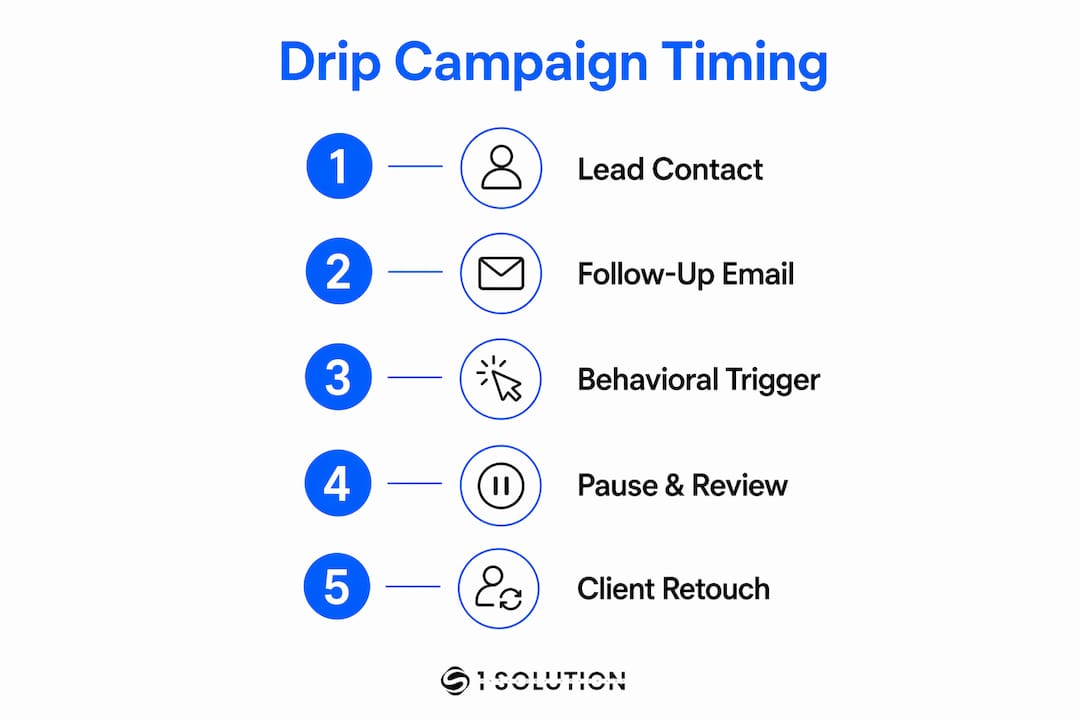

A mortgage drip campaign is an automated series of targeted messages sent to prospects and clients at timed or behavior-triggered intervals to move them from inquiry to closed loan. The industry term for this practice is "lead nurturing automation," and the two phrases are used interchangeably across mortgage marketing. Contacting a lead within 5 minutes of inquiry raises conversion rates by 9 times. That single statistic explains why brokers who rely on manual follow-up consistently lose deals to those running automated sequences. This guide covers the components, timing, behavioral triggers, compliance requirements, and performance metrics you need to build a campaign that actually closes loans.

What are the essential components of a mortgage drip campaign?

A mortgage drip campaign requires four foundational layers before you send a single message: a CRM, a communication platform, automation logic, and compliance infrastructure. Skipping any one of these creates gaps that cost you leads or expose you to regulatory risk.

CRM and communication integration is the starting point. Your CRM must sync in real time with your email and SMS platforms so that lead data, loan status, and contact history stay current across every channel. An API connection between systems prevents duplicate messages and ensures that when a lead moves from inquiry to pre-approval, the campaign responds accordingly.

Automation logic separates effective campaigns from basic scheduled emails. Two types exist: time-based drips, which send messages on a fixed schedule regardless of prospect behavior, and behavior-triggered workflows, which fire based on actions like link clicks, email opens, or loan milestone changes. Behavior-triggered responses produce 9 times higher reply rates than static, scheduled sequences. That gap is too large to ignore.

Compliance infrastructure is non-negotiable for mortgage professionals. Every email must include your NMLS ID, a valid physical address, and a working unsubscribe link under the CAN-SPAM Act. Missing these elements carries significant financial and legal penalties. The most practical fix is to build compliant footers directly into your email templates so they appear automatically on every send.

When evaluating automation platforms, compare feature categories rather than brand names. Entry-level tools handle scheduled sends and basic segmentation. Mid-tier platforms add behavioral triggers and CRM sync. Enterprise-grade systems include full mortgage automation tools with loan milestone tracking, multi-channel delivery, and built-in compliance controls. Match the platform tier to your volume and workflow complexity.

Pro Tip: Automate your compliance footer at the template level, not the campaign level. This way, every new template you create inherits the correct NMLS ID, physical address, and unsubscribe link without manual entry.

What is the ideal timing and sequence for home loan follow-up?

