A mortgage payment is defined by four core components known as PITI: principal, interest, taxes, and insurance. Understanding the mortgage payment breakdown explained in full means knowing exactly where each dollar goes every month. Most borrowers see one number on their statement and assume it is simple. It is not. PITI mechanics, escrow adjustments, private mortgage insurance (PMI), and closing costs all shape what you actually pay. This guide covers every component in plain language so you can budget with confidence and avoid the surprises that catch most first-time buyers off guard.

What is the mortgage payment breakdown explained?

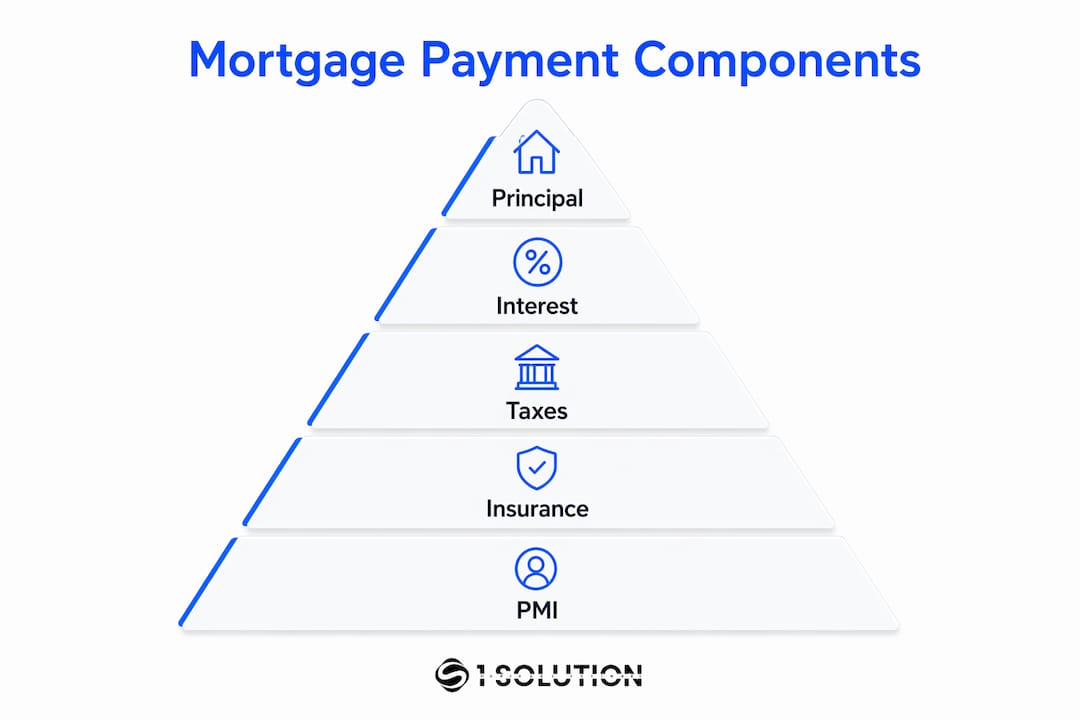

A mortgage payment consists of four main components: principal, interest, taxes, and insurance, collectively called PITI. If your down payment is less than 20%, PMI is added as a fifth cost. Each component serves a different purpose, and each one can change independently over the life of your loan. Knowing the split is the foundation of understanding mortgage payments.

What is principal and how does it impact your mortgage?

Principal is the portion of your payment that directly reduces your loan balance. Every dollar applied to principal builds home equity. On a $300,000 loan, paying down principal is the only way to own more of your home outright.

The catch is that amortization shifts the split silently over time. Early in a 30-year mortgage, the vast majority of each payment goes to interest, not principal. The payment amount stays constant, but the allocation changes every single month. By the final years of the loan, most of each payment reduces the balance directly.

Here is what you need to know about principal:

- Loan balance reduction: Each payment lowers the outstanding balance by the principal portion only.

- Equity growth: Principal payments convert debt into ownership stake in your home.

- Amortization effect: The principal share of each payment grows gradually as the loan balance decreases.

- Extra payments: Making additional principal payments shortens the loan term and reduces total interest paid.

Pro Tip: In the first five years of a 30-year mortgage, most of your payment covers interest. If you want to build equity faster, even one extra principal payment per year can meaningfully shorten your payoff timeline.

How does interest work in your mortgage payment?

