A mortgage operations manual is defined as a structured set of documents that translates company policies into role-specific procedures and task-level instructions, enabling consistent, compliant, and efficient mortgage operations. Every broker and lender who wants to pass a CFPB supervisory review, scale through a refinance boom, or onboard staff without chaos needs one. The manual is not a policy binder or a compliance checklist. It is the operational backbone of your lending business, covering everything from mortgage workflow design to exception handling. Without it, your team improvises. With it, your team executes.

What is a mortgage operations manual and what does it contain?

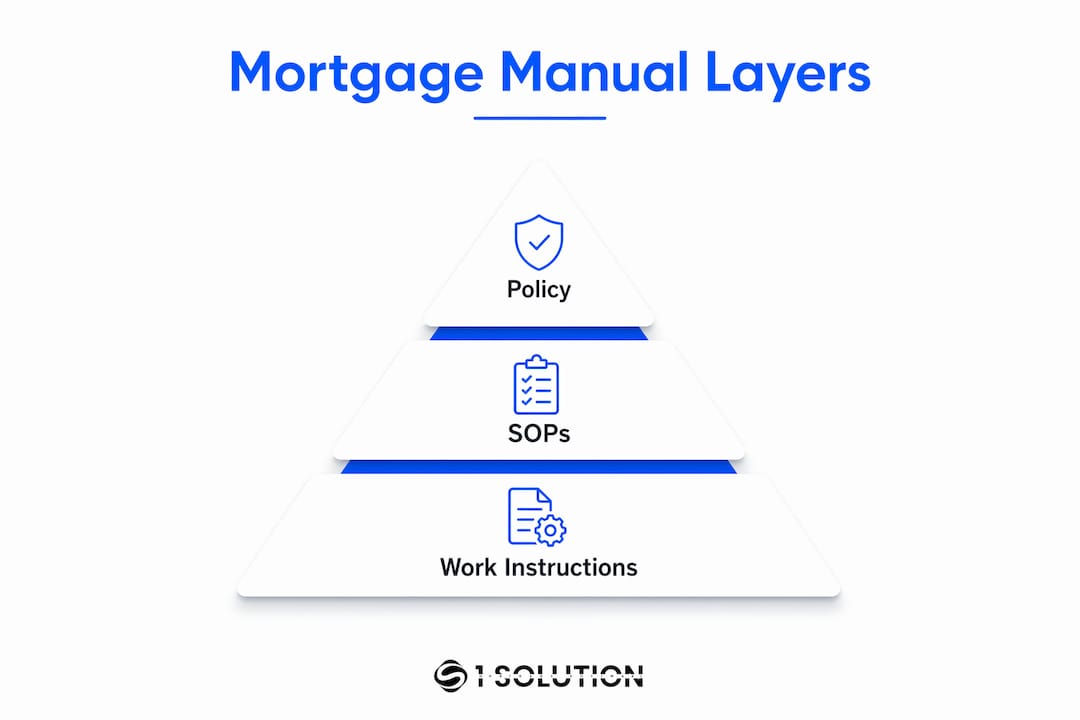

A mortgage operations manual is a hierarchical document system where policies establish "what" and "why," standard operating procedures (SOPs) define "how" at a workflow level, and work instructions provide task-level execution details. Mixing these three document types causes maintenance failures and compliance gaps. That distinction is the single most important concept in this entire guide.

Policies: the rules layer

Policies are governance documents. They state the rules your organization follows and the reasons behind them. A policy might read: "All escrow accounts must be reconciled monthly in compliance with RESPA requirements." It does not tell anyone how to reconcile. That is the SOP's job.

Standard operating procedures: the workflow layer

SOPs translate each policy into a repeatable, role-assigned workflow. A payment posting SOP, for example, assigns the task to a specific role title, defines the trigger (receipt of borrower payment), and specifies the output (updated ledger entry with timestamp). Written SOPs are primary evidence in CFPB supervisory reviews. Lack of written procedures is treated as a control deficiency.

Work instructions: the execution layer

Work instructions are the most granular level. They guide an individual operator through a specific task, step by step. A work instruction for payment posting might list the exact fields to enter in your Loan Origination System (LOS), in what order, and what to do if a field throws an error. Work instructions change frequently as systems update. Keeping them separate from SOPs means you update one document, not three.

| Document Type | Answers | Example in Mortgage Operations |

|---|---|---|

| Policy | What and why | Escrow reconciliation policy under RESPA |

| SOP | How, by whom, when | Payment posting SOP with role and trigger |

| Work instruction | Exact steps for one task | LOS field entry sequence for payment posting |

Pro Tip: Assign role titles in every SOP, never individual names. When staff turns over, the SOP stays accurate without a single edit.

