Mortgage technology adoption is the strategic integration of digital tools and AI to automate mortgage operations and improve client service outcomes. The industry crossed a clear threshold in 2026: 35% of mortgage professionals use AI daily, and 88% of current AI users plan to increase usage the following year. That is not a trend on the horizon. It is already the operating standard. Digital investment has also shifted decisively from borrower-facing tools to back-office automation, with document extraction, processing, and closing workflows now receiving the majority of new spending. For mortgage brokers and loan officers, understanding this shift is the first step toward making technology work for your business rather than against it.

What are the core technologies driving mortgage technology adoption today?

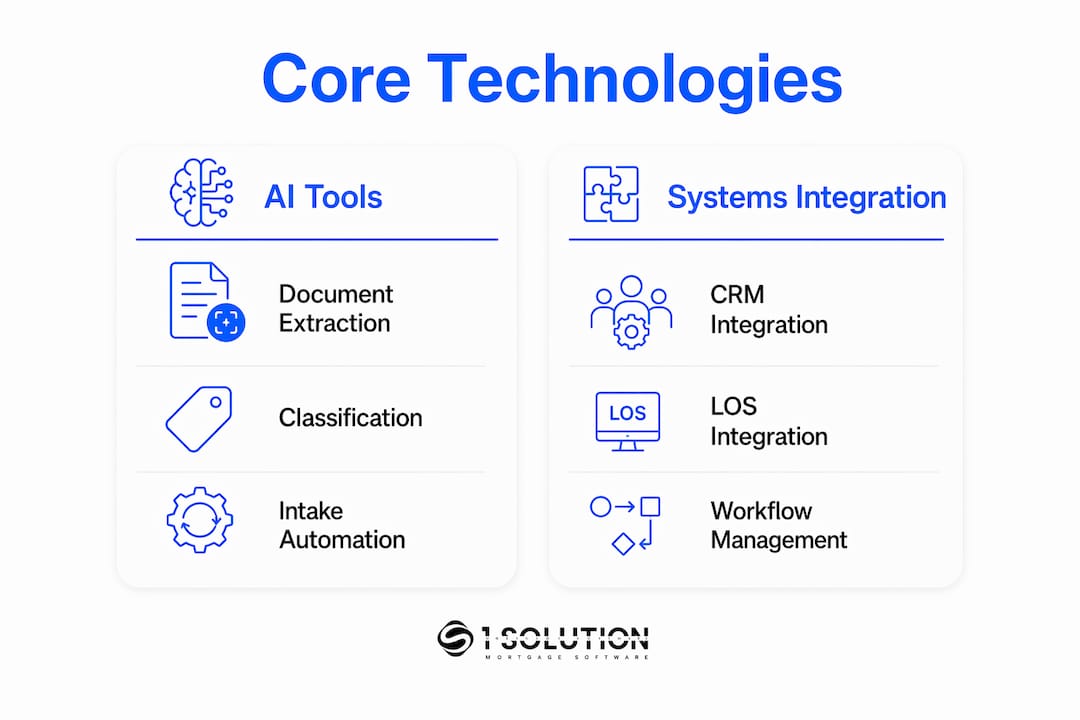

The digital transformation in the mortgage industry centers on four technology categories: AI-enabled document extraction, borrower intake automation, CRM and LOS integration, and marketing automation. Each category addresses a distinct operational bottleneck, and brokers who understand the difference between them make better investment decisions.

Document classification and reading are the leading AI use cases in mortgage operations today. Document classification leads at 68% adoption among AI-using lenders, followed by document reading at 59%. These tools reduce the manual labor of sorting and extracting data from pay stubs, tax returns, and bank statements, which cuts processing time and error rates significantly.

Borrower intake automation addresses a different problem. Online mortgage application abandonment averages 67%, meaning most leads who start an application never finish it. That is a direct revenue leak. Conversational AI tools capture and qualify those leads around the clock, converting form abandonment into active pipeline.