Interest is the lender's charge for lending you money. It is calculated on the remaining loan balance each month. As the balance drops, the interest portion of each payment also drops. That is the core mechanic of mortgage amortization.

Your interest rate and loan term together determine how much interest you pay in total. A lower rate on a shorter term produces the least total interest cost. A higher rate on a 30-year term produces the most. The monthly payment difference between a 6% and a 7% rate on a $300,000 loan is significant over three decades.

Key factors that shape your interest costs:

- Interest rate type: Fixed rates lock your rate for the life of the loan. Adjustable rates (ARMs) start lower but can rise after an initial period, changing your monthly payment.

- Loan term: A 15-year mortgage carries a higher monthly payment but far less total interest than a 30-year mortgage.

- Remaining balance: Interest is recalculated monthly on whatever balance remains. Paying down principal faster reduces future interest charges directly.

- Rate environment: Rates set by market conditions at the time you close determine your baseline cost for fixed-rate loans.

The interest-only mortgage calculator from ZENRG Finance is a useful tool for visualizing how interest-only periods compare to fully amortizing payments, which helps clarify how much of your payment actually reduces the balance.

Understanding property taxes and insurance in mortgage payments

Property taxes and homeowners insurance are typically collected monthly and held in an escrow account. Lenders escrow taxes and insurance to ensure timely payment, preventing tax liens on the property or a lapse in insurance coverage. The lender pays these bills on your behalf when they come due.

Here is how the escrow process works step by step:

- Estimate annual costs: Your lender calculates the expected annual property tax and insurance premium at closing.

- Divide into monthly amounts: The total is divided by 12 and added to your principal and interest payment.

- Collect monthly: Each payment deposits the tax and insurance portion into your escrow account.

- Pay on your behalf: When tax bills and insurance renewals come due, the lender pays them directly from the escrow account.

- Annual review: The lender reviews the account each year and adjusts the monthly escrow amount if costs have changed.

Property taxes vary widely by location. A home in New Jersey carries a very different tax burden than the same-priced home in Alabama. Homeowners insurance premiums depend on the home's value, location, and coverage level. Both costs are outside your control but directly affect your monthly payment.

Pro Tip: Request your escrow account statement every year and review it before the adjustment takes effect. If your taxes or insurance premiums increased, your monthly payment will rise even if your interest rate never changed. Catching this early lets you plan your budget without surprises.

What are PMI and closing costs, and how do they affect payments?

Private mortgage insurance (PMI) is required when your down payment is less than 20% of the purchase price. PMI adds $100 to $200 per month to a typical mortgage payment. It protects the lender, not you, against default risk. PMI is a real cost that inflates your monthly housing expense until you build enough equity.

The good news is that PMI is temporary. Under Consumer Financial Protection Bureau (CFPB) guidelines, you can request PMI cancellation when your loan balance reaches 80% of the original appraised value. Lenders must terminate PMI automatically when the balance hits 78%. On a standard 30-year loan, that automatic cancellation typically happens around year 11.

Closing costs are a separate, one-time expense paid at settlement. Typical closing costs range from 2% to 5% of the loan amount. On a $300,000 loan, that means $6,000 to $15,000 due at closing, not spread across monthly payments.

Common closing cost categories include:

- Origination fees: Charged by the lender for processing the loan application.

- Underwriting fees: Cover the lender's cost to evaluate your creditworthiness and approve the loan.

- Title insurance: Protects against ownership disputes or title defects discovered after closing.

- Appraisal fee: Pays for the independent valuation of the property.

- Recording fees: Government charges for recording the deed and mortgage documents.

- Prepaid items: Upfront deposits for homeowners insurance, property taxes, and prepaid interest.

Closing costs are paid at settlement and are entirely separate from your ongoing monthly mortgage payment. They influence how much cash you need on closing day, not what you pay each month afterward.

| Closing Cost Item | Typical Cost Range |

|---|---|

| Origination fee | 0.5%–1% of loan amount |

| Underwriting fee | $400–$900 |

| Title insurance | $500–$1,500 |

| Appraisal fee | $300–$600 |

| Recording fees | $25–$250 |

| Prepaid taxes and insurance | 2–6 months of escrow |

Pro Tip: Use a loan comparison calculator to compare total costs across loan options, including how different down payment amounts affect both PMI duration and closing cost structures.

Why does your mortgage payment change even with a fixed rate?

