Lender comparison in mortgage brokerage is the practice of systematically evaluating multiple lender offers to secure the best terms for each client while improving brokerage efficiency. The role of lender comparison in brokerage goes far beyond finding the lowest rate. It shapes client outcomes, drives operational accuracy, and positions brokers as genuine advocates rather than order takers. The CFPB's guidance on using official Loan Estimates side by side is the most reliable method for comparing lender offers accurately. Brokers who build this practice into their workflow close better loans, generate fewer rework cycles, and earn stronger client referrals.

What are the primary benefits of lender comparison for mortgage brokers?

Lender comparison delivers measurable financial benefits for both brokers and their clients. Thorough comparison shopping can save borrowers an average of over $62,000 over a standard mortgage lifetime. That figure reflects the compounding effect of even small rate differences. A 0.25% rate reduction on a $400,000 mortgage saves roughly $17,000 over 30 years.

Brokers gain a structural cost advantage through wholesale pricing channels. Retail origination costs average $11,800 per loan, while brokers who access wholesale markets negotiate lower fees for clients. This pricing gap is the core reason independent brokers compete effectively against direct lenders and banks.

Beyond base rates, skilled comparison creates negotiation leverage. Broker-led negotiation tactics can secure additional closing cost savings of $2,000–$8,000 per client. Techniques like requesting lender credits, waiving escrow requirements, and presenting competing offers to account executives unlock value that clients cannot access on their own.

Lender comparison also improves loan fit. Not every client qualifies for the same product at the same lender. Matching a client's financial profile to the right lender's appetite reduces denial risk and speeds up approval. Transparency in compensation disclosure, required under TRID regulations, reinforces client trust throughout this process.

- Cost savings: Wholesale pricing consistently beats retail origination costs for comparable loan products.

- Loan fit: Comparing lender overlays and program guidelines matches clients to the right product faster.

- Negotiation power: Competing Loan Estimates give brokers real leverage with wholesale account executives.

- Client trust: Clear cost disclosure under TRID builds confidence and reduces post-closing surprises.

Pro Tip: Present at least three Loan Estimates to clients before recommending a lender. The side-by-side format makes the cost differences concrete and positions you as a thorough advocate, not just a rate shopper.

How do mortgage brokers conduct effective lender comparison?

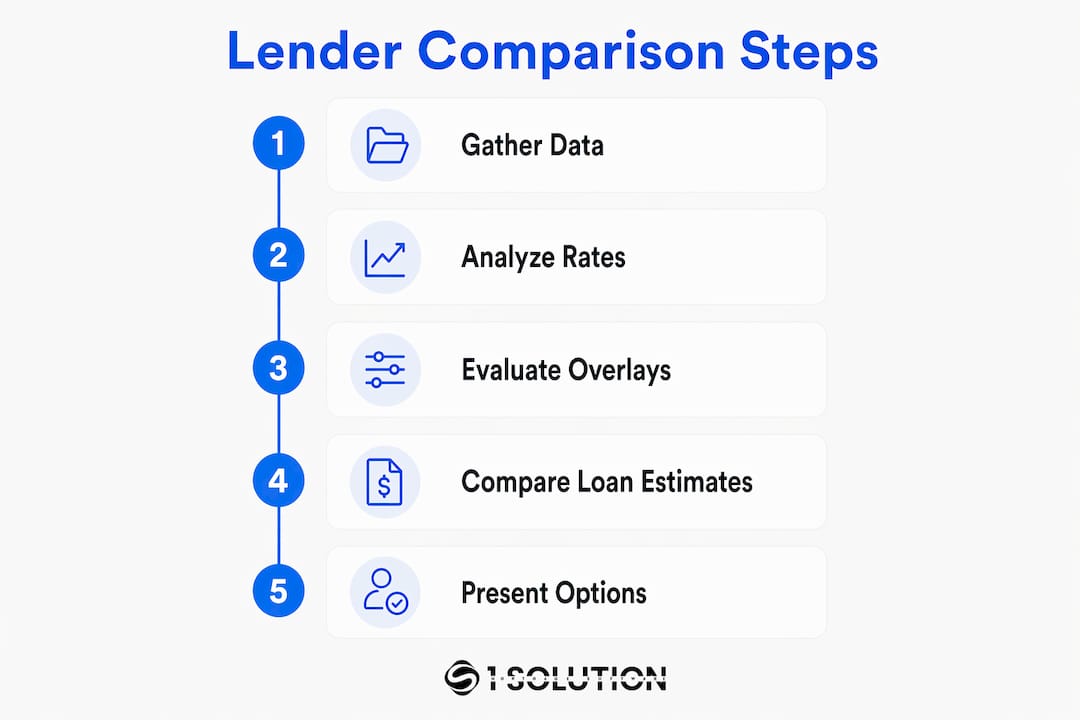

Effective lender comparison follows a structured process. Skipping steps creates errors, delays, and missed savings opportunities.