CRM and LOS integration ties everything together. Without a connected system, brokers manage data across multiple platforms, which creates duplicate entry, compliance gaps, and lost follow-up. Marketing automation, including mortgage drip campaigns, keeps prospects engaged between touchpoints without requiring manual outreach.

| Technology category | Primary function | Adoption signal |

|---|---|---|

| AI document extraction | Reads and classifies loan documents automatically | 68% of AI-using lenders |

| Borrower intake automation | Captures and qualifies leads 24/7 | Addresses 67% abandonment rate |

| CRM and LOS integration | Connects pipeline data across systems | Rated critical by 82% of brokers |

| Marketing automation | Automates prospect nurturing and follow-up | Reduces manual outreach burden |

Pro Tip: When evaluating AI document tools, choose purpose-built third-party solutions over native LOS AI. Only 6% of lenders rely on native LOS AI for document processing, while 53% use purpose-built tools, which consistently outperform on accuracy and flexibility.

What are the biggest challenges mortgage professionals face when adopting new technology?

Integration complexity is the single largest barrier to mortgage software adoption. 82% of mortgage brokers rate integration as highly important, giving it an average score of 8.81 out of 10. That number reflects a real operational reality: a tool that does not connect to your LOS or CRM creates more work, not less.

The most common adoption barriers mortgage professionals report include:

- Integration failures. New tools that cannot communicate with existing systems force manual data transfer, which defeats the purpose of automation entirely.

- Training gaps. Brokers often receive a one-time onboarding session and then are left to figure out the platform on their own. Usage drops within weeks.

- Security and compliance concerns. Mortgage data is sensitive. Brokers need platforms that meet regulatory standards without requiring them to become compliance experts.

- Cost misalignment. Many platforms price for enterprise lenders, not independent brokers. The result is paying for features you will never use.

- Resistance from loan officers. MLOs who were not involved in the selection process often view new tools as a burden rather than a benefit.

The solution to most of these barriers is not a better tool. It is a better implementation process. Over 32% of brokers say they would adopt digital tools if lenders provided integration support. That tells you the demand is there. The gap is in execution.

Pro Tip: Before signing any software contract, ask the vendor for a documented integration path with your current LOS. If they cannot provide one, the tool will likely sit unused within 90 days.

How can mortgage professionals effectively adopt technology to maximize ROI?

The most expensive technology investment is one your team does not use. Tracking login frequency, lead follow-up rates, and automation usage tied to performance incentives is what separates successful implementations from shelf-ware. Adoption is not a launch event. It is an ongoing management discipline.

A practical adoption sequence for mortgage brokers looks like this:

- Identify your highest-friction workflow first. For most loan officers, that is lead intake. Fixing the point where pipeline leaks gives you the fastest measurable return and builds internal confidence in the technology.

- Run a pilot with a small group before full rollout. Loan officers who participate in workflow design and pilot testing become internal champions. Their buy-in is more persuasive than any vendor demo.

- Build a 30/60/90-day training schedule. A single onboarding session is not enough. Refresher training at 30, 60, and 90 days after launch catches the gaps that only appear once people are using the system in real conditions.

- Assign a dedicated system administrator. Someone on your team needs to own the platform, handle questions, and monitor usage data. Without this role, adoption problems go unaddressed until they become expensive.

- Measure what matters. Track login frequency, lead response time, pipeline accuracy, and automation rates weekly. Tie these metrics to team performance reviews so adoption has real accountability.

- Expand incrementally. Once one workflow is running well, add the next. Avoid replacing your entire tech stack at once. Targeted adoption starting with lead intake and processing bottlenecks reduces disruption and proves value before you scale.

Speed of follow-up is one area where the data is unambiguous. Contacting a prospect within one hour increases the likelihood of qualification nearly seven times compared to waiting longer. Automating that first contact is not optional for brokers who want to compete on lead conversion. You can learn more about building this process in a lead conversion guide built specifically for brokers.

Understanding your broker efficiency metrics before and after adoption also gives you a clear picture of ROI. Without a baseline, you cannot prove the technology is working.

How are AI and automation reshaping loan origination and servicing?

AI is not replacing mortgage professionals. It is changing which tasks they spend time on. The shift is from manual data handling to relationship management and judgment calls, which is where MLOs create the most value.

The most widely adopted AI use cases in mortgage operations today are:

- Document classification and extraction. AI reads and sorts loan documents faster and with fewer errors than manual review. 65% of lenders plan to invest in document extraction in 2026, making this the clearest near-term investment priority.

- Conversational borrower intake. AI-powered chat tools collect borrower information, answer basic questions, and pre-qualify leads without requiring a loan officer to be available. This directly addresses the 67% application abandonment rate.

- Underwriting and income analysis. AI tools that analyze income documents and flag underwriting issues are used by 26% of mortgage professionals, according to the 2026 broker survey.