Why is a mortgage operations manual critical for compliance and scale?

A well-built mortgage operations guide protects your business on two fronts: regulatory compliance and operational capacity. Structured, process-driven firms achieve 3x faster loan processing times than those operating without documented workflows. That speed advantage compounds during high-volume periods when every day of delay costs borrower relationships.

Audit readiness is the most undervalued benefit. When a regulator asks how your team handles a borrower dispute, your SOP is the answer. An operations manual creates an audit trail that verifies process completion even when errors occur. Verification of outputs, such as ledger entries and timestamped records, proves compliance. Without that trail, you are relying on memory and goodwill.

The importance of mortgage operations documentation also shows up in cost control. Firms using structured operational models reduce overhead costs by 30–50% through automation and defined workflows. That is not a technology benefit alone. It is a documentation benefit. Automation only works reliably when the process it follows is written down and tested.

Common pitfalls that destroy manual value include:

- Confusing policies with SOPs. A policy that reads like a procedure creates confusion about who owns what.

- Packing manuals with legal citations. Excessive legal text makes manuals unusable. Staff stop reading them. Manuals must be concise and actionable.

- Skipping exception paths. If your SOP only covers the clean scenario, your team has no guidance when something goes wrong.

- Using individual names instead of role titles. When that person leaves, the SOP becomes inaccurate overnight.

- No version control. An undated, unsigned SOP has no legal defensibility and no clear owner.

How to create a mortgage operations manual that actually works

Building a mortgage manual starts with scoping one process completely before touching anything else. Pick a high-volume, high-risk process like payoff request handling or loss mitigation intake. Map it end to end: what triggers it, who owns each step, and what the final deliverable is. Every SOP needs defined triggers and measurable outputs to support audits and process improvement. A payoff request SOP, for example, starts with receipt of the borrower's request and ends with delivery of the payoff statement within the required timeframe.

Follow this sequence when building each SOP:

- Define the trigger. What event starts this process? A borrower call, a system alert, a calendar date?

- Assign role titles. Name the processor, underwriter, or servicer responsible. Never use a person's name.

- Map the steps. Write each action in plain language. One action per step.

- Build in exception paths. Exception handling must live inside the SOP, not in an appendix. Regulatory timelines for borrower disputes and loss mitigation do not wait for you to find the right document.

- Define the output. What does "done" look like? A filed document, a system status change, a sent confirmation?

- Add version control. Date the document, name the approver, and log every revision.

- Separate work instructions. Keep granular task steps in a linked work instruction, not inside the SOP body.

- Schedule review cycles. Align reviews with regulatory updates, LOS changes, and market shifts. Quarterly is a reasonable default for high-risk processes.

Pro Tip: Build a one-page workflow map for each SOP. Visual process maps help new staff understand the flow in minutes, and they double as training tools when onboarding processors or building your mortgage team.

Operational checklists are a practical companion to SOPs. A pre-closing checklist tied to your closing SOP gives processors a daily reference without requiring them to read the full document every time. The checklist is not a replacement for the SOP. It is a shortcut for experienced staff who already know the process.

How do manuals adapt to automation and market shifts?

Modular manual design is the answer to fluctuating loan volumes. A modular approach means each process is documented independently, so you can activate, outsource, or hand off a single module without rewriting the entire manual. Modular operational manuals enable lenders to scale capacity within 48–72 hours in response to market shifts. That kind of speed is only possible when roles and handoffs are already written down.

Modern mortgage operations increasingly rely on automation tools integrated with the LOS. But automation does not eliminate exceptions. Operations manuals guide staff on handling the complexities that automated workflows cannot resolve. A human-in-the-loop model, where technology handles standard processes and trained staff manage exceptions, is the current best practice. Your manual defines exactly where that handoff happens.

Key features of a manual built for 2026 market conditions:

- LOS integration mapping. Document which system fields correspond to which SOP steps. This prevents errors when your LOS updates.

- Third-party fulfillment handoffs. Demand for specialized third-party fulfillment increased by 18%. When you outsource title, appraisal, or servicing tasks, your manual must define the handoff point and the expected output.

- Automation trigger documentation. For every automated step in your workflow, document what triggers it, what it produces, and who reviews the output.

