Mortgage live rates are the continuously updated interest rates reflecting current borrowing costs across all major loan products. Unlike the static figures printed in brochures, these rates shift throughout the trading day in response to bond markets, economic data, and lender decisions. As of june 22, 2026, average 30-year fixed rates sit between 6.589% and 6.66% depending on the index you consult. That gap matters. Knowing which source to trust, when to act, and how to lock a rate before it moves is the difference between a manageable payment and one that stretches your budget.

What drives mortgage live rates up and down each day?

Mortgage live rates are not set once and left alone. Lenders adjust rates multiple times daily based on real-time movements in bond markets and Treasury yields. That means the rate you see at 9 a.m. may not exist by noon.

The single most important market signal is the 10-year Treasury yield. When Treasury yields rise, mortgage rates follow. The 10-year Treasury yield rose 3.2 basis points on june 19, 2026, and lenders repriced within hours. Bond markets react instantly to any news that changes the inflation or growth outlook, and mortgage pricing follows that reaction.

Economic data releases create the sharpest intraday swings. The Jobs Report, CPI, and GDP releases all cause rapid daily adjustments in mortgage pricing. A stronger-than-expected jobs number signals inflation risk, which pushes yields up and rates with them. A weak number does the opposite. Borrowers who know a major data release is scheduled can time their rate lock conversations accordingly.

Loan type also determines the rate you actually receive. FHA, VA, Conventional, and Jumbo loans each carry different live rate behaviors because they represent different risk profiles for lenders and investors. Federal Reserve policy adds another layer. Mortgage rates remain elevated due to market expectations of prolonged Fed rate hikes, which continue to pressure affordability across all loan categories.

Key factors that move rates on any given day:

- 10-year Treasury yield movements: The primary benchmark lenders watch in real time.

- Mortgage-backed securities (MBS) pricing: Lenders price loans off MBS spreads, not just Treasuries.

- Federal Reserve communications: Speeches, meeting minutes, and rate decisions shift expectations fast.

- Scheduled economic releases: Jobs Report, CPI, and GDP are the highest-impact events.

- Lender-specific capacity: A lender with a full pipeline may raise rates to slow volume, regardless of market conditions.

Pro Tip: Set a Google alert for "10-year Treasury yield" and check it before calling your lender. If yields spiked that morning, rates likely moved up. If they dropped, you may have a window to lock at a better number.

How do major mortgage rate indexes compare?

