A loan origination system (LOS) is a software platform that automates the entire loan application to approval process, replacing fragmented manual workflows with integrated, compliant digital solutions. For mortgage brokers and lenders, the LOS is the operational core of the lending business. It handles everything from application intake and KYC verification through credit decisioning, compliance checks, and documentation. Modern LOS platforms consolidate 7–10 previously manual processes into one unified automated workflow. That consolidation is what separates high-performing lending operations from those still drowning in spreadsheets and email chains. Understanding what a loan origination system does, what features matter most, and how to choose the right one is the clearest path to faster closings and fewer compliance headaches.

What are the essential features of a loan origination system LOS?

The best loan origination software does far more than collect applications. It orchestrates every step of the pre-disbursement lifecycle through a connected set of tools that work together without manual handoffs.

The core capabilities brokers and lenders should expect from any modern LOS include:

- Multi-channel application intake. Borrowers can apply through web portals, mobile apps, or broker-facing interfaces. Every channel feeds into one centralized pipeline.

- Automated credit decisioning. The system pulls credit bureau data, applies your underwriting rules, and generates decisions without requiring a processor to manually request and review each report.

- Embedded compliance controls. Compliance workflows for TILA, SCRA, and OFAC are built directly into the process. Violations are flagged before they become audit findings, not after.

- API-first architecture. The platform connects to credit bureaus, CRM tools, e-signature providers, and core banking systems through open APIs. This is what prevents data silos from forming between your tools.

- Borrower-facing portals. Borrowers track their application status in real time. That transparency reduces inbound calls and speeds up document collection.

- Reporting dashboards. Loan officers and managers see pipeline health, bottlenecks, and team performance at a glance. Decisions get made on data, not gut feel.

- Cloud deployment with role-based access. Encryption and permission controls protect sensitive borrower data while keeping the platform accessible from anywhere.

Pro Tip: Prioritize API openness above feature count when evaluating platforms. A system with 40 features but no open API will trap your data and block future integrations as your business grows.

One common misconception is that compliance is a separate layer you add on top of the LOS. The best loan origination software treats compliance as a frontline workflow check, not an afterthought. That shift from reactive to proactive compliance is one of the clearest signs of a mature platform.

How does a loan origination system improve lending efficiency?

The operational case for a modern LOS is straightforward. Cloud-based LOS platforms cut product launch timelines by 50–75% by enabling parallel processing and eliminating sequential handoffs. That means a loan that once took weeks to move from application to approval can move in days.

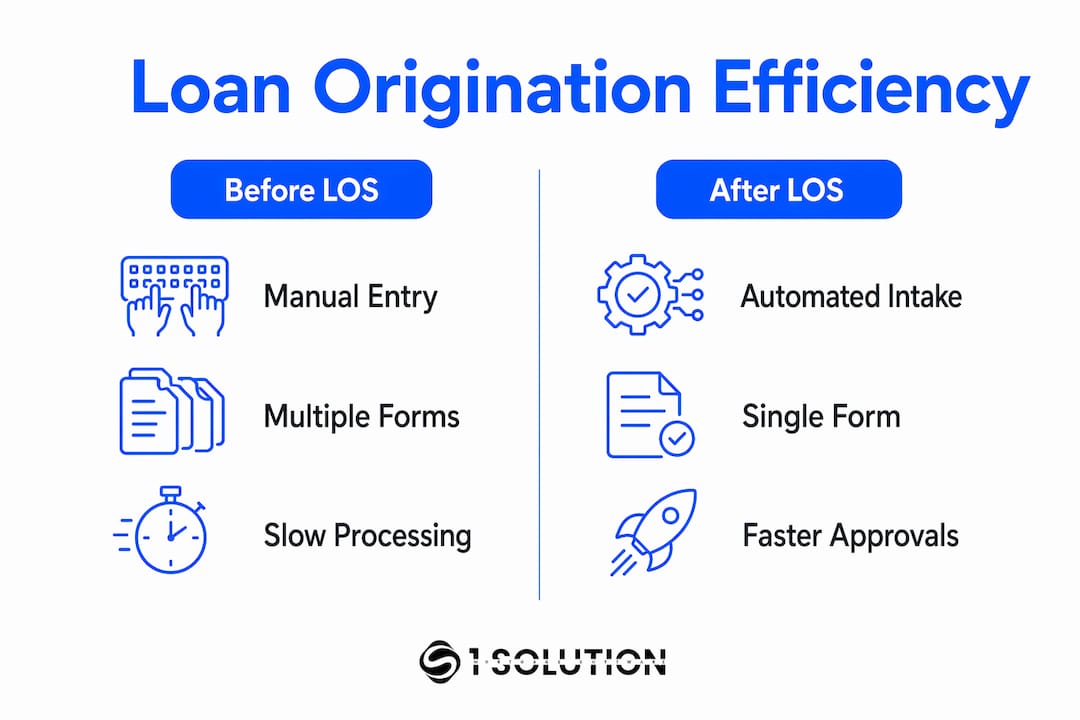

The table below shows what changes operationally when brokers move from manual workflows to a unified LOS:

