Compliance in new mortgage businesses is defined as the operational framework that governs legal adherence, risk control, and ethical conduct across every loan transaction. The role of compliance in new mortgage businesses goes far beyond filing paperwork. It determines whether your company survives its first regulatory exam, earns trust from secondary market investors, and builds a reputation that sustains long-term growth. Federal bodies including the Consumer Financial Protection Bureau (CFPB), the Financial Crimes Enforcement Network (FinCEN), and the Nationwide Multistate Licensing System (NMLS) each impose distinct obligations on new lenders and brokers. Key frameworks such as HMDA/Reg C, the SAFE Act, the Bank Secrecy Act (BSA), and TILA/RESPA form the legal backbone every new mortgage business must understand before originating a single loan.

What are the key regulatory compliance requirements for new mortgage companies?

New mortgage companies operate under a layered system of federal and state regulations. Each layer carries its own documentation requirements, reporting deadlines, and enforcement consequences.

The core federal frameworks every new mortgage business must address include:

- HMDA/Reg C: The Home Mortgage Disclosure Act requires lenders to collect, record, and report loan application data by race, income, and geography. HMDA/Reg C violations represented 38% of all cited consumer violations for state member banks in 2024. That figure shows HMDA is the single highest-risk reporting obligation for new lenders.

- SAFE Act licensing: Every mortgage loan originator (MLO) must hold a valid license through the NMLS. State-specific education, testing, and background check requirements apply before any origination activity begins.

- TILA/RESPA (TRID): The Truth in Lending Act and Real Estate Settlement Procedures Act require accurate Loan Estimates and Closing Disclosures within strict delivery timelines. Errors trigger both consumer harm and exam findings.

- ECOA/Reg B: The Equal Credit Opportunity Act prohibits discrimination in credit decisions. New businesses must document adverse action notices and maintain consistent underwriting criteria.

- BSA AML obligations: Residential mortgage lenders are classified as financial institutions under the Bank Secrecy Act. That classification requires a written Anti-Money Laundering program, employee training, and Suspicious Activity Report (SAR) filing when red flags appear.

State-level requirements add another layer. Most states mandate separate licensing through NMLS, annual renewal, surety bonds, and net worth minimums. Some states require additional reporting through their own examination systems. Ignoring state-specific rules is one of the fastest ways a new mortgage business triggers a regulatory action before it reaches its second year of operation.

Recordkeeping standards apply across all of these frameworks. Loan files, borrower communications, and compliance decisions must be retained for defined periods, typically three to seven years depending on the regulation. Gaps in documentation are not just administrative problems. They become evidence of program failure during exams.

How do new mortgage businesses operationalize compliance management effectively?