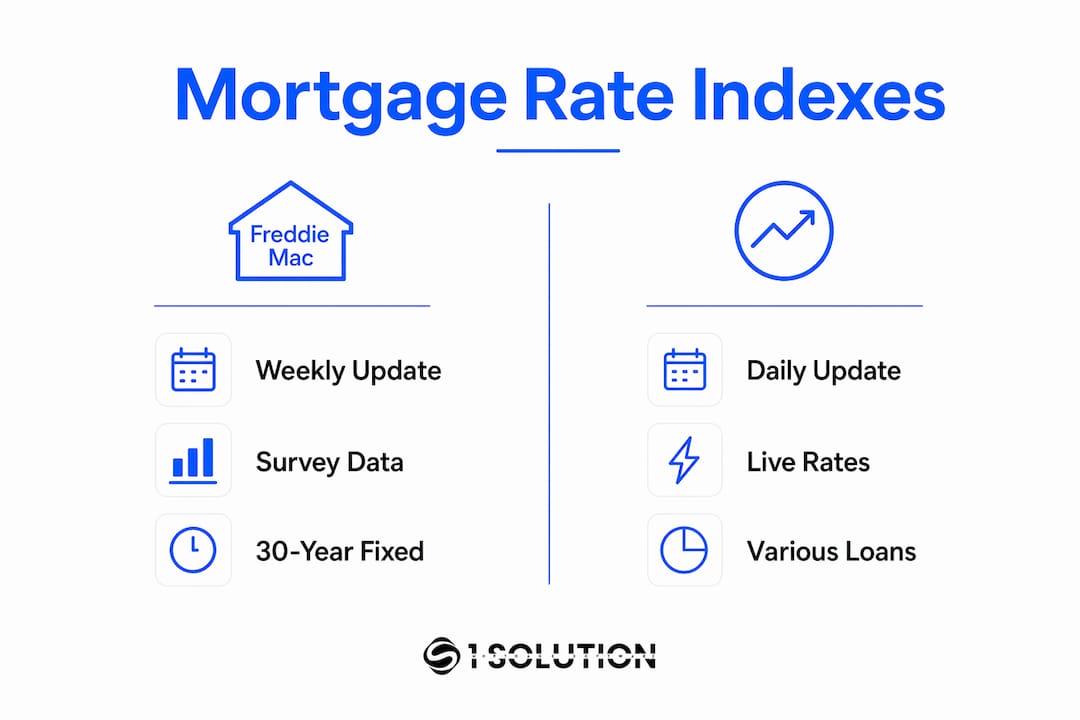

Not all rate indexes are created equal. Freddie Mac, Mortgage News Daily, and the Mortgage Bankers Association each publish rate data, but they use different methodologies, update frequencies, and borrower profiles. Treating them as interchangeable leads to confusion.

Freddie Mac's weekly 30-year fixed rate average is approximately 6.47%, while Mortgage News Daily reports a daily average around 6.66%. That 0.19 percentage point gap is not an error. Freddie Mac surveys lenders earlier in the week and publishes on thursdays, so its data can lag real market conditions by several days. Mortgage News Daily pulls from actual lender rate sheets daily, making it the faster signal.

| Index | Update frequency | Loan types covered | Typical rate profile |

|---|---|---|---|

| Freddie Mac PMMS | Weekly (thursdays) | 30-year and 15-year fixed | Best-case borrower, national average |

| Mortgage News Daily | Daily | 30-year fixed, FHA, Jumbo | Real-time lender sheet average |

| MBA Weekly Survey | Weekly (wednesdays) | Purchase and refinance, multiple types | Application-weighted average |

The Freddie Mac Primary Mortgage Market Survey (PMMS) is the most cited index in news coverage, but it reflects a sample of lenders and assumes a well-qualified borrower with a 20% down payment. The MBA survey weights rates by actual loan applications, which skews it toward the loan types borrowers are actually closing. Mortgage News Daily is the closest thing to a live ticker for daily rate watchers.

Knowing which index to use depends on your goal. For a broad market trend, Freddie Mac works. For a real-time read before a rate lock conversation, Mortgage News Daily is the more current source. For understanding what borrowers are actually paying on closed loans, the MBA survey adds context.

How to use current mortgage rates in your buying or refinancing process

Tracking rates is only useful if you act on the information correctly. The process breaks down into four practical steps.

-

Set up real-time alerts. Most lender apps and aggregator platforms like NerdWallet and The Mortgage Reports allow rate alerts by email or push notification. Configure alerts for your target rate and loan type. This removes the need to check manually every day.

-

Understand rate lock timing. A rate lock guarantees your interest rate during underwriting for a defined period, typically 30–60 days. Lock timing is as critical as the rate itself because intraday fluctuations can move a rate by 0.125% or more between morning and afternoon. Ask your lender what time of day they reprice and plan your lock conversation accordingly.

-

Know when refinancing makes sense. Refinancing is worth pursuing when current market rates are at least 0.5–0.75 percentage points lower than your existing mortgage rate. Run a break-even calculation: divide your closing costs by your monthly savings to find how many months it takes to recoup the cost. If you plan to move before that break-even point, refinancing does not benefit you financially.

-

Align rate decisions with your personal finances. There is no perfect timing universally. Affordability and personal financial alignment matter more than chasing a lower rate that may never arrive. Build your budget around current rates, not projected ones. Use a mortgage scenario analysis to model different rate and payment combinations before committing.

Pro Tip: Ask your lender about float-down options when locking. A float-down provision lets you capture a lower rate if the market improves before closing. Not all lenders offer it, and it sometimes costs a small fee, but it provides real protection in a volatile rate environment.

Common misconceptions about live mortgage rate updates

The biggest mistake borrowers make is treating advertised rates as the rate they will receive. Rates quoted online reflect best-case scenarios for highly qualified borrowers, typically those with credit scores above 760, low debt-to-income ratios, and 20% down payments. Most borrowers receive a rate that is higher than the headline figure.

Several other misconceptions consistently cost borrowers money:

- "The national average is my rate." National averages blend thousands of loan profiles. Your actual rate depends on your credit score, loan-to-value ratio, property type, and loan amount. A borrower with a 680 credit score will see a meaningfully higher rate than the published average.