| Operational Area | Before LOS | After LOS |

|---|---|---|

| Application intake | Manual data entry, multiple forms | Single digital intake, auto-populated fields |

| Credit decisioning | Processor pulls reports manually | Automated bureau pull and rule-based decision |

| Compliance checks | End-of-process audit review | Real-time rule engine flags issues at intake |

| Document collection | Email and fax, tracked in spreadsheets | Borrower portal with automated reminders |

| Turnaround time | Weeks per file | Days per file with parallel task processing |

| Audit trail | Reconstructed manually | Auto-generated and timestamped throughout |

The efficiency gains are not just about speed. Automation removes the human error that creeps into manual data re-entry across disconnected systems. When a borrower's income figure is entered once and flows through every downstream step automatically, the risk of a typo derailing a closing drops sharply.

Pro Tip: Before going live on a new LOS, map every current workflow step on paper first. The platform will automate what you give it. If your current process has gaps, the LOS will automate those gaps too.

Compliance automation deserves special attention here. Embedded compliance features reduce manual workload, improve audit trails, and increase regulatory adherence. That is not a minor operational benefit. It is the difference between a clean exam and a corrective action plan.

What criteria should you use to choose the best loan origination software?

Selecting lending management software is a long-term business decision. Eight critical evaluation criteria in 2026 are configurability, API integration, AI decisioning, compliance automation, cloud scalability, user experience, reporting and analytics, and vendor stability. Each one matters, but they do not all carry equal weight for every business.

The table below breaks down each criterion with what to look for and where brokers commonly get burned:

| Criterion | What to look for | Common pitfall |

|---|---|---|

| Configurability | Low-code rule editors, custom workflows | Assuming defaults match your credit policy |

| API integration | Open REST APIs, documented endpoints | Choosing a closed system that blocks future tools |

| AI decisioning | Explainable models, override controls | Black-box decisions that fail regulatory review |

| Compliance automation | TILA, SCRA, OFAC rule engines | Treating compliance as a post-process add-on |

| Cloud scalability | Multi-tenant architecture, uptime SLAs | On-premise systems that cap growth |

| User experience | Intuitive UI, minimal training time | Complex interfaces that slow adoption |

| Reporting and analytics | Real-time dashboards, exportable data | Static reports that require IT to generate |

| Vendor stability | Funding history, client retention rate | Choosing a startup with no track record |

Choosing a closed-box LOS can create new data silos that block growth. That trade-off between all-in-one convenience and integration flexibility is the most consequential decision brokers face. An all-in-one platform with open APIs gives you the best of both worlds. A closed all-in-one gives you convenience today and constraints tomorrow.

Business-led configuration is another point most brokers underestimate. Your credit logic, underwriting rules, and compliance requirements must be mapped and documented before the technical team touches a single setting. The platform reflects your business decisions. If those decisions are not clear before implementation, the platform will reflect the confusion.

Vendor stability matters more than most brokers realize. A platform built by a team with no lending background will require you to explain your own business to them repeatedly. Platforms built by practitioners, like 1 Solution Mortgage Software, start from a position of understanding the broker's actual workflow rather than guessing at it.

How does an LOS fit into the broader lending technology ecosystem?

A loan origination system is not the only platform in a lender's technology stack. Understanding where it starts and stops is critical to avoiding operational confusion.

LOS manages pre-disbursement lending processes. LMS handles post-disbursement servicing tasks like collections, payment processing, and account management. Confusing the two leads to system failures and gaps in the borrower experience. The LOS closes the loan. The loan management system (LMS) services it afterward.

Within the pre-disbursement phase, a well-designed LOS connects to a wide range of external tools through APIs:

- Credit bureaus (Equifax, Experian, TransUnion) for automated credit pulls and score retrieval

- CRM platforms for lead management, borrower communication history, and pipeline tracking

- E-signature tools for digital document execution without printing or scanning

- Fraud detection services for identity verification and synthetic identity screening

- Core banking systems for fund disbursement triggers and account creation

- Payment gateways for application fee collection and rate lock deposits

API-first architecture prevents fragmentation and supports real-time data flow across all of these tools. When the LOS and CRM share live data, a loan officer sees the full borrower picture without switching tabs or re-entering information. That is the practical value of integration done right.

