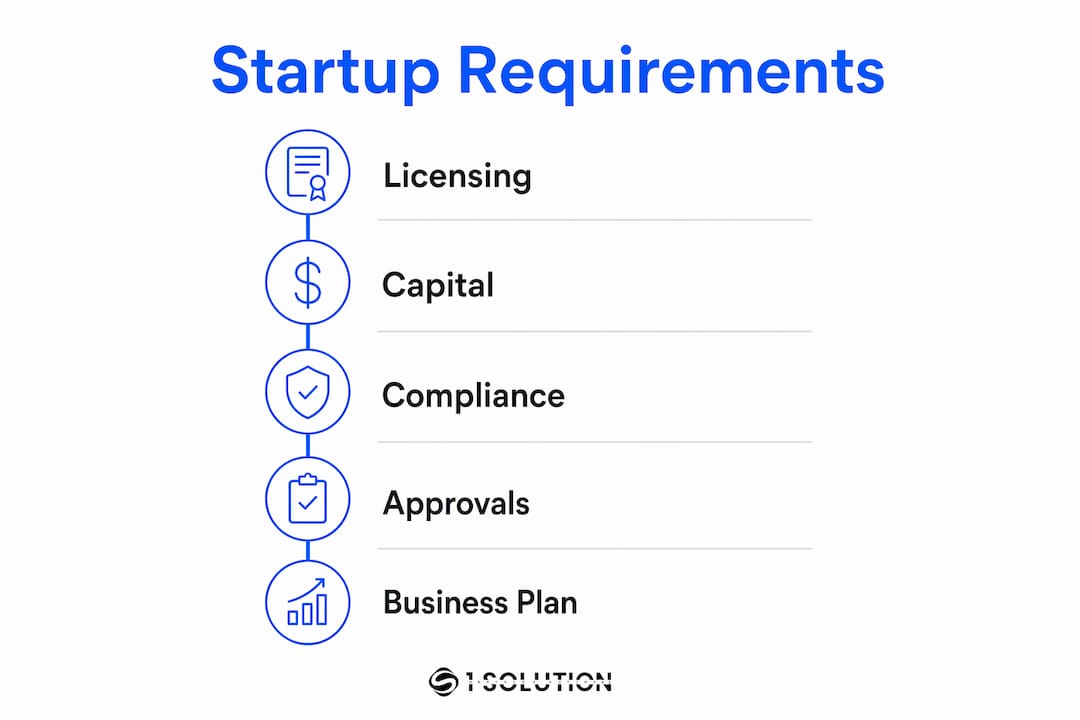

Launching a mortgage brokerage requires licensing, capital, compliance, and lender approvals before you can originate a single loan. These are the mortgage startup requirements explained in full: a company NMLS license, individual MLO licenses for every loan officer, surety bonds, errors and omissions insurance, and wholesale lender agreements. Platforms like Encompass, Floify, and the NMLS system itself are part of your operational infrastructure from day one. Understanding these legal and financial commitments upfront is the difference between a brokerage that opens on schedule and one that stalls in regulatory limbo.

What licenses and education are required to start a mortgage brokerage?

Licensing is the first and most non-negotiable step when starting a mortgage business. Launching a residential brokerage requires both a company NMLS license and individual MLO licenses for every loan originator on your team. You submit all applications through the Nationwide Multistate Licensing System, which is the federal registry that every state regulator uses to track mortgage professionals.

Every individual MLO must complete 20 hours of SAFE Act pre-licensing education before sitting for the national exam. That education covers federal mortgage law, ethics, lending standards, and elective coursework. After completing the hours, each candidate must pass the National SAFE MLO Test with a score of at least 75%. If someone fails, they wait 30 days before retesting. After three failures, the wait period extends to 180 days. That timeline alone can push your launch date back by months if you are not planning ahead.

Here is what the licensing process requires at a glance:

- Company NMLS license: Filed at the entity level, covering your brokerage as a business

- Individual MLO licenses: Required for every loan originator, filed separately through NMLS

- 20 hours of SAFE Act education: Covering federal law, ethics, and non-traditional mortgage products

- National SAFE MLO Test: Minimum passing score of 75%, with structured retest waiting periods

- FBI background check and fingerprints: Mandatory for all MLO applicants

- Credit check: Regulators review financial history as part of the fitness determination

- Annual renewal: Each license must be renewed yearly with 8 hours of continuing education

State-specific requirements add another layer. Some states require additional education hours, state-specific exams, or net worth documentation. You must research each state where you plan to originate loans. If you are planning to operate across multiple states, the licensing workload multiplies fast.