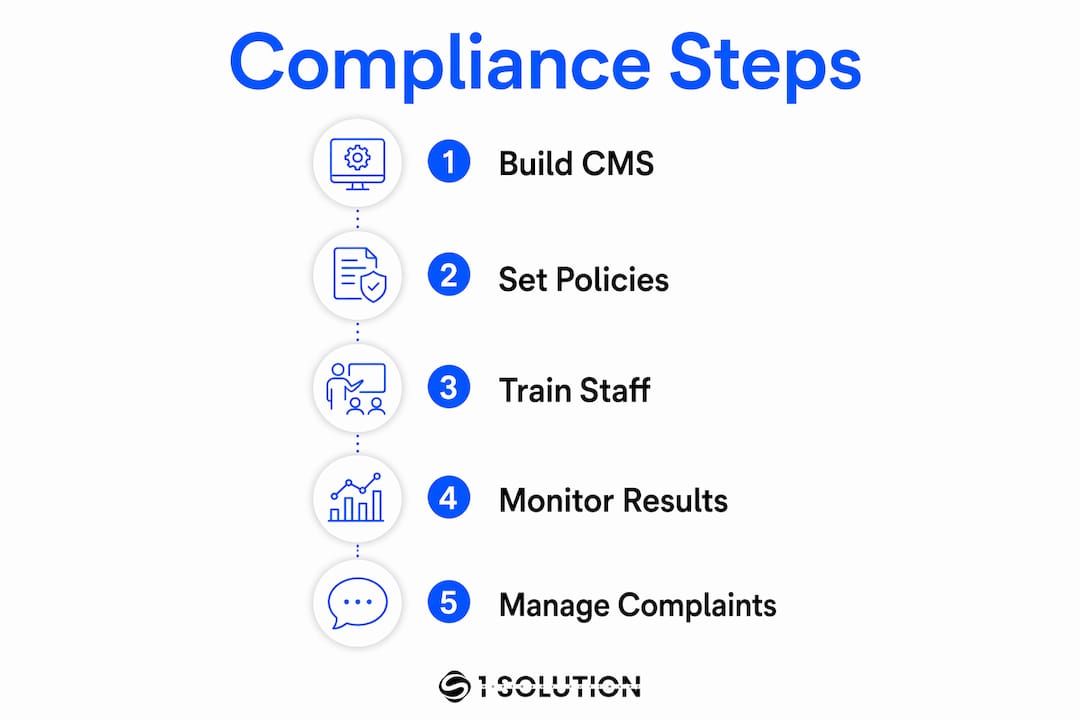

A Compliance Management System (CMS) is the structured program that connects your policies, training, monitoring, and corrective action into one operating cycle. The CFPB evaluates every supervised entity against its CMS components. Building one from day one is not optional.

Here is how to build a functional CMS as a new mortgage business:

- Write policies that mirror real workflows. Regulators prefer evidence that compliance reflects daily operations rather than binders that sit on a shelf. Write your procedures around what your team actually does, not what sounds good in theory.

- Staff compliance appropriately from the start. Part-time or outsourced compliance functions create gaps that show up during exams. Compliance staffing must be scaled early, even if that means a dedicated part-time hire before volume justifies a full-time role.

- Build a training program with three tiers. Onboarding training covers foundational rules for every new hire. Role-specific training addresses the regulations most relevant to each job function. Refresher training runs at least annually and updates staff on regulatory changes.

- Configure your loan origination software for compliance. Automated compliance testing saves lenders an average of 20 minutes and $14 per loan. That efficiency compounds across hundreds of loans per year and reduces the manual error rate that drives exam findings.

- Establish a complaint handling process. Every borrower complaint must be logged, investigated, and resolved within a defined timeframe. Complaint data also serves as an early warning system for systemic problems.

- Schedule independent monitoring and testing. Internal audits or third-party reviews should run at least annually. Findings must be documented, escalated to board-level oversight, and resolved through a corrective action plan.

Pro Tip: Build your compliance setup checklist before you originate your first loan. Retrofitting a CMS after volume picks up is far more expensive and disruptive than building it correctly from the start.

The CFPB's CMS review covers board oversight, written policies, training records, monitoring results, complaint handling, and audit findings. Deficiencies in any one component affect the integrity of the entire system. A strong training program cannot compensate for absent board engagement, and thorough policies mean nothing without evidence of consistent implementation.

What are common compliance risks and challenges faced by new mortgage businesses?

New mortgage businesses face a predictable set of compliance failures. Knowing them in advance gives you a real advantage.

The most common deficiencies regulators find in new mortgage operations include:

- Weak documentation: Loan files missing required disclosures, unsigned acknowledgments, or incomplete adverse action notices are the most frequent exam triggers.

- Inadequate staffing: Compliance functions assigned to processors or loan officers as secondary duties produce inconsistent results and poor audit trails.

- Poor training records: Regulators ask for proof of training completion. Verbal training with no documentation is treated the same as no training at all.

- Insufficient monitoring: New businesses often skip internal audits in their first year. That gap leaves systemic errors undetected until an examiner finds them.

- HMDA data quality problems: HMDA/Reg C violations represented 38% of cited violations for state member banks in 2024. Data entry errors, missing fields, and incorrect geocoding are the most common causes.

Vendor management is a frequently overlooked risk area. When you use third-party settlement service providers, appraisers, or technology vendors, their compliance failures can become your exam findings. New businesses rarely have formal vendor oversight programs in place, which creates exposure.

Inconsistent borrower communications and poor record-keeping are among the most common early triggers for regulatory red flags during exams. A borrower who receives different fee estimates from two loan officers at the same company creates a fair lending risk that examiners take seriously.

The consequences of compliance gaps extend beyond fines. Enforcement actions become public record. Secondary market investors and warehouse lenders review your compliance history before extending credit lines. A single material finding can cost a new business its most important funding relationships at exactly the wrong moment.

How can new mortgage businesses build a culture of compliance?

A culture of compliance means your team treats regulatory requirements as part of the job, not as obstacles to closing loans. That mindset starts at the top and gets reinforced through systems, not speeches.

Board-level visibility is the foundation. Board engagement and independent testing reduce the risk of enforcement actions. When your board reviews compliance reports quarterly and asks specific questions about findings, the entire organization treats compliance as a real priority.

Self-identification and remediation of compliance issues create a strategic advantage. When you find a problem before an examiner does, you control the narrative. You can document the issue, show your corrective action, and demonstrate a functioning oversight system. Regulators treat self-identified problems very differently from exam discoveries.

Proactive self-identification of compliance gaps, followed by documented remediation, is one of the strongest signals a new mortgage business can send to regulators and secondary market partners. It shows the program works.

