every role interacts with the LOS daily.

- CRM Platform: Manages borrower communication, follow-up sequences, and pipeline reporting. A CRM keeps MLOs accountable for touchpoints without relying on memory or spreadsheets. The mortgage touchpoint strategy built into a CRM directly supports borrower retention and referral generation.

- Compliance Software: Tracks regulatory requirements, disclosure deadlines, and audit trails. This is non-negotiable for any licensed operation.

- Task and Milestone Tracking Tools: Whether built into the LOS or layered on top, task tracking gives processors and coordinators a live view of what is complete, what is pending, and what is overdue.

- Communication Platforms: Secure messaging tools that keep borrower and third-party communication inside a documented system rather than scattered across personal email and text threads.

Mortgage team transparency best practices center on one principle: every handoff must leave a record. When a processor sends a file to underwriting, that action should trigger a timestamp, a notification, and a status update visible to the MLO and the borrower. Layered operational boundaries aligned with licensing levels prevent errors by ensuring only licensed professionals make compliance and underwriting decisions while operational staff support with defined, documented tasks.

For teams integrating offshore support, digital transparency becomes even more critical. Offshore staff need access to the same task boards, checklists, and communication threads as in-house staff. The mortgage team collaboration platforms comparison matters most when you are deciding which tools can support distributed teams without creating information silos.

Key takeaways

A mortgage team structure built on decision rights, role specialization, and milestone ownership is the most direct path to faster closings, fewer errors, and sustainable compliance.

| Point | Details |

|---|---|

| Design by decision rights | Assign each loan milestone to a specific role, not a general title, to prevent overlap and compliance gaps. |

| Separate licensed from operational roles | Licensed staff handle judgment-heavy decisions; operational staff execute defined, process-driven tasks. |

| Automate handoffs with human sign-off | Use file completeness triggers and SLA thresholds to advance files automatically, with licensed approval at key stages. |

| Document structure for regulators | A Q&A memo mapping compliance, sales, processing, and financial control ownership satisfies most regulatory inquiries. |

| Transparency tools are non-negotiable | Every handoff must leave a timestamped record visible to all relevant team members to maintain accountability. |

Why most mortgage teams are structured backwards

I have spent over 20 years inside mortgage operations, working as a processor, underwriter, loan originator, and systems consultant. The single most consistent problem I have seen is not a lack of talent. It is a lack of structure. Most mortgage teams are built reactively. Someone gets busy, so they hire a person and hand them whatever is overflowing. That person becomes a generalist by accident, and the team never recovers its efficiency.

The conventional wisdom says to hire experienced people and trust them to figure it out. I disagree. Experience matters, but structure matters more. Team members perform better when they understand their ownership and have clear escalation pathways. That is not a soft management principle. It is a measurable operational fact.

The "all-in-one" role is the biggest trap in this industry. When one person originates, processes, and coordinates closing on the same file, you get faster movement on easy loans and complete chaos on complex ones. The complexity is where you lose money and where compliance risk lives.

My practical advice: draw your org chart before you hire your next person. Map the decision rights first. Decide who owns each loan artifact at each stage. Then hire to fill the gaps in that map, not to fill a seat. If you are integrating offshore support, treat those roles with the same rigor. Define their tasks, their boundaries, and their escalation paths in writing before day one.

— Omar Khamisa

How 1 solution mortgage software supports your team structure

Building the right structure is only half the work. The other half is giving your team the tools to execute it consistently.

1 Solution Mortgage Software was built from the ground up by mortgage professionals who have worked every role in this article. The platform connects your LOS, CRM, compliance tracking, POS, and communication tools into one system so your team always knows where every file stands. Role-based access controls mean each team member sees exactly what they need and nothing they do not. Milestone tracking and automated handoff notifications keep your pipeline moving without manual follow-up. If you are ready to give your team the operational foundation it deserves, 1 Solution Mortgage Software is built for exactly that.

FAQ

What is a mortgage team structure?

A mortgage team structure is the organized division of roles and responsibilities within a mortgage operation, segmented by licensing requirements, decision authority, and workflow stage to maximize efficiency and compliance.

What are the core roles in a mortgage team?

The core roles are loan originator, loan processor, underwriter, closing coordinator, and trailing document specialist. Each role owns specific file artifacts and milestones at distinct stages of the loan process.

How does role specialization improve mortgage team efficiency?

Role specialization eliminates context switching and reduces errors by ensuring each team member focuses on a defined set of tasks. Specialized role design increases throughput and protects licensed staff for judgment-heavy decisions.

What tools do mortgage teams use for collaboration?

Mortgage teams rely on a combination of LOS platforms, CRM systems, compliance software, and task tracking tools. The most effective setups integrate these into a single connected system to maintain milestone visibility and handoff accountability.

How should a mortgage team document its structure for regulators?

A one-page Q&A memo mapping compliance, sales, processing, and financial control ownership with clear reporting lines satisfies most regulatory requests for an organizational structure or business plan.