- "Rates are stable during the day." Lenders reprice multiple times daily. A rate sheet from 8 a.m. may be replaced by 1 p.m. Calling your lender in the morning and locking in the afternoon without confirming the current rate is a real risk.

- "All lenders offer the same rate for the same loan." Lender margins, operational costs, and investor relationships all affect pricing. Comparing lender-specific live quotes for your exact loan profile is the only way to find the best price. Getting three to five quotes on the same day, for the same loan type, is the standard practice that consistently saves borrowers money.

- "FHA rates are always lower than Conventional rates." FHA loans carry mortgage insurance premiums that affect the total cost of borrowing. The note rate may look lower, but the annual percentage rate (APR) often tells a different story.

Understanding these distinctions separates borrowers who get good deals from those who accept the first number they see.

Key takeaways

Tracking mortgage interest rates live is only valuable when you know how to interpret what you see and act on it at the right moment.

| Point | Details |

|---|---|

| Rates move multiple times daily | Lenders reprice based on Treasury yields and MBS markets, so lock timing matters as much as the rate itself. |

| Index choice affects your read | Freddie Mac lags by days; Mortgage News Daily reflects real-time lender sheets and is better for daily decisions. |

| Advertised rates are not your rate | Published averages assume top-tier borrowers; get lender-specific quotes for your actual loan profile. |

| Refinance requires a clear break-even | A 0.5–0.75 point rate reduction is the minimum threshold; calculate months to recoup closing costs before deciding. |

| Personal finances outweigh market timing | Affordability today beats waiting for a rate that may not arrive; build your budget around current numbers. |

Why I stopped waiting for the perfect rate

I have spent over 20 years in mortgage operations, working as a processor, underwriter, loan originator, and systems consultant. The single most common mistake I watched borrowers make was waiting. They would track rates daily, see a number they liked, then hesitate. By the time they called their lender, the rate had moved. Then they would wait again.

The market does not reward patience the way borrowers expect. Bond yields and inflation expectations shift faster than most people realize, and the Federal Reserve's rate policy has made the rate environment less predictable than any point in the past decade. Waiting for a specific number is a strategy built on hope, not data.

What actually works is building your purchase decision around what you can afford at today's rates, then locking the moment you find a rate that fits your budget. Technology helps. Platforms that deliver live mortgage updates and automated comparisons give you the information you need without the daily manual effort. The brokers I have seen serve their clients best are the ones who use real-time data tools and act decisively when the window opens. Continuous education about what moves rates, combined with the right technology, is the only reliable edge in this market.

— Omar Khamisa

How 1 Solution Mortgage Software keeps you ahead of rate changes

Rate information is only useful when you can act on it fast. 1 Solution Mortgage Software was built by mortgage professionals who know what it costs to work with fragmented, slow, or outdated tools.

The platform brings pricing, CRM, POS, LOS, and compliance tools into one connected system designed for independent mortgage professionals. Brokers using 1 Solution get updated rate data and automated loan comparisons without switching between five different platforms. That speed matters when rates reprice at noon and your borrower needs an answer by end of day. For homebuyers working with a broker, it means faster quotes and more accurate comparisons across loan types. Visit 1 Solution Mortgage Software to see how the platform delivers the rate transparency and operational control that independent brokers and their clients deserve.

FAQ

What are mortgage live rates?

Mortgage live rates are real-time interest rates that lenders update throughout the trading day based on bond market movements and Treasury yields. They differ from weekly published averages because they reflect current lender pricing, not lagged survey data.

How often do mortgage rates change in a single day?

Lenders reprice mortgage rates multiple times daily, often two to four times, depending on bond market activity. Major economic data releases like the Jobs Report or CPI can trigger immediate repricing within minutes of publication.

What is the difference between Freddie Mac and Mortgage News Daily rates?

Freddie Mac publishes a weekly average on thursdays using a lender survey, while Mortgage News Daily pulls from actual lender rate sheets every day. Freddie Mac's rate is approximately 6.47% versus Mortgage News Daily's daily average of around 6.66% as of june 2026.

When should I lock my mortgage rate?

Lock your rate when you find a number that fits your budget and your closing timeline falls within the lock period, typically 30–60 days. Float-down options provide additional protection if rates drop after you lock.

How do I compare mortgage rates accurately?

Get lender-specific quotes for your exact loan type, credit score, and down payment on the same day. National averages reflect best-case borrower profiles and do not represent what most borrowers actually receive.