- Guideline research. AI assistants that search and summarize lending guidelines save loan officers hours per week. 34% of brokers now use dedicated guideline AI tools.

The impact on loan volume capacity is real. When processors spend less time sorting documents and loan officers spend less time chasing leads manually, the same team can handle more files. That is the core benefit of mortgage tech trends pointing toward back-office automation.

AI works best when paired with human oversight for compliance, client communication, and final review. Brokers who treat AI as a research and drafting assistant rather than a decision-maker get the productivity gains without the compliance risk. For a full breakdown of available tools, the mortgage automation tools guide covers the current category landscape in detail.

Key Takeaways

Successful mortgage technology adoption requires treating implementation as a change management process, not a software purchase, with integration, training, and measurement as the three non-negotiable pillars.

| Point | Details |

|---|---|

| Start with lead intake | Fixing borrower intake automation delivers the fastest ROI for most loan officers. |

| Integration is the top barrier | 82% of brokers rate integration as critical; always confirm LOS compatibility before purchasing. |

| Training must be ongoing | One-time onboarding fails; schedule refresher training at 30, 60, and 90 days post-launch. |

| Measure adoption metrics | Track login frequency, lead follow-up rates, and automation usage weekly to sustain gains. |

| AI augments, not replaces | Use AI for document processing and intake; keep humans in charge of compliance and client decisions. |

What I've learned about technology adoption after 20 years in mortgage operations

The biggest misconception I see is that brokers treat technology adoption as a purchasing decision. They research platforms, compare features, sign a contract, and then wonder why their team is still doing things the old way six months later. The platform was never the problem.

I have worked as a processor, underwriter, loan originator, and systems consultant. Every failed implementation I witnessed had the same root cause: the people who had to use the system were not involved in choosing or designing it. Loan officers who feel like a new tool was imposed on them will find every reason not to use it. Loan officers who helped build the workflow around it will defend it to new hires.

The second thing I have learned is that full system replacements almost always fail. The disruption is too large, the learning curve hits everyone at once, and the team loses confidence before the tool has a chance to prove itself. Starting with one pain point, fixing it well, and then expanding is slower on paper but faster in practice.

AI is the area where I see the most unrealistic expectations right now. Brokers either dismiss it entirely or expect it to run their operation without oversight. The reality is more useful than either extreme. AI handles the high-volume, repetitive work. Your MLOs handle the judgment, the relationships, and the compliance decisions. That division of labor is what actually moves the needle on loan volume.

My honest advice: pick one workflow that is costing you time or pipeline, find a tool that integrates with what you already have, involve your team in the rollout, and measure the results before adding anything else.

— Omar Khamisa

How 1 Solution Mortgage Software supports your adoption process

Adopting mortgage technology works best when the platform was built by people who have done your job. 1 Solution Mortgage Software was founded by Omar Khamisa after two decades working across mortgage operations, and every feature reflects a real workflow problem brokers face.

The platform connects pricing, CRM, POS, LOS, compliance, marketing, and communication tools into one ecosystem. That means no integration gaps between systems, no duplicate data entry, and no compliance blind spots. The all-in-one mortgage platform also includes training support and a structure designed for independent brokers, not enterprise lenders. If you are ready to adopt technology that your team will actually use, 1 Solution Mortgage Software is built for exactly that.

FAQ

What is mortgage technology adoption?

Mortgage technology adoption is the process of integrating digital tools and AI into mortgage operations to automate workflows and improve client service. It covers everything from borrower intake automation to document processing and CRM integration.

What is the biggest barrier to adopting mortgage technology?

Integration complexity is the top barrier. 82% of mortgage brokers rate integration as highly important, and disconnected tools are the most common reason adoption fails after launch.

Where should mortgage brokers start with technology adoption?

Borrower intake automation delivers the fastest ROI for most loan officers. Contacting a prospect within one hour increases qualification likelihood nearly seven times, making automated lead response the highest-leverage starting point.

How does AI fit into mortgage operations without replacing loan officers?

AI handles document classification, intake, and guideline research. Human MLOs retain responsibility for compliance review, client relationships, and final decisions. That division keeps productivity high without introducing regulatory risk.

How do you measure whether mortgage technology adoption is working?

Track login frequency, lead follow-up compliance, automation rates, and pipeline accuracy on a weekly basis. Tying these metrics to performance reviews creates the accountability needed to sustain adoption over time.