The research-backed standard for mortgage lead nurturing is a 12-step sequence spanning 21 days. Sending fewer than 8 emails in this window leaves engagement on the table. Sending more than 14 drives unsubscribes. The goal is consistent presence without crossing into noise.

The sequence structure should follow this cadence:

- Immediate SMS (within 5 minutes of inquiry): A short, personal message confirming you received their request and will follow up shortly. Speed here is the single biggest conversion lever.

- Email within the first hour: Introduce yourself, confirm your NMLS ID, and set expectations for next steps. Keep it under 150 words.

- Day 2 follow-up email: Share one piece of genuinely useful content, such as a first-time buyer checklist or a rate comparison explainer.

- Day 4 SMS check-in: A brief, direct message asking if they have questions. Two sentences maximum.

- Day 6 email: Address the most common objection at this stage, typically credit score concerns or down payment requirements.

- Day 8 value email: Provide a loan program overview tailored to what you know about their situation.

- Day 10 SMS: A soft nudge toward scheduling a call or completing a pre-qualification form.

- Day 12 email: A case study or testimonial from a similar borrower. Social proof works at this stage.

- Day 14 email: A direct call to action for a pre-approval application.

- Day 17 SMS: A final check-in for leads who have not yet responded.

- Day 19 email: A "last chance" message with a clear next step and your direct contact information.

- Day 21 email: A graceful close that moves the lead to a long-term nurture list.

Past clients deserve their own sequence. Quarterly contact with past clients produces 3.4 times more business than irregular follow-up. A simple four-email annual sequence covering rate updates, refinance opportunities, and referral requests keeps you top of mind without heavy effort.

Pro Tip: Build pause triggers into your sequence. If a lead clicks your pre-approval link on day 6, the campaign should pause the standard sequence and route them to a human follow-up workflow immediately. Static scheduling cannot do this.

How do behavioral triggers improve automated mortgage emails?

Behavioral triggers are the mechanism that turns a broadcast into a structured conversation. A time-based drip sends the same message to everyone on day 4 regardless of what they did on days 1 through 3. A behavior-triggered workflow reads what the prospect actually did and responds accordingly.

The key triggers to configure in any mortgage campaign include:

- Email open without click: The subject line worked but the content did not. Queue a follow-up with a different angle within 48 hours.

- Link click without form submission: The prospect showed intent but did not convert. Trigger an immediate SMS from the loan officer with a direct offer to help.

- Form submission: Remove the prospect from the drip and route them to an active pipeline workflow. Continuing the nurture sequence after a form submission is a common mistake that signals poor data integration.

- Loan status change: When a file moves from pre-qualification to pre-approval, trigger a congratulatory message and a checklist of next steps. This keeps the borrower engaged and reduces anxiety during the process.

- Inactivity for 7 days: Trigger a re-engagement message with a different subject line and a lower-friction call to action.

Top brokers implement CRM sequences that pause or shift based on prospect behavior, signaling when human interaction is needed. The trigger is not just a marketing tool. It is a workflow signal that tells the loan officer exactly when to pick up the phone.

Automation frees loan officers from routine touchpoints so they can focus on rate locks, underwriting issues, and closing tasks. The goal is not to replace human contact. The goal is to make human contact happen at the right moment, with the right context already established.

What compliance pitfalls should mortgage brokers avoid?

Compliance failures in mortgage email marketing are not just embarrassing. They are expensive. Federal law under the CAN-SPAM Act mandates that every commercial email include a valid physical address and a functional unsubscribe mechanism. For mortgage professionals, NMLS ID requirements add another layer that general email marketing guides do not cover.

The most common mistakes brokers make in their drip campaigns include:

- Missing or incorrect NMLS IDs in email footers, which creates regulatory exposure even when the content itself is compliant.

- Generic sender addresses like "team@brokerage.com" instead of the loan officer's direct email. Personalized sender addresses improve trust and engagement. Prospects are more likely to open and reply to a message from a named person.

- No unsubscribe link or a broken one. This is a direct CAN-SPAM violation. Test every template before activating a campaign.

- Sending too frequently in the first week. More than one message per day in the first 72 hours drives opt-outs before the relationship has a chance to form.

- Failing to suppress opted-out contacts across all channels. If someone unsubscribes from email, they should also stop receiving SMS messages from the same campaign.

"Automating required footer information minimizes the risk of compliance breaches. Federal law mandates a valid physical address and unsubscribe links in every commercial email. Building these into templates at the system level removes human error from the equation entirely."

Pro Tip: Schedule a quarterly template audit with your compliance officer. Regulations change, NMLS ID formats update, and state-specific disclosures evolve. A 30-minute review every quarter is far cheaper than a compliance penalty.

What metrics should you track to measure campaign performance?