A fixed interest rate does not mean a fixed total payment. The principal and interest portion stays constant. The escrow portion does not. Escrow adjustments can increase your monthly payment if property taxes or insurance premiums rise, even when your rate never moves.

Three common reasons your payment changes:

- Escrow shortage: If your tax or insurance costs rose more than the lender projected, you owe the difference. The lender spreads that shortage across the next 12 months, raising your payment.

- Escrow surplus: If costs came in lower than projected, the lender refunds the surplus or credits it to future payments, slightly reducing your monthly amount.

- PMI removal: Once your loan balance hits 80% of the original appraised value, you can request PMI cancellation. Removing $100 to $200 per month in PMI is a meaningful reduction in your total housing cost.

Escrow shortages and surpluses are reconciled annually. Most borrowers are surprised by the adjustment letter because they never tracked the escrow portion separately. Reviewing your escrow statement each year eliminates that surprise. For a deeper look at how lenders disclose these costs, the TRID disclosure standards covered in the 2026 mortgage compliance checklist explain exactly what lenders are required to show you.

Key Takeaways

A mortgage payment is made up of principal, interest, taxes, insurance, and potentially PMI. Each component behaves differently and can change independently over the life of the loan.

| Point | Details |

|---|---|

| PITI is the core structure | Every mortgage payment includes principal, interest, taxes, and insurance as the four base components. |

| Amortization shifts the split | Early payments are mostly interest; later payments allocate more to principal as the balance decreases. |

| Escrow causes payment changes | Property tax and insurance increases raise your monthly payment even when your interest rate is fixed. |

| PMI is temporary | Request cancellation at 80% loan-to-value; lenders must remove it automatically at 78%. |

| Closing costs are separate | Closing costs of 2%–5% of the loan are paid at settlement, not rolled into monthly payments. |

What I have learned from watching borrowers misread their mortgage

By Omar Khamisa

After two decades working as a processor, underwriter, and loan originator, the single most common mistake I see is borrowers treating their mortgage payment as one number instead of four. They negotiate hard on the interest rate and then get blindsided six months later when an escrow adjustment raises their payment by $150 a month.

The interest rate matters. But taxes and insurance often matter just as much over a 30-year term, especially in high-tax states or areas with rising insurance premiums due to climate risk. I have seen borrowers in Florida and Texas watch their insurance premiums double in three years, pushing their total payment well above what they budgeted at closing.

My practical advice: ask your lender for the full PITI breakdown before you close, not just the principal and interest figure. Review your escrow statement every year the moment it arrives. And if you put less than 20% down, track your loan balance against the original appraised value. Requesting PMI cancellation the day you hit 80% loan-to-value is money back in your pocket that most borrowers leave on the table for years.

Understanding the full mortgage costs breakdown before you sign is not just good financial practice. It is the difference between a payment that fits your life and one that strains it.

— Omar Khamisa

How 1 Solution Mortgage Software helps you see the full picture

Knowing your PITI breakdown is one thing. Having a tool that shows it clearly is another.

1 Solution Mortgage Software was built by mortgage professionals who know exactly where borrowers get confused. The platform gives brokers and their clients a clear view of how each payment is allocated across principal, interest, taxes, and insurance. It brings pricing, compliance, and payment detail into one place so nothing gets buried in a statement. If you work with a broker powered by 1 Solution Mortgage Software, you get the transparency that most mortgage platforms simply do not offer. Visit 1smtg.com to learn how the platform supports better mortgage planning from day one.

FAQ

What does PITI stand for in a mortgage payment?

PITI stands for principal, interest, taxes, and insurance. These four components make up the standard monthly mortgage payment for most homebuyers.

When is PMI required and how do I remove it?

PMI is required when your down payment is less than 20% of the purchase price. You can request cancellation when your loan balance reaches 80% of the original appraised value, and lenders must remove it automatically at 78%.

Why did my mortgage payment increase if I have a fixed rate?

A fixed rate locks only the principal and interest portion of your payment. If your property taxes or homeowners insurance premiums increased, your escrow portion rises, which raises the total monthly payment.

What are typical closing costs on a mortgage?

Closing costs typically range from 2% to 5% of the loan amount. On a $300,000 loan, that equals $6,000 to $15,000 paid at settlement, separate from your ongoing monthly payment.

How does amortization affect my principal and interest split?

Early mortgage payments are weighted heavily toward interest. As the loan balance decreases over time, each payment allocates a larger share to principal, building equity faster in the later years of the loan.