Mortgage regulatory compliance is defined as the process by which mortgage professionals adhere to applicable federal and state laws, quality control standards, and licensing requirements to ensure lawful, fair, and transparent lending. The core framework rests on overlapping federal statutes: the Truth in Lending Act (TILA), the Real Estate Settlement Procedures Act (RESPA), the Equal Credit Opportunity Act (ECOA), and the Home Mortgage Disclosure Act (HMDA). Anti-Money Laundering (AML) obligations, including Know Your Customer (KYC) and OFAC screening, apply at loan intake. Enforcement falls to the Consumer Financial Protection Bureau (CFPB), the FDIC, and the Financial Crimes Enforcement Network (FinCEN). Understanding mortgage regulatory compliance explained in full means tracking requirements from application through post-closing quality control, not just at the point of approval.

What federal laws govern mortgage regulatory compliance?

Mortgage lending sits at the intersection of multiple federal statutes, each targeting a distinct risk. Together, they form the foundation of every mortgage compliance checklist a broker or loan originator must follow.

Key laws and what they require

- TILA (Regulation Z): Requires lenders to disclose the Annual Percentage Rate (APR) and all key credit terms before consummation. Borrowers must receive a Loan Estimate within three business days of application and a Closing Disclosure at least three business days before closing. The TILA-RESPA Integrated Disclosure (TRID) rule merged these two disclosure timelines into one coordinated process.

- RESPA (Regulation X): Prohibits kickbacks, fee-splitting, and referrals to affiliated settlement service providers unless proper disclosure is made. RESPA also governs escrow account management and requires a Good Faith Estimate of settlement costs.

- ECOA and the Fair Housing Act (FHA): Both prohibit discrimination in lending based on race, color, religion, national origin, sex, marital status, age, or receipt of public assistance. Lenders must document credit decisions with objective, consistent criteria.

- HMDA: Requires covered lenders to collect and report loan-level data on applications, originations, and denials. Regulators use HMDA data to identify fair lending patterns and geographic disparities.

- Gramm-Leach-Bliley Act (GLBA) and Fair Credit Reporting Act (FCRA): The GLBA requires privacy notices and data protection for consumer financial information. The FCRA governs how lenders obtain, use, and dispute consumer credit data.

- AML and KYC/OFAC: At loan intake, lenders must verify borrower identity under KYC protocols and screen applicants against the OFAC Specially Designated Nationals list. These steps satisfy Bank Secrecy Act and FinCEN obligations.

Each law carries its own penalty structure. RESPA violations can result in fines up to $10,000 per violation. ECOA violations can trigger class-action exposure. Treating these statutes as separate checklists rather than an integrated system is the first operational mistake most brokers make.

How do compliance checkpoints integrate across the mortgage lifecycle?

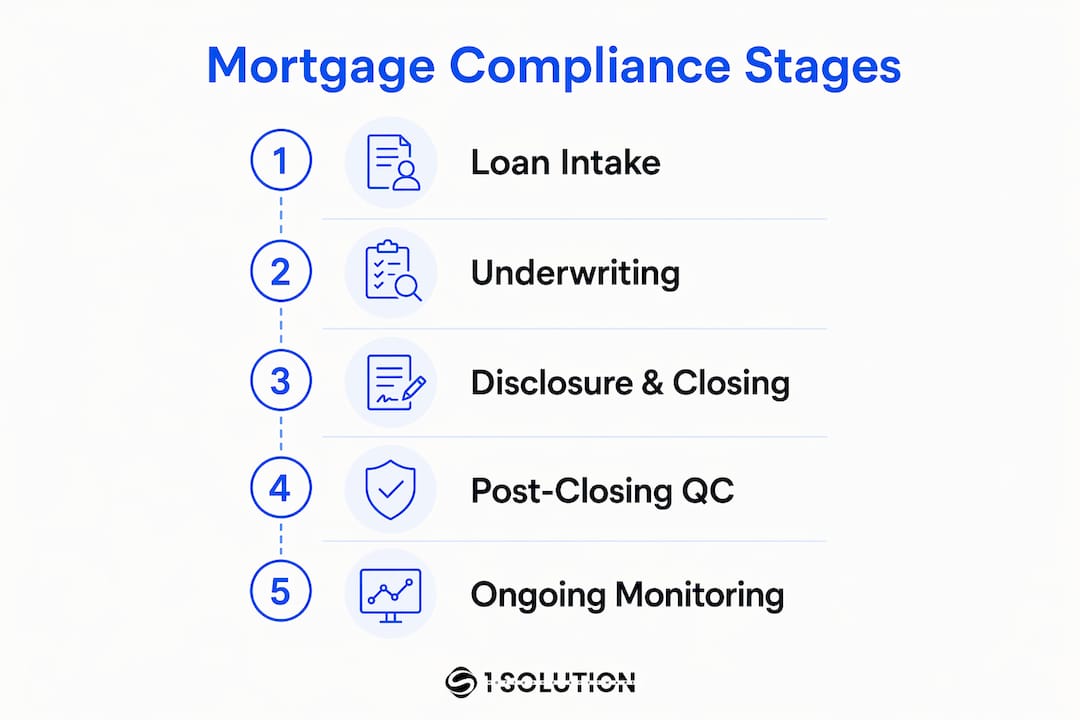

Mortgage lending compliance is not a single event. It runs as a sequence of operational checkpoints from intake through closing and beyond.