Performance measurement turns a mortgage drip campaign from a set-and-forget tool into a continuously improving system. Key metrics include SMS delivery rate, SMS click rate, email open rate, email click-through rate, unsubscribe rate, and conversion rate.

| Metric | Healthy Benchmark | What It Signals |

|---|---|---|

| SMS delivery rate | Above 95% | Clean contact list and valid carrier routing |

| SMS click rate | Above 10% | Message relevance and call-to-action clarity |

| Email open rate | Above 25% | Subject line effectiveness and sender trust |

| Email click-through rate | Above 3% | Content relevance and offer alignment |

| Unsubscribe rate | Below 0.5% | Appropriate frequency and audience targeting |

| Conversion rate | Varies by segment | Overall campaign effectiveness against pipeline goals |

Review these metrics at the sequence level, not just the campaign level. An email with a 12% open rate on day 8 tells you something specific about that message. Aggregate campaign data hides those signals.

Combine quantitative data with qualitative input from your loan officers. If the day 6 email consistently generates phone calls asking the same question, that is a content gap the data alone will not reveal. Loan officers who work the pipeline daily know what prospects are confused about. Build that feedback into your next template revision.

Pro Tip: Track unsubscribe rate by message position, not just by campaign. A spike at message 4 tells you the cadence is too aggressive at that point. A spike at message 10 tells you the sequence is running too long for your audience.

Key Takeaways

A well-structured mortgage drip campaign combines behavior-triggered automation, strict compliance controls, and a 12-step sequence to convert more leads with less manual effort.

| Point | Details |

|---|---|

| Speed drives conversion | Contacting a lead within 5 minutes raises conversion rates by 9 times. |

| Sequence length matters | Use 8–14 messages over 21 days to maximize engagement without driving opt-outs. |

| Behavioral triggers outperform schedules | Trigger-based workflows produce 9 times higher reply rates than fixed-schedule drips. |

| Compliance is mandatory | Every email must include your NMLS ID, physical address, and a working unsubscribe link. |

| Past clients need consistent contact | Quarterly outreach to past clients generates 3.4 times more business than irregular follow-up. |

What I've learned about drip campaigns after 20 years in mortgage

Most brokers I talk to think of a drip campaign as a way to stay in front of leads while they are busy doing other things. That framing is partially right, but it misses the more important function. A well-built campaign is a diagnostic tool. It tells you exactly where a prospect is in their decision process based on what they do and do not engage with.

The shift from time-based drips to behavior-triggered workflows is the single biggest change I have seen in mortgage marketing over the past several years. Brokers who still run static sequences are essentially sending the same letter to everyone regardless of what they already know. That is not nurturing. That is broadcasting.

The compliance piece is where I see the most avoidable damage. Brokers spend weeks building a campaign and then launch it with a generic footer copied from a template they found online. One missing NMLS ID or a broken unsubscribe link can unwind all of that work. Build compliance into the system architecture, not the checklist.

The brokers who grow their pipelines consistently are not the ones sending the most messages. They are the ones sending the right message at the right moment, then getting out of the way and letting a loan officer close. Automation handles the volume. Human judgment handles the close. That division of labor is what makes the lead conversion process work at scale.

Hard money and non-QM referral pipelines also benefit from drip sequences. If you are growing your broker business with alternative loan products, the same behavioral trigger logic applies. The content changes. The structure does not.

— Omar Khamisa

How 1 Solution Mortgage Software supports your drip campaign

Mortgage brokers who want to run compliant, behavior-triggered campaigns without stitching together three separate platforms have a direct path forward with 1 Solution Mortgage Software.

1 Solution Mortgage Software was built by mortgage professionals who ran these workflows manually before building the tools to automate them. The platform includes pre-built compliant email and SMS templates with automated footers that carry your NMLS ID, physical address, and unsubscribe link on every send. Behavioral triggers connect directly to your CRM and loan pipeline so that when a prospect clicks a link or a file changes status, the right message fires automatically. Loan officers get notified when human follow-up is needed, freeing them to focus on closings rather than routine touchpoints. Visit 1 Solution Mortgage Software to see how the platform handles campaign automation, compliance, and pipeline management in one connected system.

FAQ

What is a mortgage drip campaign?

A mortgage drip campaign is an automated sequence of emails and SMS messages sent to prospects and clients at timed or behavior-triggered intervals to move them toward a closed loan. It is the standard lead nurturing method for mortgage brokers managing high inquiry volumes.

How many emails should a mortgage drip campaign include?

The research-backed standard is 8–14 emails over 21 days. Fewer than 8 misses key engagement windows, and more than 14 drives unsubscribes.

What compliance rules apply to mortgage drip campaign emails?

Every email must include your NMLS ID, a valid physical address, and a working unsubscribe link under the CAN-SPAM Act. Missing any of these elements creates legal and financial exposure.

How do behavioral triggers differ from standard drip sequences?

Behavioral triggers fire based on prospect actions like link clicks or email opens, while standard drips send on a fixed schedule regardless of behavior. Behavior-triggered campaigns produce 9 times higher reply rates than static sequences.

How often should you contact past mortgage clients?

Quarterly contact with past clients produces 3.4 times more business than irregular follow-up. A simple four-message annual sequence covering rate updates and referral requests is enough to maintain the relationship.