Brokers who want a deeper look at how these tools fit together can read about mortgage automation tools and the broader mortgage broker platform landscape. Understanding the full stack makes LOS selection a much clearer decision.

The most common integration failure is not a technical one. It is organizational. Teams assume the LOS will automatically sync with every existing tool. Without deliberate API configuration and data mapping, the result is a new system running in parallel with the old ones, which defeats the purpose entirely.

Key Takeaways

A loan origination system is only as effective as the workflows, data quality, and integration architecture built around it.

| Point | Details |

|---|---|

| LOS automates pre-disbursement | It consolidates 7–10 manual processes from application intake through approval into one workflow. |

| Compliance must be embedded | TILA, SCRA, and OFAC controls built into the workflow prevent violations before they occur. |

| API-first design is non-negotiable | Open APIs connect the LOS to credit bureaus, CRM, e-sign, and banking systems without data silos. |

| LOS and LMS serve different phases | LOS handles origination; LMS handles post-disbursement servicing. Confusing them causes operational gaps. |

| Business-led configuration wins | Map your credit logic and compliance rules before technical implementation begins. |

What I've learned after 20 years of watching LOS implementations succeed and fail

The most expensive mistake I see brokers make is treating LOS selection as a software purchase rather than a business transformation. They evaluate features, negotiate pricing, and sign a contract. Then they import their existing data and workflows directly into the new system. Six months later, they are frustrated that the platform is not delivering the efficiency gains they expected.

The reason is almost always the same. Importing legacy data without cleanup leads to ineffective automation and errors. The LOS did not fail. It automated a broken process at higher speed. The inefficiency was always there. The platform just made it more visible and more expensive.

My honest advice: spend as much time cleaning up your internal data and documenting your workflows as you spend evaluating vendors. That work is unglamorous. It does not show up in a demo. But it is what separates a successful implementation from a costly one.

The second pattern I see consistently is brokers choosing feature breadth over integration capability. A platform with 60 features and a closed architecture will limit you within two years. A platform with 40 features and open APIs will grow with you. Effective deployment requires business-led configuration to map credit logic and compliance before the technical rollout begins. That is not a vendor's job. It is yours.

Finally, treat your LOS as a living platform, not a one-time purchase. Regulations change. Your product mix changes. Your team grows. The system needs to evolve with the business. Vendors who build for that reality are worth paying more for. Vendors who sell you a static product and disappear after go-live are not.

— Omar Khamisa

Why 1 Solution Mortgage Software is built for brokers who need a real LOS

Independent mortgage brokers deserve a platform built from actual lending experience, not one retrofitted from a bank product.

1 Solution Mortgage Software brings LOS, CRM, POS, compliance, pricing, and communication tools into one connected platform built specifically for independent mortgage professionals. The system is configurable, cloud-deployed, and built with open architecture so your tools work together rather than against each other. Founded by Omar Khamisa after 20 years working as a processor, underwriter, loan originator, and systems consultant, 1 Solution Mortgage Software reflects the real workflows brokers run every day. If you are ready to replace fragmented tools with a platform that actually fits your business, 1 Solution is worth a close look.

FAQ

What is a loan origination system (LOS)?

A loan origination system is a software platform that automates the pre-disbursement lending lifecycle, covering application intake, credit decisioning, compliance checks, and documentation. It replaces manual, disconnected processes with one integrated workflow.

How is an LOS different from a loan management system (LMS)?

An LOS manages the origination process from application through approval and closing. An LMS handles post-disbursement servicing tasks like payment collection and account management. Using one system for both functions without clear role separation causes operational gaps.

What compliance regulations should a mortgage LOS cover?

A mortgage LOS should embed automated controls for TILA, SCRA, and OFAC at minimum. These rules govern disclosure timing, servicemember protections, and sanctions screening. Platforms that enforce these rules in real time reduce audit risk significantly.

Why does API-first architecture matter when choosing loan lending software?

API-first design allows the LOS to connect directly with credit bureaus, CRM platforms, e-signature tools, and core banking systems. Without open APIs, data must be moved manually between systems, which creates errors and slows every loan file.

How long does it take to implement a loan origination system?

Implementation timelines vary based on business complexity and data readiness. Cloud-based, configurable platforms can compress setup from months to weeks, but only when internal workflows and credit logic are documented and clean before the technical rollout begins.