-

Pull multiple Loan Estimates. The CFPB recommends side-by-side Loan Estimate review as the standard method for identifying true cost differences. Loan Estimates strip out marketing language and show real fees, compensation, and APR on a standardized form.

-

Assess lender overlays. Overlays are internal lender requirements that go beyond agency guidelines. A lender may require a 680 minimum credit score even when Fannie Mae allows 620. Brokers who track overlay changes weekly place loans more accurately and avoid unnecessary declines.

-

Leverage your wholesale network. Brokers with strong broker-lender relationships access pricing and programs unavailable to retail borrowers. Presenting a competing Loan Estimate directly to a wholesale account executive often unlocks price exceptions or lender credits that are not publicly listed.

-

Disclose compensation clearly. Broker compensation of 1–2.75% of the loan amount must appear on the Loan Estimate under TRID rules. Explaining this disclosure proactively prevents client confusion and reinforces your credibility.

-

Use technology to manage the process. Platforms like 1 Solution Mortgage Software centralize lender comparison data, track multiple loan scenarios, and reduce the manual effort of managing competing offers across a pipeline.

Understanding how to compare lenders requires more than pulling rates from a pricing engine. It demands overlay awareness, relationship management, and disciplined documentation at every step.

Pro Tip: Build a weekly overlay tracker for your top five wholesale lenders. Overlay requirements shift frequently, and knowing which lender is most flexible on a specific file type saves hours of rework per loan.

What nuances and challenges affect lender comparison results?

Lender comparison is not a simple apples-to-apples exercise. Several factors complicate the results and require experienced judgment.

Compensation disclosure creates a perception problem. Broker compensation, typically 1–2.75% of the loan amount, appears as a visible line item on the Loan Estimate. Direct lender margin is built into the rate and is not separately disclosed. This makes broker pricing appear more expensive at first glance, even when the net cost to the borrower is lower after accounting for wholesale discounts.

Speed versus cost tradeoffs are real. Direct lenders sometimes close faster because they control underwriting internally. Brokers route files through wholesale channels, which adds a processing layer. For clients with tight closing timelines, this tradeoff matters. Brokers who communicate turnaround times honestly and choose lenders with strong operational track records manage this challenge effectively.

Complex files require overlay expertise. Self-employed borrowers, clients with lower credit scores, and non-QM candidates benefit most from broker-led comparison. Overlay flexibility is greatest in the wholesale channel. Banks apply the strictest overlays; brokers access lenders with the lightest requirements. This difference directly affects approval rates for non-standard files.

Common pitfalls brokers should avoid in the comparison process:

- Competing purely on interest rate without accounting for fees, overlays, and closing speed

- Failing to present competing Loan Estimates to account executives before accepting initial pricing

- Ignoring lender appetite changes, which shift weekly based on volume and secondary market conditions

- Overlooking the importance of choosing the right lender for each specific file type rather than defaulting to a preferred lender for every deal

- Presenting clients with too many options without a clear recommendation, which creates confusion rather than confidence

The importance of lender selection comes down to matching the loan's characteristics to the lender's current appetite. A lender that was aggressive on jumbo pricing last month may have tightened this week. Brokers who track these shifts place loans faster and with fewer conditions.

How does lender comparison enhance brokerage efficiency and client satisfaction?

Lender comparison directly reduces rework. When a broker places a loan with the wrong lender, the result is conditions, delays, and sometimes a full restart. Effective lender comparison improves operational efficiency by reducing these rework cycles and accelerating loan closures. Fewer surprises in underwriting mean faster closings and lower per-loan processing costs.

Client satisfaction follows directly from accurate placement. Clients who receive the right loan product at a competitive price, with clear cost disclosure, refer more business. The broker's role as a knowledgeable advocate is reinforced every time a comparison reveals a better option than the client found on their own.

"The debate of broker versus direct lender misses the point. The key is which originator offers the best combination of rate, fees, overlays, and timing for the specific client. Lender comparison is how brokers answer that question with evidence rather than assumption."