Pro Tip: Review the SAFE Act education requirements before you hire your first MLO. Knowing the exam timeline helps you build a realistic launch schedule and avoid costly delays.

How much capital and insurance does a mortgage startup need?

Capital requirements for a mortgage startup depend heavily on your business model. Startup capital ranges from $15,000 to $40,000 for a solo commercial broker and from $100,000 to $500,000 for a small-team residential brokerage. That spread reflects real differences in staffing, office space, technology, and regulatory fees. Do not plan around the low end unless your model genuinely supports it.

| Expense Category | Solo Commercial Broker | Small-Team Residential |

|---|---|---|

| Startup Capital Range | $15,000–$40,000 | $100,000–$500,000 |

| Surety Bond Premium | 1%–3% of bond amount annually | 1%–3% of bond amount annually |

| Legal Consultation | $2,000–$5,000 upfront | $2,000–$5,000 upfront |

| Technology and LOS | Varies by platform | Varies by platform |

| E&O Insurance | Varies by coverage level | Varies by coverage level |

Surety bonds are required in every state. Bond amounts range from $10,000 to $500,000 depending on the state, and premiums run 1%–3% of the bond amount annually. A $100,000 bond at 2% costs $2,000 per year. That is a recurring cost you need to build into your annual budget from the start.

Errors and omissions insurance protects your brokerage against claims arising from mistakes in the loan process. Most wholesale lenders require proof of E&O coverage before approving your brokerage. The cost varies based on your loan volume, coverage limits, and state. Budget for it as a fixed operating expense, not an afterthought.

Legal consultation is one area where founders consistently underinvest. A $2,000 to $5,000 legal consultation upfront helps you structure your entity correctly, understand your compliance obligations, and avoid mistakes that cost far more to fix later. Skipping this step to save money is one of the most common and expensive errors new founders make.

Pro Tip: Get your entity structure and compliance framework reviewed by a mortgage attorney before you file your NMLS application. Fixing a structural mistake after licensing is approved costs more in time and money than doing it right the first time.

What ongoing compliance obligations must mortgage startups meet?

Compliance does not stop at launch. The regulatory obligations for a licensed mortgage brokerage are continuous, and missing deadlines carries real consequences including fines, license suspension, and forced audits.

Here are the core ongoing requirements every mortgage startup must track:

- Annual MLO license renewal: Every MLO must renew their license each year. Renewal requires 8 hours of continuing education, covering federal law updates, ethics, and elective topics. Missing the renewal window can result in license lapse.

- Quarterly Mortgage Call Reports: These reports must be submitted within 45 days after each quarter ends. They capture your loan volume, origination activity, and business data. Regulators use them to monitor market activity and flag anomalies.

- Annual financial statements: Reviewed financial statements are due within 90 days of your fiscal year-end. Some states require audited statements depending on your loan volume or license type.

- Surety bond maintenance: Bonds must stay active and current. If your bond lapses, your license is at risk.

- TRID compliance: Every loan file must comply with TILA-RESPA Integrated Disclosure rules, which govern how and when you deliver loan estimates and closing disclosures to borrowers.

- Regulatory exam readiness: New licensees should expect regulatory audits within the first two years. Examiners review loan files, advertising materials, and financial records. Net worth requirements up to $250,000 may apply depending on the state.

The most common compliance failure for new brokerages is poor recordkeeping. Regulators expect organized, complete loan files from the first loan you close. Build your filing and documentation systems before you originate, not after. Review the mortgage compliance setup checklist to make sure your systems are ready before you open your doors.

What operational approvals do mortgage startups need before originating loans?

Licensing gets you legal authority to operate. Operational approvals get you the actual ability to do business. These are two different things, and many founders underestimate the second.

Wholesale lender approvals are the most critical operational requirement. Without approved lender agreements, you cannot originate loans. Lenders like UWM and Rocket Pro have structured approval processes with specific documentation requirements, financial thresholds, and contract terms. Some agreements include anti-competition clauses that restrict you to one lender for certain loan types. Read every contract before you sign. Understanding broker-lender relationships before you negotiate these agreements gives you a real advantage.

Your technology stack is the next critical layer. A Loan Origination System handles disclosures, document collection, and workflow automation. Platforms like Encompass and Floify are widely used in the broker channel. Your LOS must integrate with your pricing engine, CRM, and compliance tools. Fragmented systems create compliance gaps and slow down your loan processing.