- Exception escalation paths. Define who handles a stalled automated process and what the resolution timeline is.

You can explore mortgage automation tools that integrate directly with documented workflows to understand how technology and process documentation work together in practice.

| Manual Feature | Purpose | 2026 Relevance |

|---|---|---|

| Modular SOP structure | Rapid capacity scaling | Refinance booms, seasonal volume spikes |

| LOS field mapping | Reduce data entry errors | System updates and integrations |

| Exception escalation paths | Prevent compliance bottlenecks | CFPB oversight and loss mitigation timelines |

| Third-party handoff documentation | Clear accountability | Increased BPO and fulfillment outsourcing |

Key Takeaways

A mortgage operations manual is the single most defensible asset a broker or lender can build, because it converts institutional knowledge into verifiable, auditable process documentation.

| Point | Details |

|---|---|

| Three-layer hierarchy | Separate policies, SOPs, and work instructions to prevent compliance gaps and simplify updates. |

| Audit trail creation | Named roles and defined outputs in each SOP create verifiable evidence for CFPB reviews. |

| Cost and speed gains | Structured operational models reduce overhead by 30–50% and deliver 3x faster loan processing. |

| Modular design for scale | Independent process modules let you scale or outsource capacity within 48–72 hours. |

| Exception paths are mandatory | Build exception handling inside every SOP, not as an appendix, to meet regulatory timelines. |

Why I think most mortgage manuals fail before they're ever used

After 20 years working across mortgage operations as a processor, underwriter, loan originator, and systems consultant, I have seen the same failure pattern repeat itself. A broker or operations manager spends weeks building a manual, then nobody reads it. The reason is almost always the same: the manual was written for a regulator, not for the person doing the work.

The best mortgage operations guide I have ever seen was 40 pages. The worst was 400 pages and referenced 12 federal statutes in the first section. Efficiency in mortgage operations is a competitive differentiator that improves borrower experience by stabilizing throughput and reducing errors. You cannot get that efficiency from a document nobody opens.

The second failure I see constantly is treating the manual as a one-time project. Regulations change. Your LOS updates. Staff turns over. A manual that was accurate in january is often wrong by june. The brokers who win on compliance and operational speed treat their manual as a living system, not a filing cabinet artifact.

My honest advice: start with your three highest-risk processes, build clean SOPs with real exception paths, and review them every quarter. Do not wait until you have a perfect manual to start using it. An imperfect SOP that your team actually follows beats a perfect one that sits in a shared drive. The role of staff training in making those SOPs stick is just as important as writing them well.

The future of mortgage operations is not fully automated. It is human judgment applied at the right moment, guided by clear documentation. Brokers who build that foundation now will handle the next rate cycle, the next regulatory update, and the next staffing change without losing a step.

— Omar Khamisa

How 1 Solution Mortgage Software supports your operations

1 Solution Mortgage Software was built from the same operational challenges this article describes. The platform supports modular workflow design, role-based process mapping, and compliance management inside a single connected system. Brokers can document, assign, and track processes without stitching together separate tools. The LOS, CRM, POS, and compliance features work together so your documented workflows connect directly to the technology executing them. If you are ready to build a mortgage operations system that holds up under audit and scales with your volume, explore 1 Solution Mortgage Software and see how the platform supports independent brokers from origination through closing.

FAQ

What is a mortgage operations manual?

A mortgage operations manual is a structured set of documents that translates company policies into role-specific SOPs and task-level work instructions. It enables consistent, compliant, and auditable mortgage operations across all loan types and volume levels.

What is the difference between a policy and an SOP in mortgage lending?

A policy states the rule and the reason behind it, while an SOP defines the step-by-step workflow that fulfills that policy. Confusing the two creates compliance gaps and makes both documents harder to maintain.

Why do mortgage lenders need written SOPs for CFPB reviews?

Written SOPs are primary evidence in CFPB supervisory reviews. Lack of written procedures is treated as a control deficiency, which can result in enforcement action or required remediation.

How often should a mortgage operations manual be updated?

High-risk processes should be reviewed quarterly and updated whenever a regulatory change, LOS update, or staffing shift affects the documented workflow. Undated, unsigned SOPs have no legal defensibility.

What is a mortgage workflow and how does it relate to the manual?

A mortgage workflow is the sequence of tasks, roles, and handoffs that moves a loan from application to closing. The operations manual documents each workflow as an SOP, assigning ownership and defining outputs so the process is repeatable and verifiable. You can review the FHA loan process as a practical example of a documented mortgage workflow.