Technology integration amplifies these gains. Platforms built for mortgage broker operations centralize loan scenario management, automate document tracking, and reduce the manual effort of comparing multiple offers. 1 Solution Mortgage Software, built specifically for independent brokers, connects pricing, CRM, and pipeline management in one place. That integration cuts the time brokers spend switching between systems and reduces the risk of data errors across competing loan scenarios.

| Benefit | Impact on brokerage |

|---|---|

| Reduced rework cycles | Fewer conditions and restarts lower per-loan processing time |

| Accurate loan placement | Right lender match on the first submission speeds closings |

| Client cost savings | Wholesale pricing and negotiation produce better net costs |

| Stronger referral rates | Transparent advocacy builds long-term client relationships |

| Technology efficiency | Centralized comparison tools reduce manual errors and decision time |

The best lender options for brokers are not always the ones with the lowest published rates. They are the ones whose overlays, pricing, and turnaround times align with the specific file in front of you today.

Key Takeaways

Lender comparison is the single most effective practice brokers use to improve client outcomes and reduce operational waste in the loan origination process.

| Point | Details |

|---|---|

| Comparison saves real money | Borrowers can save over $62,000 lifetime through thorough lender comparison shopping. |

| Loan Estimates are the standard tool | CFPB recommends side-by-side Loan Estimate review as the most accurate comparison method. |

| Overlays determine approval, not just rate | Tracking weekly overlay changes prevents misplaced files and unnecessary declines. |

| Negotiation unlocks hidden savings | Presenting competing offers to account executives can secure $2,000–$8,000 in additional savings. |

| Technology reduces errors and rework | Integrated platforms like 1 Solution Mortgage Software cut manual effort and speed decisions. |

What I've learned about lender comparison after 20 years in the trenches

Most brokers treat lender comparison as a pricing exercise. That is the wrong frame. After two decades working as a processor, underwriter, loan originator, and systems consultant, I can tell you that the brokers who consistently outperform their peers are the ones who treat comparison as a placement strategy.

The rate is just one variable. The lender's current appetite for a specific file type, their overlay flexibility, their underwriting turnaround, and their willingness to grant a price exception when you bring a competing Loan Estimate to the table. Those factors determine whether a loan closes cleanly or drags through conditions for six weeks.

The brokers I've watched struggle are the ones who default to the same two or three lenders for every deal. They stop tracking overlay changes. They stop building relationships with account executives. They compete on rate and wonder why their margins erode. The brokers who thrive are the ones who treat their lender panel as a living tool, updated constantly, matched deliberately to each file's specific characteristics.

Technology matters here, but only if it is built for how brokers actually work. That is why we built 1 Solution Mortgage Software from the ground up for independent brokers, not adapted from a bank platform. The comparison workflow has to be fast, accurate, and connected to the rest of your pipeline. When it is, lender comparison stops feeling like extra work and starts feeling like your competitive edge.

— Omar Khamisa

How 1 Solution Mortgage Software supports your lender comparison workflow

Independent brokers need tools that match how they actually work, not platforms built for banks and retrofitted for the wholesale channel.

1 Solution Mortgage Software brings pricing, CRM, pipeline management, and compliance tools into one connected platform built specifically for mortgage professionals. Brokers use it to manage multiple loan scenarios simultaneously, track competing lender offers, and move files through the pipeline without switching between fragmented systems. The result is faster decisions, fewer errors, and more time spent on client relationships rather than administrative work. If you are ready to make lender comparison a consistent part of your workflow, explore 1 Solution Mortgage Software and see what a platform built from real brokerage experience looks like.

FAQ

What is the role of lender comparison in brokerage?

Lender comparison is the process of evaluating multiple lender offers to find the best combination of rate, fees, overlays, and closing speed for each client. It is the primary method brokers use to deliver better outcomes than direct lenders or banks.

How much can borrowers save through lender comparison?

Thorough lender comparison can save borrowers an average of over $62,000 over a standard mortgage lifetime, with even a 0.25% rate reduction on a $400,000 loan saving roughly $17,000 over 30 years.

What are lender overlays and why do they matter?

Overlays are internal lender requirements that exceed standard agency guidelines, such as a higher minimum credit score than Fannie Mae requires. Brokers who track overlay changes weekly place loans more accurately and avoid unnecessary client declines.

How do brokers use Loan Estimates to compare lenders?

The CFPB recommends reviewing multiple Loan Estimates side by side to identify true cost differences across lenders. This standardized form removes marketing language and shows real fees, APR, and broker compensation on a comparable basis.

Does broker compensation make loans more expensive than direct lenders?

Broker compensation of 1–2.75% appears as a visible line item on the Loan Estimate, while direct lender margin is built into the rate. The net cost to borrowers is often comparable or lower with brokers due to wholesale pricing discounts.