Stage 1: Loan intake

Identity verification is the first mandatory step. KYC procedures confirm the borrower's identity using government-issued documents. OFAC screening checks the applicant against federal sanctions lists. Both checks must be documented before the file moves forward. Skipping or delaying either creates an AML gap that regulators treat as a material deficiency.

Stage 2: Underwriting

The Ability-to-Repay (ATR) and Qualified Mortgage (QM) rule requires lenders to verify a borrower's capacity to repay using eight specific factors: income, assets, employment, credit history, monthly payment, simultaneous loans, mortgage-related obligations, and debt-to-income ratio. A loan that meets QM standards receives a legal safe harbor against ATR challenges. Lenders who skip the documentation trail lose that protection entirely.

Fair lending analysis also runs during underwriting. Loan officers must apply consistent credit standards across all applicants. Any deviation that correlates with a protected class characteristic triggers ECOA and FHA scrutiny.

Stage 3: Disclosure and closing

TRID governs the closing stage. The Closing Disclosure must match the Loan Estimate within defined tolerance thresholds. Fees outside tolerance require a cure, meaning the lender absorbs the difference. Mortgage servicing compliance continues after closing under Regulations X and Z, covering escrow management, error resolution, loss mitigation, and periodic statements.

- Confirm TRID tolerance compliance before the three-day waiting period begins.

- Verify all trailing documents are collected and filed within required timeframes.

- Deliver the closed loan package to the investor within the agreed purchase window.

- Initiate post-closing quality control within the required review cycle.

Pro Tip: Build a compliance checklist that maps each regulatory requirement to a specific staff role and deadline. Ambiguity about who owns a task is the most common cause of missed disclosure windows.

What is the role of post-closing quality control in mortgage compliance?

Post-closing quality control is where many compliance failures actually occur. Most brokers focus their compliance energy on the approval stage. The gap between loan closing and final investor delivery is where defects accumulate and repurchase risk grows.

Fannie Mae's Selling Guide Announcement SEL-2025-04, effective September 2, 2025, requires lenders to review at least 10% of monthly loan production through a formal QC process, completed within 90 days of the loan closing month. Lenders who fall more than one 30-day cycle behind must notify Fannie Mae directly. That notification requirement is not optional, and missing it compounds the original deficiency.

Pre-closing vs. post-closing compliance responsibilities

| Responsibility | Pre-closing | Post-closing |

|---|---|---|

| Disclosure accuracy | Loan Estimate and Closing Disclosure review | Confirm no tolerance cures were missed |

| Identity verification | KYC and OFAC screening at intake | Re-verify if file is flagged during QC |

| Income documentation | Verify pay stubs, tax returns, W-2s | Audit for inaccuracies or missing docs |

| Undisclosed debt | Credit refresh before closing | QC review of final credit report |

| Investor delivery | Prepare complete loan package | Confirm receipt and trailing document status |

Common defects uncovered in post-closing QC include income verification errors, missing or unsigned documents, undisclosed liabilities, and appraisal discrepancies. Each defect category carries a different remediation path. Income errors often require a repurchase demand from the investor. Missing documents may be curable with a trailing document submission.

Pro Tip: Assign a dedicated post-closing coordinator whose sole responsibility is tracking QC timelines. A shared calendar with 30-day cycle alerts prevents the notification failures that trigger Fannie Mae escalations.

What are the major compliance risks and how can brokers mitigate them?

The CFPB, FDIC, and FinCEN each hold enforcement authority over different segments of mortgage compliance. CFPB focuses on consumer protection laws including TILA, RESPA, and ECOA. FDIC supervises depository institutions. FinCEN enforces AML and Bank Secrecy Act requirements. Enforcement actions range from civil money penalties to consent orders and license revocations.

The most frequent violations mortgage professionals face fall into four categories: inaccurate or late disclosures, discriminatory underwriting patterns, poor documentation practices, and AML gaps at intake. Each category is preventable with the right operational controls.

Best practices for ongoing compliance adherence

- Conduct regular training. Loan officers and processors must complete annual fair lending and AML training. Regulations change, and staff who learned compliance rules three years ago are operating on outdated knowledge.

