Mortgage document packaging is defined as the systematic assembly of all required loan paperwork into a single, structured, lender-ready file used to assess and approve a mortgage application. The industry term for this process is "loan file compilation," though mortgage professionals widely use "document packaging" to describe the same workflow. A complete package includes income verification, asset statements, credit documentation, property records, and compliance disclosures organized to meet lender and regulatory standards. Poor packaging is one of the leading causes of underwriting delays, loan rejections, and compliance failures. Getting this process right from the start protects your pipeline and your reputation.

What is mortgage document packaging and what goes inside?

Mortgage document packaging covers five core document categories. Each category serves a specific underwriting purpose, and missing even one page can trigger a condition or rejection.

Income verification is the foundation of every package. This includes W-2s for the past two years, recent pay stubs, federal tax returns, and Verification of Employment (VOE) forms. Self-employed borrowers require two years of business returns plus a year-to-date profit and loss statement.

Asset documentation proves the borrower has funds to close. Asset statements must cover the most recent 60 days, typically two full monthly statements, and every page must be included. A single missing page is one of the most common reasons lenders issue conditions.

Property documents tie the loan to the collateral. The purchase contract, homeowners insurance binder, HOA certification (when applicable), and the appraisal report all belong here. The appraisal must match the property address on the application exactly.

Credit documentation includes the tri-merge credit report, payoff letters for debts being satisfied at closing, and any required disclosures. Letters of explanation (LOEs) for derogatory credit, large deposits, or employment gaps belong in this section as well.

Loan-type specific documents round out the package. VA loans require a Certificate of Eligibility and DD-214. FHA loans need a case number assignment and the FHA appraisal addendum. USDA loans require income eligibility certification. Submitting without these documents wastes everyone's time.

| Document Category | Key Items | Coverage Requirement |

|---|---|---|

| Income verification | W-2s, pay stubs, tax returns, VOE | 2 years history, 30-day pay stubs |

| Asset statements | Bank and brokerage accounts | Most recent 60 days, all pages |

| Property records | Purchase contract, appraisal, insurance | Current and property-specific |

| Credit documentation | Credit report, payoff letters, LOEs | Dated within lender guidelines |

| Loan-type documents | VA COE, FHA case number, USDA cert | Program-specific requirements |

How to package mortgage documents for lender submission

The technical format of your package matters as much as its contents. Lenders use automated document review systems, and a file that fails format checks gets flagged before a human ever reads it.

The industry standard is a single, OCR-ready PDF with continuous pagination, descriptive bookmarks, and a hyperlinked index at the front. OCR scanning at 200–300 dpi keeps text legible and machine-readable. Image-only scans fail automated checks at most lenders and cause immediate rejections.

File size is a practical constraint. Lender portals cap uploads at 50MB, but the optimal submission range is 20–30MB. Compress images without sacrificing legibility. A bloated file slows processing; an over-compressed file creates illegible documents.