Practical, short standard operating procedures (SOPs) reduce tribal knowledge and accelerate training. Building concise SOPs lowers repeat mistakes and makes onboarding faster when you add staff. A two-page SOP that your team actually follows beats a 40-page policy manual that no one reads.

Compliance programs that reflect daily operational reality are favored by regulators and secondary market partners alike. Referral partners, warehouse lenders, and investors all evaluate your compliance posture before deepening a relationship. A well-documented, consistently executed program is a competitive asset, not just a regulatory requirement.

Pro Tip: Review your compliance management approach annually against CFPB examination guidelines. Treat the review as a practice exam, not a formality. The gaps you find are far cheaper to fix internally than during an actual examination.

Understanding the broader regulatory environment also helps. The international banking compliance framework shows how financial institutions globally are moving toward integrated compliance systems. That trend applies directly to U.S. mortgage businesses building programs for 2026 and beyond.

Key Takeaways

Compliance in new mortgage businesses is the operating system that determines legal survival, exam outcomes, and long-term growth, not a back-office function to address after launch.

| Point | Details |

|---|---|

| Compliance starts before origination | Build your CMS, policies, and training program before closing your first loan. |

| HMDA data quality is the top risk | HMDA/Reg C violations led all cited consumer violations in 2024; prioritize data accuracy from day one. |

| Automation reduces cost and error | Automated compliance testing saves an average of 20 minutes and $14 per loan across your pipeline. |

| Board engagement is non-negotiable | Board-level oversight and independent testing are the strongest defenses against enforcement actions. |

| Self-identification pays off | Finding and fixing compliance gaps internally gives you control and signals a functioning program to regulators. |

Compliance as the operating system: my perspective

I have spent over 20 years working inside mortgage operations as a processor, underwriter, loan originator, and systems consultant. The pattern I have seen repeat itself across new mortgage businesses is always the same. Compliance gets treated as a task to complete rather than a system to build. That mindset is expensive.

The businesses that struggle most in their first CFPB or state exam are not the ones that broke the rules intentionally. They are the ones that assumed compliance would take care of itself once they had good people and good intentions. It does not work that way. Regulators do not grade on effort. They grade on documentation, consistency, and evidence.

What I have learned is that compliance staffing is the most undervalued investment a new mortgage business makes. Assigning compliance duties to a processor who is already managing a pipeline is not a cost-saving measure. It is a deferred penalty. The exam finding that results from that decision costs far more than the salary you avoided paying.

Automation changes this equation significantly. When your loan origination system is configured to flag exceptions, generate required disclosures automatically, and maintain a clean audit trail, your compliance officer spends time on judgment calls rather than data entry. That is the right use of a skilled person.

The businesses I have seen build lasting compliance cultures share one trait. They treat their compliance program as evidence of how they operate, not as a defense against how they might be accused of operating. That shift in framing changes everything.

— Omar Khamisa

How 1 Solution Mortgage Software supports compliance in your mortgage business

New mortgage businesses need technology that keeps compliance embedded in every workflow, not bolted on as an afterthought.

1 Solution Mortgage Software was built by mortgage professionals who understand what regulators look for and what brokers actually need. The platform integrates compliance workflows directly into your loan origination, CRM, and communication tools, so your team follows the right process without extra steps. Automated exception tracking, disclosure management, and audit-ready recordkeeping reduce the manual errors that drive exam findings. If you are building a new mortgage business and want a platform designed from the ground up for independent brokers, visit 1 Solution Mortgage Software to see how it fits your compliance and operational needs.

FAQ

What is the role of compliance in a new mortgage business?

Compliance defines the legal and operational boundaries within which a new mortgage business must operate. It covers federal regulations like HMDA, TILA/RESPA, ECOA, and BSA AML requirements, as well as state licensing obligations through the NMLS.

What is a Compliance Management System (CMS)?

A CMS is the structured program that connects a mortgage company's policies, training, monitoring, complaint handling, and corrective action into one operating cycle. The CFPB evaluates every supervised entity against its CMS components during examinations.

Why is HMDA compliance so critical for new lenders?

HMDA/Reg C violations represented 38% of all cited consumer violations for state member banks in 2024, making it the highest-risk reporting obligation for new mortgage businesses. Data entry errors and missing fields are the most common causes.

How does automation help with mortgage compliance?

Automated compliance testing saves lenders an average of 20 minutes and $14 per loan. That efficiency reduces manual errors, improves data submission accuracy, and frees compliance staff to focus on higher-judgment tasks.

When should a new mortgage business start building its compliance program?

A new mortgage business should build its compliance program before originating its first loan. Retrofitting a CMS after volume grows is significantly more expensive and creates gaps that regulators identify during early examinations.