- Run internal audits quarterly. Do not wait for a regulatory examination to find defects. A quarterly file review on a random sample of closed loans catches patterns before they become enforcement issues.

- Use a mortgage compliance checklist for every loan. A written checklist tied to each regulatory requirement creates a documented record that the process was followed.

- Implement user-level access controls in your loan origination system. Restricting who can modify a file after underwriting approval prevents unauthorized changes that create compliance exposure. A user permissions setup in your software is a direct AML control.

- Monitor regulatory updates from the CFPB and Fannie Mae. SEL-2025-04 is one example of a mid-year update that changed operational requirements. Brokers who missed it are already out of cycle.

A compliance management system (CMS) ties these practices together. A CMS documents policies, tracks training completion, logs audit results, and generates reports for regulatory review. Building a CMS is not optional for any broker operating at scale. It is the infrastructure that makes every other compliance practice defensible.

Key Takeaways

Mortgage regulatory compliance requires integrating federal law, operational checkpoints, and post-closing quality control into one documented, auditable system.

| Point | Details |

|---|---|

| Federal law framework | TILA, RESPA, ECOA, HMDA, GLBA, and FCRA each govern a distinct compliance obligation. |

| AML at intake | KYC identity verification and OFAC screening must be completed and documented before underwriting begins. |

| ATR/QM safe harbor | Documenting all eight ATR factors protects lenders from legal challenges on repayment capacity. |

| Post-closing QC mandate | Fannie Mae requires a 10% monthly loan review completed within 90 days under SEL-2025-04. |

| Compliance management system | A documented CMS covering policies, training, and audits is the foundation of defensible compliance. |

Compliance is an operational system, not a paperwork exercise

After 20 years working as a processor, underwriter, loan originator, and systems consultant, I have seen the same mistake repeated across shops of every size. Brokers treat compliance as a documentation task. They fill out the forms, check the boxes, and move on. The problem is that regulators do not grade you on whether the forms exist. They grade you on whether the process behind the forms is consistent, documented, and auditable.

The post-closing QC phase is the clearest example of this gap. Most brokers I have worked with have no formal QC program. They close the loan, deliver it to the investor, and consider the file done. The Fannie Mae SEL-2025-04 requirement changes that calculus. A post-closing compliance program is now a mandatory operational function, not an optional best practice.

Technology helps, but only if the underlying process is sound. I have seen brokers implement compliance software and still fail audits because the software was tracking the wrong things. The tool reflects the process. If the process is broken, the software just documents the failure faster.

The brokers who stay clean through regulatory cycles are the ones who build compliance into their daily operations. They train staff consistently, run internal audits before examiners do, and use their compliance management guide as a living document, not a binder that sits on a shelf. That is the difference between compliance as a culture and compliance as a checkbox.

— Omar Khamisa

How 1 Solution Mortgage Software supports your compliance operations

Staying current with mortgage compliance guidelines requires more than good intentions. It requires systems that track requirements, flag deficiencies, and document your process at every stage.

1 Solution Mortgage Software was built by mortgage professionals who have worked every role in the origination process. The platform integrates compliance checks, document tracking, KYC and AML screening, and post-closing QC management into one connected system. Fannie Mae QC requirements, TRID disclosure timelines, and fair lending documentation are all supported within the platform. Independent brokers who want control over their compliance process without paying enterprise prices can see the full platform and request a walkthrough. Built from the trenches, for the brokers who work in them.

FAQ

What is mortgage regulatory compliance?

Mortgage regulatory compliance is the process of adhering to federal and state laws, quality control standards, and licensing requirements that govern mortgage lending. Core statutes include TILA, RESPA, ECOA, HMDA, and AML obligations under the Bank Secrecy Act.

What does TRID require at closing?

TRID requires lenders to deliver a Closing Disclosure at least three business days before closing, with fees matching the Loan Estimate within defined tolerance thresholds. Fees outside tolerance must be cured by the lender.

What is the Fannie Mae post-closing QC requirement?

Fannie Mae requires lenders to review at least 10% of monthly loan production within 90 days of the closing month under SEL-2025-04, effective September 2, 2025. Lenders who fall behind must notify Fannie Mae directly.

Which agencies enforce mortgage compliance?

The CFPB enforces consumer protection laws including TILA and RESPA. The FDIC supervises depository institutions. FinCEN enforces AML and Bank Secrecy Act requirements across all covered lenders.

What is a compliance management system for mortgage brokers?

A compliance management system (CMS) is a documented framework covering written policies, staff training records, internal audit logs, and regulatory reporting. It is the operational structure that makes a broker's compliance process auditable and defensible during regulatory review.