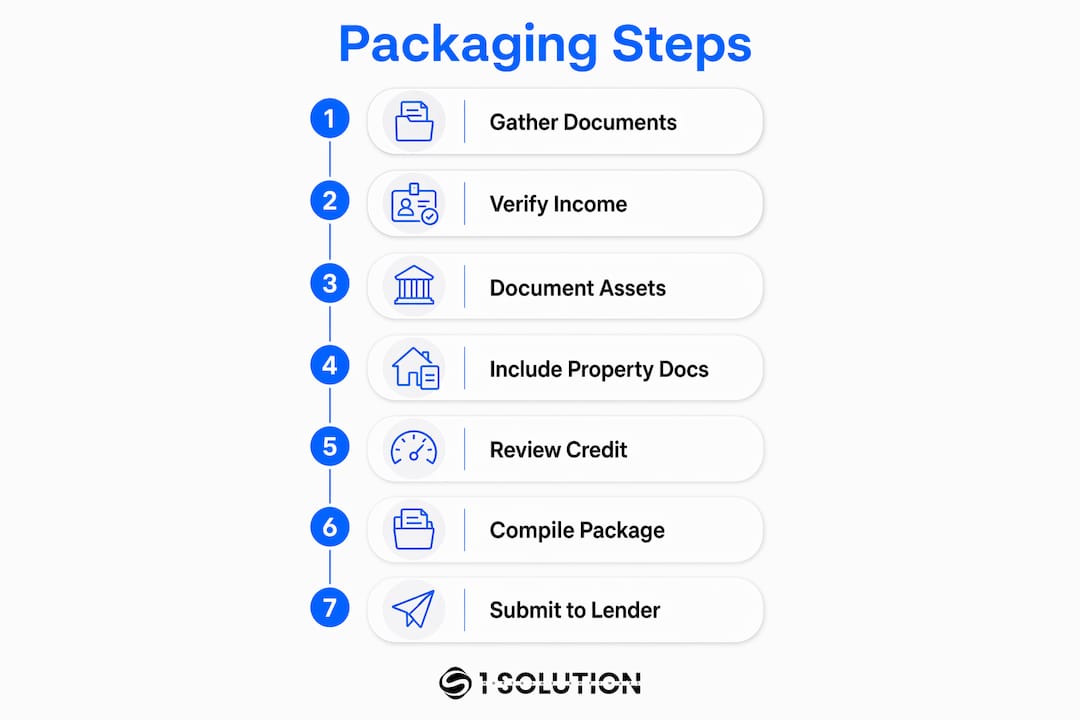

Follow these steps to build a submission-ready package:

- Collect all documents in their original digital format before combining anything. Avoid scanning already-digital documents, which degrades quality.

- Organize by category using the five sections above. Income first, then assets, credit, property, and loan-type documents.

- Add a cover page and deal summary at the front. One page summarizing the borrower profile, loan purpose, and key figures saves underwriter time.

- Combine into a single PDF with continuous page numbers. Page 1 starts at the cover and runs through the last document.

- Add bookmarks and a hyperlinked index. Missing bookmarks cause lenders to reject submissions or issue clarifications. Every major section needs a named bookmark.

- Apply a consistent file naming convention. Use a format like: LastName_FirstName_LoanNumber_Date.pdf. Version control prevents the wrong file from being submitted.

- Submit before lender cut-off times. Late uploads risk delaying closings and fund disbursement. Know your lender's portal deadline and build in a 30-minute buffer.

Pro Tip: Send fragmented email attachments only as a last resort. Combining everything into one file reduces the risk of a document getting lost and cuts lender review time significantly.

How does automation change the mortgage documentation process?

Basic OCR reads text from a scanned page. Intelligent Document Processing (IDP) goes further. IDP classifies each page by document type, extracts specific data fields using schema-driven rules, and validates that data against other documents in the file. The difference in accuracy and speed is substantial.

IDP systems in 2026 classify and extract data from loan files up to 500 pages in a single pass. That means a processor no longer manually indexes a 300-page file. The system identifies the W-2, the bank statement, and the appraisal automatically, then routes each to the correct underwriting queue.

Cross-document validation is where automation delivers its clearest compliance benefit. The system compares the borrower's name, address, and income figures across every document simultaneously. Real-time data validation saves lenders 130–160 hours per 1,000 loans processed. That is not a marginal gain. It is the difference between a three-person processing team handling 50 loans a month and handling 150.

Modern automation systems classify each page, split large files into logical bundles, extract key fields, and flag missing or mismatched content before the file reaches an underwriter. The practical result is fewer conditions, fewer rework cycles, and faster closings.

Integration with a Loan Origination System (LOS) closes the loop. When IDP connects directly to your mortgage automation tools, extracted data flows into the LOS without manual re-entry. That eliminates a major source of data entry errors and keeps the audit trail clean from intake to closing.

- Classification accuracy: IDP identifies document types across varied formats without manual sorting.

- Schema-driven extraction: Predefined field maps pull borrower name, income, account numbers, and property address consistently.

- Cross-document validation: Flags discrepancies between the 1003, tax returns, and bank statements before underwriting.

- Compliance audit trail: Every action is logged with a timestamp, supporting regulatory review.

- LOS integration: Extracted data populates the loan file directly, removing duplicate data entry.

Common challenges in mortgage document packaging and how to fix them

Incomplete documentation is the most common reason a loan file stalls. A missing page from a bank statement or an unsigned disclosure triggers a condition that adds days to the timeline. The fix is a pre-submission checklist tied to the specific loan type and lender guidelines. Check every requirement before the file leaves your desk.

Lenders relying on manual sorting face compounding risks as loan volume grows. A processor managing 20 files manually can keep up. At 60 files, errors multiply. Automation is not a luxury at scale. It is a quality control requirement.

Presentation quality directly affects underwriting speed. A clean, well-indexed deal summary can reduce underwriter review time by half. That one page at the front of the package tells the underwriter the borrower's story before they open a single document. For complex files with multiple income sources, gaps in employment, or non-warrantable properties, a deal summary is not optional. It is the difference between a quick approval and a long list of conditions.

Compliance documentation requires its own discipline. Every disclosure must be signed, dated, and within the required delivery window. The mortgage underwriting process depends on a complete compliance trail. A missing RESPA disclosure or an unsigned Loan Estimate can delay closing or trigger a regulatory finding.