Mortgage fintech startups face a higher bar. Documented alignment with GLBA, FFIEC, and CFPB rules is required, and tech audits verify that privacy policies and staff compliance training are current within the last 12 months. This is not a checkbox exercise. Regulators treat technology compliance as seriously as licensing compliance.

Your business plan must also contain real working numbers. A plan without explicit assumptions tied to deal count, average loan size, and commission rate is not a plan. It is a wish list. Founders who build their projections around specific, defensible assumptions are far better positioned to manage cash flow and communicate with lenders or investors.

Key takeaways

Launching a mortgage brokerage requires NMLS licensing, adequate capital reserves, continuous compliance management, and secured lender approvals before you can originate a single loan.

| Point | Details |

|---|---|

| Licensing is non-negotiable | Every brokerage needs a company NMLS license and individual MLO licenses before operating. |

| Capital needs vary widely | Solo brokers need $15,000–$40,000; small teams need $100,000–$500,000 to cover all startup costs. |

| Compliance is continuous | Annual renewals, quarterly call reports, and audit readiness are required from day one. |

| Lender approvals unlock origination | Without wholesale lender agreements, you cannot fund loans regardless of your license status. |

| Business planning must use real numbers | Projections tied to deal count, loan size, and commission rates are the foundation of a viable plan. |

What i have learned after 20 years in this industry

Most founders I talk to underestimate two things: how long the runway actually is, and how much the first two years test your reserves.

The period before your first commission check often runs four to eight months. That is not a warning. That is a fact you need to plan around. I have seen capable, experienced originators run out of operating capital before their pipeline produced a single closed loan. The fix is not working harder. It is reserving six to nine months of living expenses on top of your startup capital before you file your first NMLS application.

The second thing founders consistently get wrong is treating legal consultation as optional. Early legal counsel is not a luxury. It is the cheapest insurance you will ever buy. A mortgage attorney who knows your state's licensing rules can catch entity structure problems, flag compliance gaps, and help you negotiate lender agreements before you are locked into terms you did not fully understand.

Technology is where I see the most confusion. Founders often pick a platform based on price or a recommendation from another broker, without thinking about how it connects to their compliance workflow. Your LOS, CRM, and pricing engine need to work together. Fragmented systems do not just slow you down. They create audit exposure. Build your tech stack around compliance first, then efficiency.

My honest advice: treat your business plan as a financial model, not a narrative. Know your deal count assumptions. Know your average loan size. Know your commission split. If you cannot defend every number in your plan, you are not ready to launch.

— Omar Khamisa

How 1 solution mortgage software supports new mortgage startups

Starting a mortgage brokerage is hard enough without technology working against you. 1 Solution Mortgage Software was built specifically for independent brokers who need one connected platform instead of five fragmented tools.

1 Solution Mortgage Software brings together LOS, CRM, pricing, compliance, POS, and communication tools into a single ecosystem designed for the realities of broker operations. For startups, that means you can manage NMLS compliance workflows, track license renewals, and maintain audit-ready documentation without juggling multiple vendors. The platform was built by mortgage professionals who have worked as processors, underwriters, and loan originators. It reflects how brokers actually work. Explore 1 Solution Mortgage Software to see how it fits your startup plan.

FAQ

What is the NMLS and why do mortgage startups need it?

The Nationwide Multistate Licensing System is the federal registry that processes and tracks mortgage company and MLO licenses across all states. Every mortgage brokerage must register through NMLS before originating loans.

How long does it take to get licensed as a mortgage broker?

The timeline varies by state, but most founders should plan for 60–120 days from starting SAFE Act education to receiving their company and individual MLO licenses. Retest waiting periods and state-specific requirements can extend that timeline.

What is a surety bond and is it required for mortgage brokers?

A surety bond is a financial guarantee that protects consumers if a broker violates licensing laws. Surety bonds are required in every state, with amounts ranging from $10,000 to $500,000 depending on state rules.

Do mortgage startups need a business plan to get licensed?

A formal business plan is not always required for NMLS licensing, but it is required by most wholesale lenders during the approval process. A data-driven business plan with specific loan volume and revenue assumptions is the standard lenders expect.

What is the difference between a mortgage broker and a mortgage lender?

A mortgage broker originates loans on behalf of borrowers and submits them to wholesale lenders for funding. A mortgage lender funds loans directly using its own capital. Brokers require NMLS licensing and wholesale lender approvals; lenders face additional net worth and warehouse line requirements.