Pro Tip: Build a lender-specific checklist for every investor you submit to regularly. Lender overlays change, and a checklist that was accurate six months ago may be missing a new requirement today.

- Audit your package against the lender's guidelines, not just agency guidelines.

- Include letters of explanation proactively for any item an underwriter might question.

- Maintain version control so the submitted file and the file in your system match exactly.

- Log every document received, reviewed, and submitted with timestamps for your audit trail.

- Review loan approval speed factors regularly to identify where your process creates bottlenecks.

Key Takeaways

Mortgage document packaging quality directly determines underwriting speed, compliance outcomes, and loan approval rates for every file you submit.

| Point | Details |

|---|---|

| Complete documentation prevents delays | Asset statements need all pages for the most recent 60 days; income docs need 30-day coverage. |

| Format standards matter as much as content | Submit a single OCR-ready PDF at 20–30MB with bookmarks and a hyperlinked index. |

| Automation reduces errors at scale | IDP systems save 130–160 hours per 1,000 loans by validating data across documents automatically. |

| Deal summaries accelerate underwriting | A one-page summary at the front of complex files can cut underwriter review time by half. |

| Lender-specific checklists prevent conditions | Agency guidelines are the floor; lender overlays add requirements that change regularly. |

What 20 years in mortgage operations taught me about packaging

I have worked every seat in this industry: processor, underwriter, loan originator, and systems consultant. The one thing that separates the brokers who close fast from the ones who chase conditions is how they present a file.

Most professionals treat packaging as an administrative task. It is not. It is a communication act. When an underwriter opens your file, they are forming an opinion about the borrower and about you within the first two minutes. A disorganized file signals a disorganized broker. A clean, indexed, well-summarized package signals a professional who has already done the underwriter's job for them.

The shift to automation is real and it is necessary. I have seen processors drown in manual indexing at volumes that should be manageable. The brokers who adopted intelligent document processing early are not just faster. They have fewer buybacks, fewer compliance findings, and better lender relationships. That is a compounding advantage.

The deal summary is the most underused tool in this business. I have watched a one-page summary turn a file that would have generated ten conditions into a clean approval. Write it like you are briefing a senior underwriter who has 90 seconds to understand the borrower's situation. Lead with the loan purpose, the key income figure, the LTV, and any complexity that needs context. Then let the documents prove it.

Lender guidelines change constantly. The brokers who get burned are the ones running on memory instead of current checklists. Build the habit of reviewing your lender overlays quarterly. It takes 20 minutes and it prevents the kind of last-minute condition that blows a closing date.

Finally, packaging is a team sport. Your processor, your loan officer assistant, and your compliance coordinator all touch the file. When everyone understands the standard, the package quality goes up and the rework goes down. Train your team on the format, not just the checklist.

— Omar Khamisa

How 1 Solution Mortgage Software handles document packaging

Mortgage professionals who want to move faster without adding headcount need a platform built for the way brokers actually work.

1 Solution Mortgage Software integrates document classification, extraction, and validation directly into the loan workflow. The platform connects with your existing intake process and produces lender-ready, compliant packages without manual indexing or reformatting. Processors spend less time organizing files and more time closing loans. The built-in compliance tools maintain a clean audit trail from document receipt to submission. For brokers managing growing pipelines, 1 Solution brings together the LOS, compliance, and document management functions that typically require three separate tools. Visit 1 Solution Mortgage Software to see how the platform fits your operation.

FAQ

What is mortgage document packaging?

Mortgage document packaging is the process of assembling all required loan documents into a single, organized, lender-ready file. It includes income, asset, credit, property, and compliance documents structured to meet lender and regulatory standards.

What format should a mortgage document package use?

The industry standard is a single OCR-ready PDF with continuous pagination, descriptive bookmarks, and a hyperlinked index, compressed to 20–30MB for portal submission.

How does automation improve the mortgage documentation process?

Intelligent Document Processing classifies, extracts, and validates data across a full loan file automatically. Cross-document validation saves lenders 130–160 hours per 1,000 loans by catching discrepancies before underwriting.

What documents are required for a complete mortgage package?

A complete package includes W-2s, pay stubs, tax returns, 60-day asset statements, a tri-merge credit report, property documents, and any loan-type specific forms such as a VA Certificate of Eligibility or FHA case number assignment.

Why do mortgage packages get rejected?

The most common causes are missing document pages, non-OCR scans, files that exceed portal size limits, and absent bookmarks or indexes. Reviewing your mortgage file submission process against lender-specific guidelines before upload prevents most rejections.